The Brent oil price tanked 3.4% to $48.77 last night as the emerging market news flow turned nasty. First up was China’s sputtering industrial growth. That was followed by news that Saudi Arabia stockpiles are growing fast as exports struggle and Iran is readying its oil deluge, from the FT:

Speaking in Tehran at the first international oil and gas conference since a nuclear deal was struck in July, Bijan Namdar Zanganeh told representatives of some of the world’s biggest energy companies he is prioritising a return to Iran’s pre-sanctions export levels, the development of energy sector technology and access to international financial markets.

…“From the first day that nuclear agreement is implemented and sanctions are lifted, Iran will increase its exports,” he said.

Sanctions linked to Iran’s nuclear programme have cut the Opec member’s oil exports to little more than 1m barrels a day in recent years, putting pressure on its economy and shutting out western companies from some of the world’s richest energy deposits.

…Mr Zanganeh said Iran could increase production by 500,000 b/d immediately after the lifting of sanctions and reach its pre-sanctions output level within seven months.

That would double the current oil glut overnight. Here’s a useful chart from Forbes on the current surplus:

We should perhaps Iranian protestations with a grain of salt but there is no doubt that Iran will make things worse and that it entrenches the market share battle dynamics with hegemomic sparring partner, Saudi.

The perceived balance of risks has shifted significantly over the last six weeks and hedge funds have reacted by trimming their short positions.

Goldman Sachs, among the biggest bears, has acknowledged “there are growing signs of a supply side adjustment and rebalancing taking place” though the bank warns about become bullish too soon (“Oil Gauge: On the road to rebalancing, but patience needed” Oct 14).

Barclays is blunter. “Current price levels are not nearly high enough to encourage production over the medium term” the bank warned and “prices need to move higher than what the oil futures market is currently pricing in, or there will not be enough supply” (“Oil

special report: upward bound” Oct 14).

…Oil production from the four largest shale plays is forecast to decline 93,000 barrels per day (bpd) in November, the biggest monthly decline to date, according to the U.S. Energy Information Administration.On the demand side, there is clear evidence of higher fuel consumption in the United States and other advanced economies, as well as India and China, in response to continued economic recovery and lower prices.

With some of the extreme shorts squeezed out, we could go lower. Chinese consumption has been rising on an inventory build and its “recovery” is a glide slope to lower growth. Oil will get support from the bearish supply side news flow but I can still see it going lower as the EM crisis rolls on.

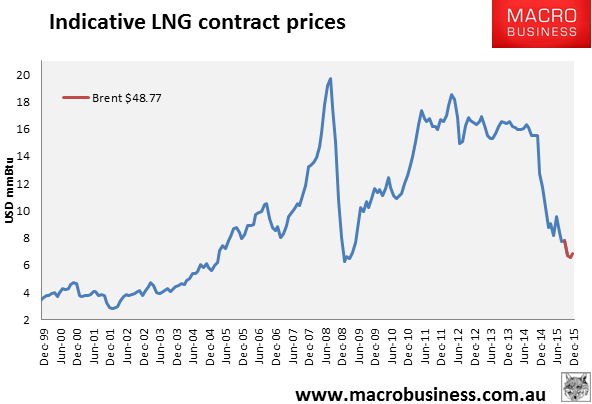

Turning to LNG, the indicative oil-linked contract price was hit hard to $6.83mmBtu:

No news of interest.