I’m sorry to say it but it’s true. In fact, the scenario is shockingly easy to imagine, is already playing out, though who knows how fast it arrives and how deep it goes? It has three cascading dominoes to it.

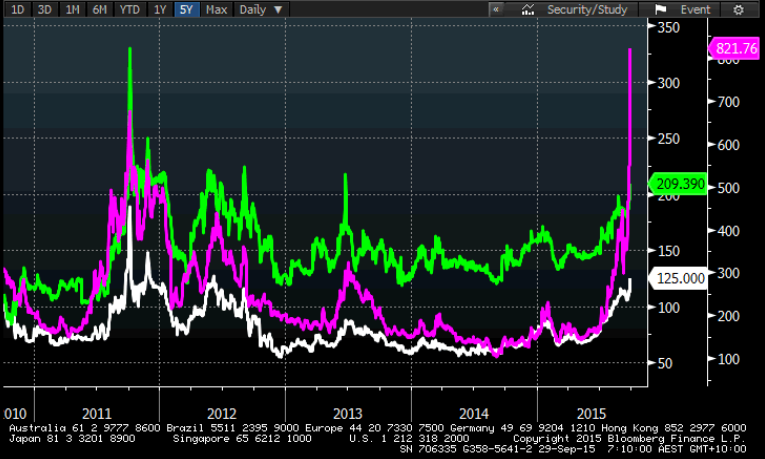

The first is an anything but ordinary global commodities bear market. It is shaping up as one of the greatest bubbles, mis-allocations of capital and busts in the history of capitalism. The macro dynamics at work in the global economy virtually ensure commodity prices will continue to fall as China slows and the US speeds up, boosting its dollar. This is exacerbated by other nations like Europe and Japan doing QE. That is a double hit to commodity prices in the form of weakening demand and a monetary headwind. In turn, commodity exporting emerging markets (EM) are double-smashed via falling exports and capital flight. At some point one these EMs is going to default big and unleash a credit panic around commodities and EM debt (that is, if Glencore doesn’t do it first). That will bring on the final great crash in the commodities shakeout.

It has already started in debt markets with the CDS prices of many EMs already ripping higher with major miners in tow:

To imagine the impact of this on Australia consider that if the tide on commodity debt does go out then it will bankrupt such household names as Fortescue Metals, Arrium, Santos and Origin Energy, virtually simultaneously. There is nothing in Australian contemporary history to compare with such an event.

That brings us to domino number two. Australian households will be in the direct line of fire as the share market denudes them of retirement savings, an huge labour market shock hits and the Budget is ravaged. They will bunker of course. That will immediately pour the commodity contagion into housing markets where prices will roll over and begin to fall.

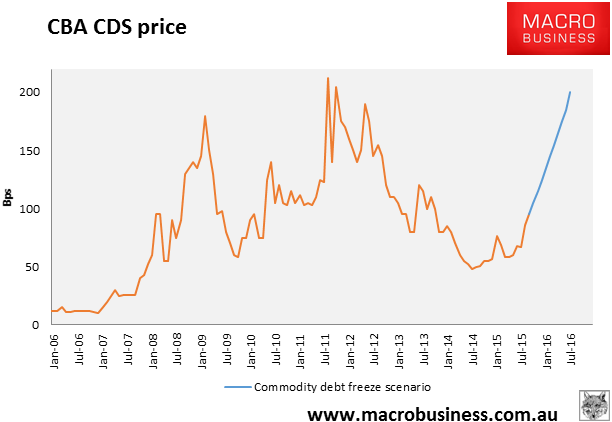

The rate cuts that follow will be swift and deep. Well, not that deep actually, -1.5% in short order, to a bottom at 0.5%. Compare that to the relief served up in the GFC of -4% and it does not look so comforting. Worse, Australian bank funding costs will also soar:

As such, banks will not pass on a large portion of the rate cuts as they seek to recover lost net interest margins. The banks will also be locked out of global markets for their wholesale funding needs so the RBA will have to activate its emergency liquidity facility to keep them afloat.

So, as house prices keep falling despite rate cuts and consumers stop spending, unemployment rises and population growth falls, as the terms of trade crater, the capex cliff continues, the residential construction boom goes bust, and the car industry shutters, recessionary conditions will spread, triggering fiscal stimulus. It will come in two forms, letting the automatic stabilisers run without cutting spending and actual Keynesian stimulus spending initiatives.

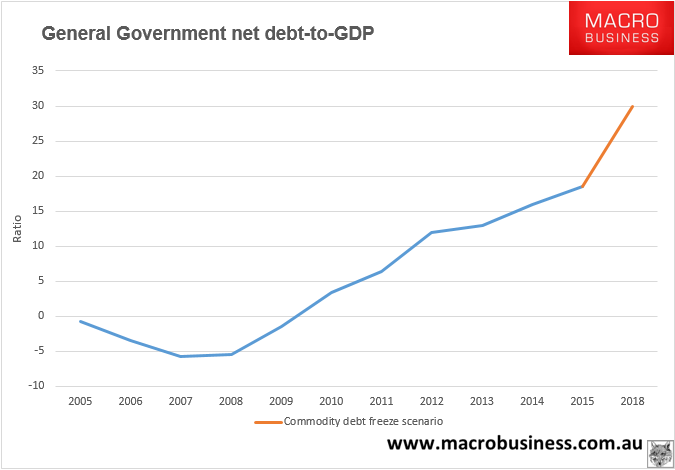

However, it will be much smaller than the Rudd stimulus because net debt is already at around 18% of GDP and rising fast. And here we come to the last domino. The Budget will be posting $100 billion plus deficits so the trajectory for sovereign debt will be a rather swift punch through the AAA-securing ceiling of 30% net debt to GDP:

S&P is not going to wait for it to happen to downgrade the rating. They’ll do it the moment the trajectory is set.

So, now we’ll have weak and perhaps still falling house prices, banks on life support at the RBA, frightened households shocked anew at sovereign downgrades, swiftly deteriorating asset quality at the banks necessitating a lot more government spending yet a credit rating under ongoing pressure, and stubbornly high bank funding costs as any public guarantee of the bank’s borrowing in frozen offshore debt markets is of limited use.

It’s a very negative feedback loop that could see house prices fall, and fall, and fall.