The Australian Financial Review‘s Street Talk column revealed last week the miner had narrowed discussions to Hebei Iron and Steel to sell a partial stake in its mines, rail and port infrastructure

“It’s more likely it will come down to an equity stake in a project and a combined capital injection,” Morgans resources analyst James Wilson said.

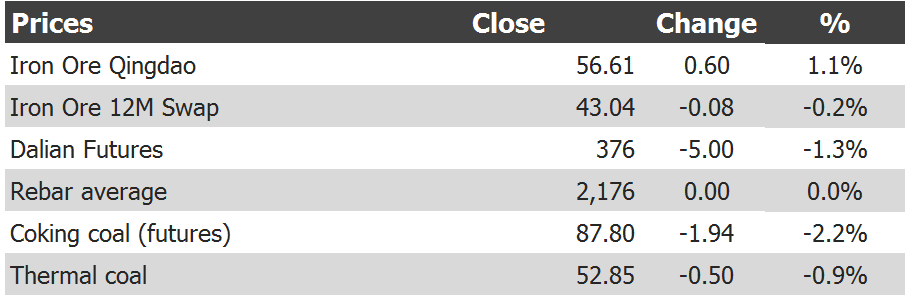

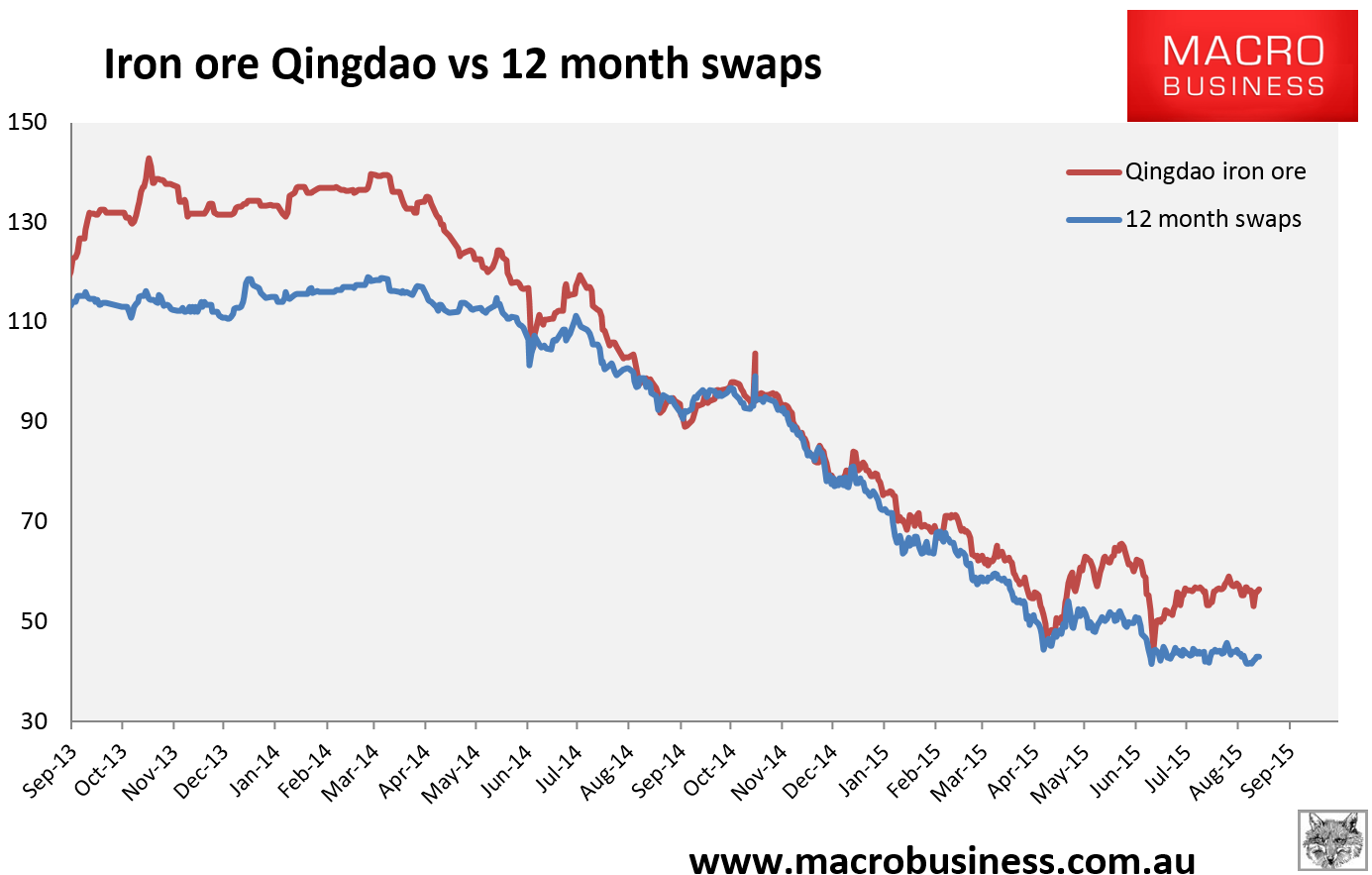

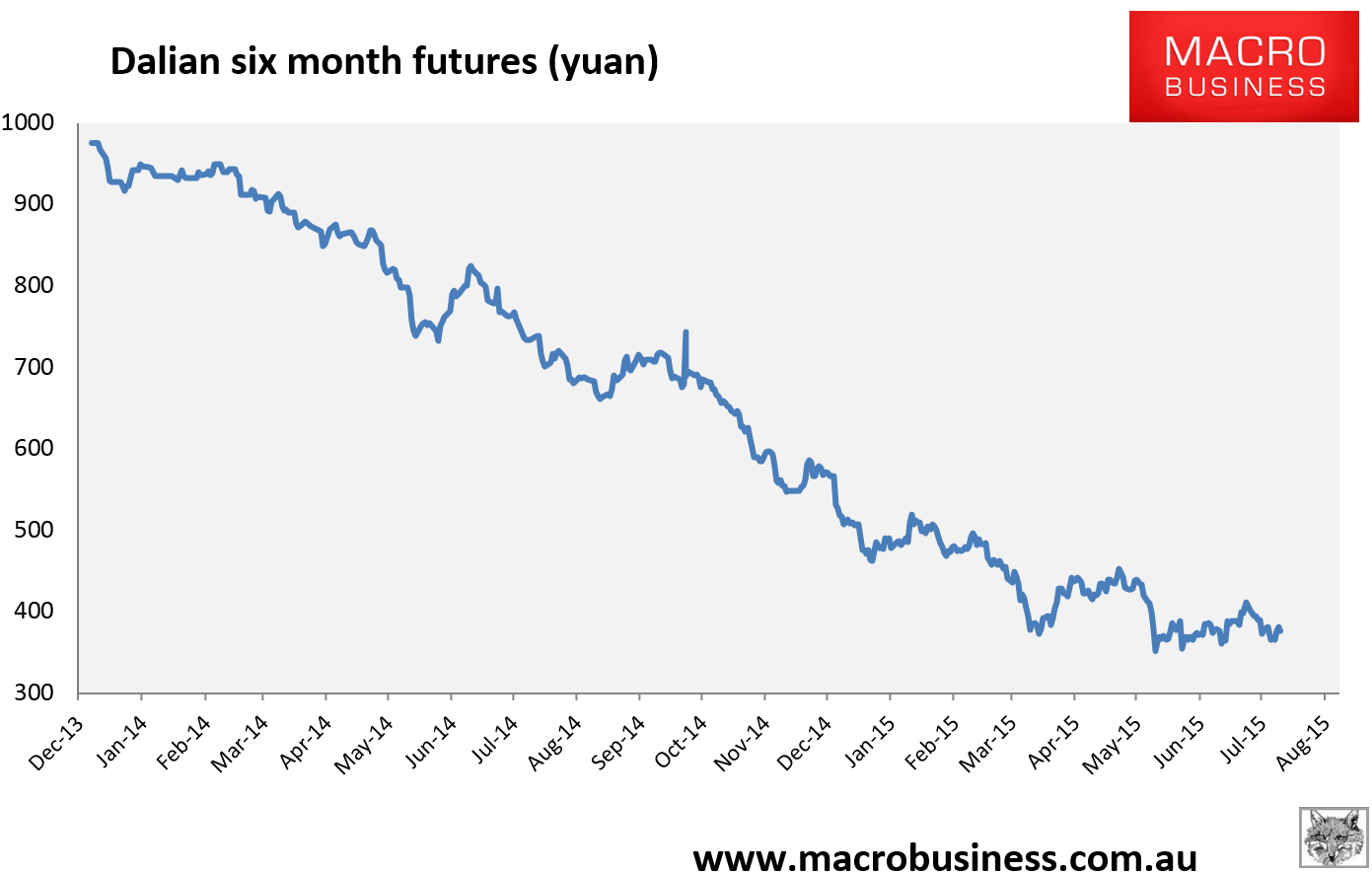

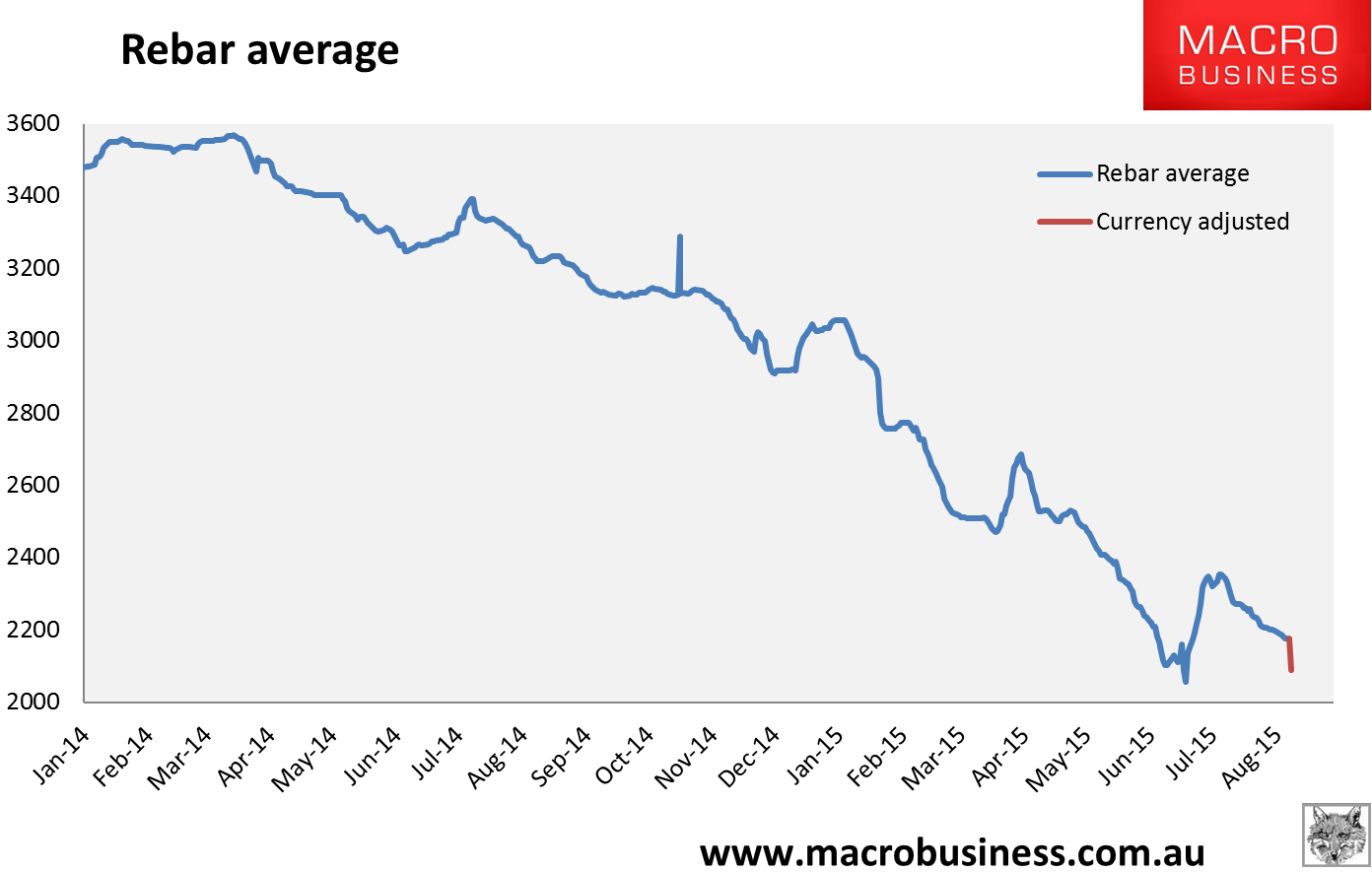

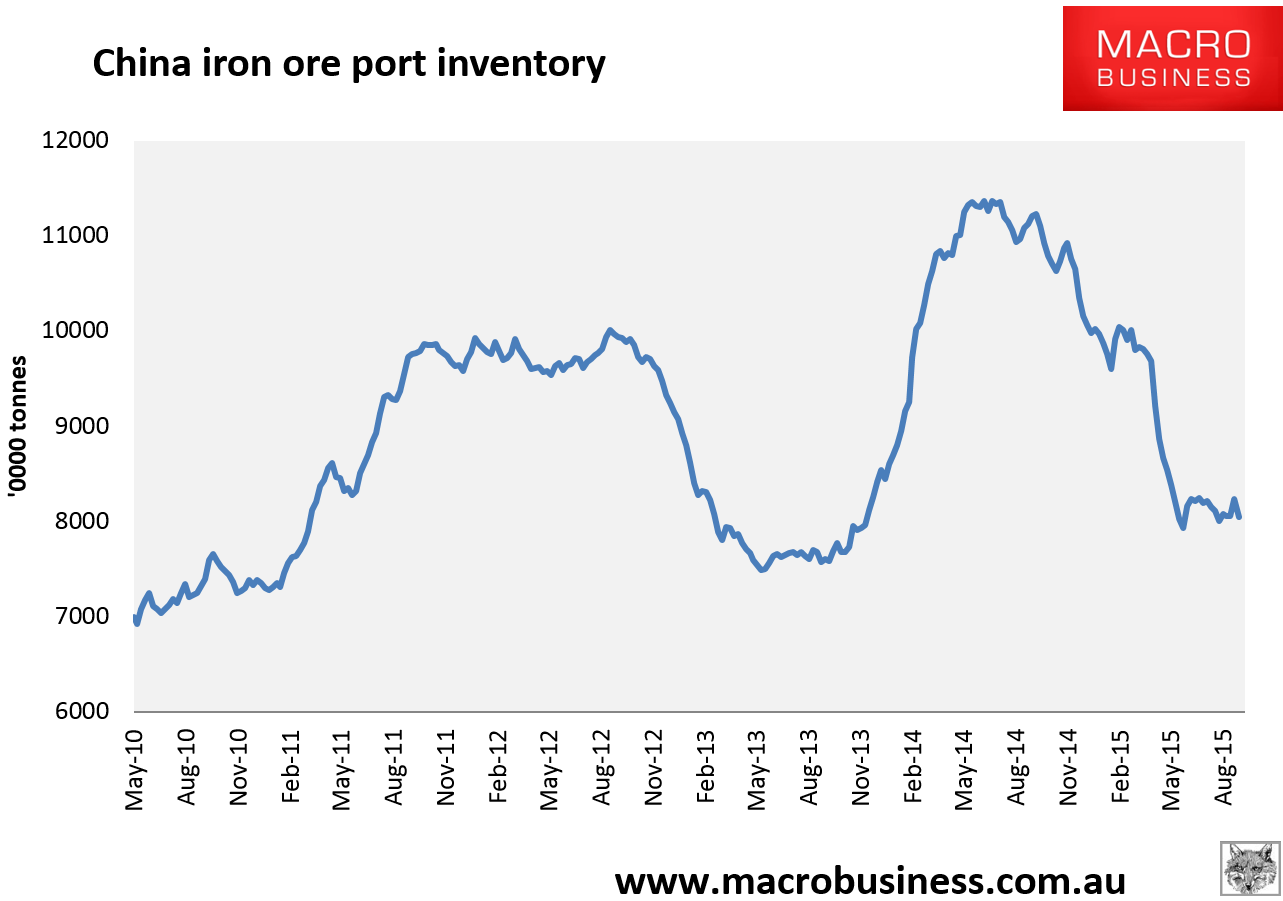

Here are the iron ore charts for October 12, 2015:

Spot firm with benchmark up 0.4% to $55.70. Paper eroding. Rebar flat. Broader bulks in trouble. Chinese iron ore port stocks down 2 million tonnes over the break. That’s enough to explain the recent buying interest.

Not much in news beyond some more FMG scuttlebutt at the AFR:

Advertisement

Mr Wilson said a sale of Fortescue’s more mature Cloudbreak and Christmas Creek mines at its Chichester hub was more likely to be on offer, with a 30 per cent stake likely to generate about $2 billion.

The miner could generate a further $1 billion from a share placement as part of a potential deal, he said.

Street Talk also revealed Fosun International had cast an eye over the Chichester assets but walked away.

“Solomon is the jewel in the crown and we don’t anticipate FMG would look at selling this,” Mr Wilson said.

If I’m buying I wouldn’t want Chichester. By my calculations Solomon spits out ore at $35FOB and Chichester at $39FOB. Come to think of it, I wouldn’t want either given my long term outlook is for ore to find an equilibrium around $30.