Sequentially, iron ore supply should continue to strengthen into year-end, both for seasonal and structural reasons, while pig iron production will likely soften. This should ensure plentiful supply availability in an already oversupplied market, and no need for mills to ‘bid up’ material. This was reflected in our latest steel survey, which showed that the raw materials purchasing appetite of mills had dropping to the lowest level on record. This is also a reflection of the risk of further steel mill closures in a massively loss-making Chinese steel industry.

The inventory situation in coking coal is even starker, with combined coke plant and port inventories at their lowest recorded level (Fig 3). One might be inclined to believe that Chinese protectionism, which has cut coking coal imports by almost 20% YTD, is a large part of the explanation for low port inventories. But even if these are removed, coke plant stocks alone are also at their lowest recorded level. Combined with domestic supply cuts – we have seen negative YoY supply growth over the past 3 months – and seaborne supply that is ex-growth, the implication is that there might be some near-dated price support. Relative to iron ore, coking coal may indeed prove to be marginally more resilient, but demand and sentiment are just as weak, macro factors continue to weigh and for the seaborne market, arguably the most important factor is whether the Chinese decide upon further protectionism.

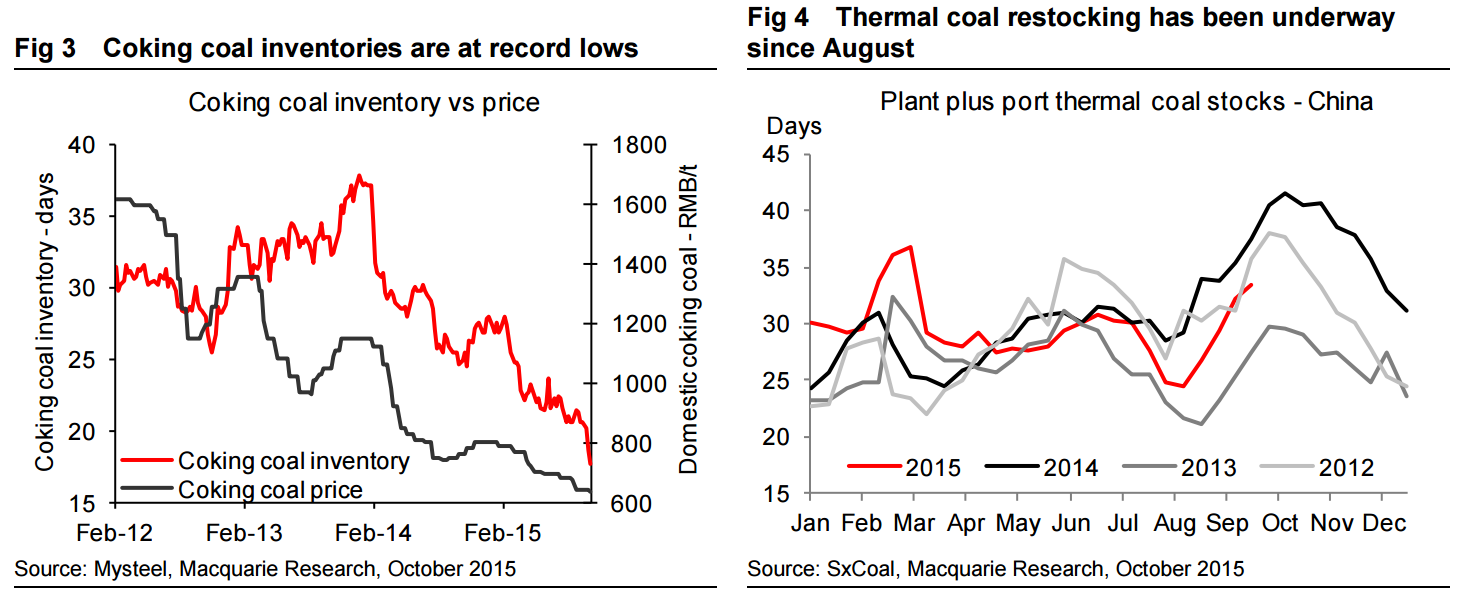

On the thermal coal front, the usual pre-winter restock commenced in August and there may be slightly further to go in the process (Fig 4). However most of the restocking is likely to be done and given that throughout this period domestic thermal coal prices continued to drop, now down 30% YTD, and that the industrial sector continues to look weak, only production cuts and/or more protectionism look likely to make a difference to pricing. Short-term price risk remains skewed to the downside.

This more or less supports my contention that iron ore and the wider bulks prices are simply going to keep bleeding. Low inventories take away the danger of big cyclical drops in the market but the poor business conditions causing the inventory rundown also ensures no year end restocking. Sheer weight of market imbalance is now the determining price factor and that means ongoing price erosion.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

Sequentially, iron ore supply should continue to strengthen into year-end, both for seasonal and structural reasons, while pig iron production will likely soften. This should ensure plentiful supply availability in an already oversupplied market, and no need for mills to ‘bid up’ material. This was reflected in our latest steel survey, which showed that the raw materials purchasing appetite of mills had dropping to the lowest level on record. This is also a reflection of the risk of further steel mill closures in a massively loss-making Chinese steel industry.