Special Report: How to profit from a house price crash

Undoubtedly the biggest asset that Australians aspire to and acquire is property, either owning your home and/or investing in residential property. This has been the most risk free investment in the last 30 years as the traditional Anglo-Saxon cultural bias towards owning one’s home has been deliberately transformed into an enormous edifice of greed and largesse, fostering one of the world’s biggest asset bubbles.

In this report we will first examine the prognosis for Australian residential property as the economy goes into an income shock not seen in almost a century.

Next, a discussion of the optimal strategy available to the retail investor to protect against and profit from a significant decline in residential property prices.

Finally, looking at the circumstances facing four typical homeowners and investors, we look at practical solutions that can both protect and hedge from this coming storm.

Prognosis

The “once in a century mining boom that shall never end” is over. Australia’s fateful mistake to latch on to an endless commodity boom just as China begins to restructure its growth led economy amid an enormous supply response has created a gigantic risk to the other “boom that will never end” – house prices.

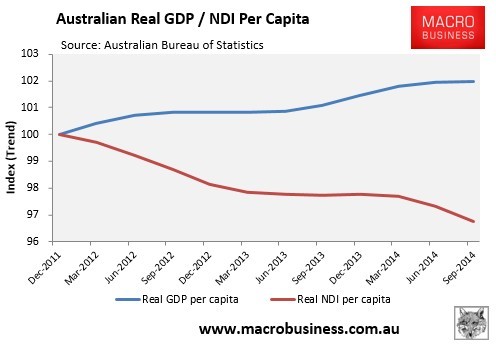

Beyond the headline GDP (gross domestic product) number that “measures” economic growth, the truth is the significant falls in commodity prices from the beginning of China’s slowdown and the supply response have reversed national disposable income (NDI), leading to an income recession:

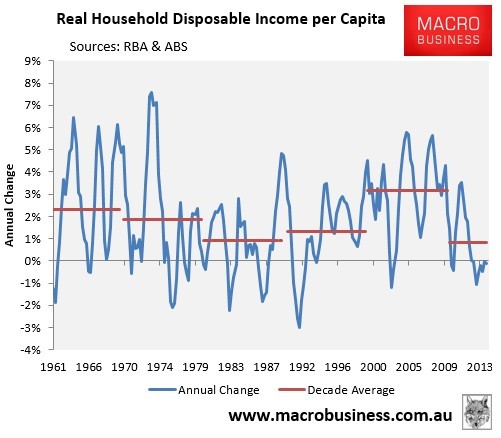

So while the economy per se is not in recession, due to export volumes of commodities whose receipts go to foreign owned mining companies, households are in recession. This is showing up in the lowest level of wage growth on record and household income growth slowing to a 60 year low at barely 0.8% per annum:

This income shock at the beginning of the end is nothing compared to what is coming down the line as the surge in mining investment – construction of mines, related infrastructure etc. – not only slows down, but retracts from economic growth from as early as 2016.

This will cause a huge drop in mining sector jobs as they retract by as much as two-thirds or approximately 100,000 unemployed as the construction phase turns into a low manpower operational phase. Add to this number is the approx. 40,000 jobs to be lost when the car industry closes shop in 2016/17 as the manufacturing industry was destroyed during the mining boom due to the high dollar.

The offset to this large shock in unemployment is the housing boom itself. The Reserve Bank of Australia (RBA) has attempted to rebalance this risk by the “wealth effect” that is inflating house prices which lead to increased consumer spending and mortgages creating a positive feedback loop. Again, like in any boom, the supply response to this effect has been a construction boom and an investment frenzy, concentrated in Melbourne and Sydney, creating unsustainable double digit price growth.

However, this plug in the dyke is starting to fail as the construction boom peaks, with dwelling approvals declining as population growth rate falls. This is confirmed by a peak in housing finance and investor mortgage growth as concern over the east coast bubble has led to some regulatory restriction of housing loans and other macroprudential measures, including a significant crackdown on foreign investment in the Sydney housing bubble.

The main factor however is the elephant in the room. Australian households have one of the highest levels of debt in the developed world, currently at 165% of GDP and rising. While other nations deleveraged after the GFC, Australians doubled down and continued to borrow money to buy mostly existing houses off each other.

With declining income, households can no longer afford to borrow more, even as interest rates reach multi-decade lows. The RBA has had to cut rates further than anyone has expected, which has had the benefit of lowering the Australian dollar and helping out tradeable sectors like tourism and manufacturing, but this is nowhere near enough and too late to offset the income shock. The RBA will be forced to continue to lower interest rates as unemployment inexorably rises and to service the mountain of private debt.

On the fiscal side, the Coalition government is restricted in both political expedience in keeping a “tight budget” and external sovereign rating on the ever increasing public debt. The current AAA rating is very important because it is the key determinant in how the banks – the engine of the housing boom – fund their loan books. A loss of this rating and banks must pay more for the same amount of lending, which will lead to finance rationing and/or tighter loan restrictions just as government and the RBA run out of stimulus ammunition.

Scenarios

This scenario above is the base case and suggests a set of conditions for the next three to ten years completely unlike any experienced in the last 30 years.

At best house prices will move in line with disposable income, or approximately 0 to 1% per year, i.e no real increase. The biggest losers in the best case scenario are negatively geared investors, who are already facing declining rental growth and will have no capital growth to cover their loss making strategy. Older homeowners or those who bought before the GFC will only have to worry about their job in terms of mortgage repayments, but most in this cohort have significant equity and/or payments in advance. Newer and first homebuyers on high loan to value ratios (LVR) will have the risk of not being able to service their loans and dip into negative territory. The banking sector will be slightly stressed with a series of corrections and counter rallies in bank stocks but will not return to their highs, with the Australian dollar pushing to 60c.

The next likely and our base case scenario is a significant correction of between 10 and 20% in nominal house prices as worse than expected unemployment shocks the economy, reducing consumer spending as household income shrinks swiftly. This feeds into further unemployment with larger cohorts unable to service a mortgage on one wage leading to a wave of forced selling, at discount. Again, older homeowners with sub 50% LVRs will be somewhat isolated from this event, although falling stock prices will significantly impact their superannuation savings, hurting those getting ready to retire. Newer homeowners will be either under stress or underwater, with some forced to sell or drastically cut back on spending. Investors face a double edged sword as those with little debt maybe able to pickup “bargains” but the majority with high debt levels will face pressure from banks to both service and close out their loans. Bank stock prices will be under extreme pressure, falling at least 25-40% from current levels as investors factor in rising bad debts against paper thin capital ratios and probable cuts to dividends. The Australian dollar would likely see a 50c level here as interest rates plummet to 1% or below.

The worst case scenario is a 30-50% decline in nominal property prices, drawn out over a long period as the economy cannot withstand a global financial shock. While their houses retain some value, the inability to sell in that long drawn out deflationary environment coupled with a devastated superannuation portfolio comprising mainly bank and service stocks (mining stocks already having been decimated so far) will wipe out older homeowners retirement plans. Newer homeowners, especially first home buyers will be completely underwater even as interest rates near zero, instilling a fear of debt that will last a lifetime. Again, cashed up investors may benefit from opportunities available but banks will have inordinately stringent lending standards thrust upon them, so any notion of negative gearing or using high LVRs to accumulate a portfolio will be out of the question as rental yield becomes the foremost measure. Negatively geared only investors will be wiped out. Here bank stocks will fall at least 50%, and possibly up to 80% from current highs as drastic capital management measures are enacted including bailouts from the Reserve Bank and no dividend payouts. The Australian dollar will find new historic lows as capital flight takes hold as fiscal deficits soar to unknown heights to stabilize the depression like conditions. It will be a very long road to recovery.

Core Strategy

The optimum strategy for hedging Australian residential property is to ride the volatility wave that will shock those institutions most exposed to the downturn: banks and the Australian dollar.

In essence, it means take a short position that profits from bank stock prices and the Australian dollar will fall more in magnitude compared to average house prices.

Why just banks and the Australian dollar? Other complementary strategies could include shorting property trusts (A-REITs), homebuilder stocks and any other companies exposed to the property bubble. The problem with execution is primarily a lack of liquidity and availability of products to take a downwards view.

The aim of the strategy is to hedge at least 50% of the fall in house prices. Given the average house price is approx. $500,000 and the base case is a 10-20% decline in value, a minimum $25,000 to $50,000 hedge or profit needs to be constructed.

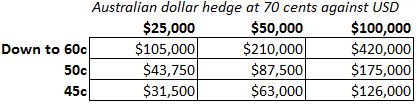

The table below illustrates the size of the short positions required against increasing declines in the value of the Australian dollar, assuming a current price of 70 cents against the US dollar.

For example, if you wanted to create a $25,000 hedge but thought the base case was the most likely scenario, where the AUDUSD only falls to 60 cents, you need to create a short position that sells $105,000 AUD. This equates to just over 1 lot, or a $100,000 bundle, which is how foreign exchange markets trade in size. Half that amount if you contend a more serious downgrade to 50 cents or double that to 2 lots or $200,000 for a larger hedge.

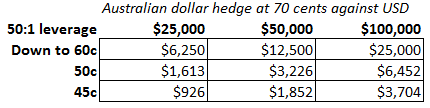

Due to the leverage involved in forex, the funds required or margin reduces to a fraction, albeit depending on your risk point of view. Assuming 50:1 leverage (double the usual 100:1), the margin required to build the hedge is as follows:

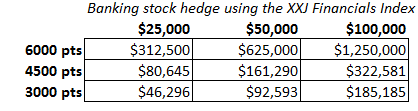

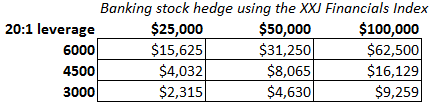

With the banks, due to the unhedged currency factor, large positions sizes are required because the technical targets are of a different magnitude:

Position sizes more than double when shorting bank stocks, but can be offset by the use of leverage, which is built in to the only products available for this strategy. The standard for most banks is 5% or 20:1 leverage, needing the follow basic margin:

The products used in both cases would be contracts for difference (CFD) or Mini warrants (bank stocks). A straight, non-leveraged short Australian dollar position can be built using the Betashares Exchange Traded Funds (ETF) in USD form. CFDs and Minis, when used as a hedge, are less risky than supposed but they do require very careful capital management.

Even though these are long term positions, with holding periods that could extend over twelve months, volatility around price will dictate larger account balance than the underlying position size. The rough rule of thumb will be approximately twice although this can be reduced over time as the position becomes more profitable. The reason for this size will be explained later.

What about options? Put options can be used to create a virtual short position in bank stocks and while they have built in leverage, they do not have any account or margin call risk because the whole price is paid when the contract is created. The main drawback with options is time decay because like an insurance premium, put options have a terminal date where they expire either “in the money” or “out of the money”, i.e worthless. They only expire in the money if the price of the underlying security, e.g bank stocks, is below the original put price at the exact terminal date. If not, the option is worthless.

That means timing and time in this trade must be near perfect, unlike CFDs or Minis, where you can “hang on” and let the trade ride out, especially if macro conditions do not degrade as quickly as expected.

Using the other products allows for some fudge factor in terms of time in the trade, but the entry itself is relatively easy to ascertain.

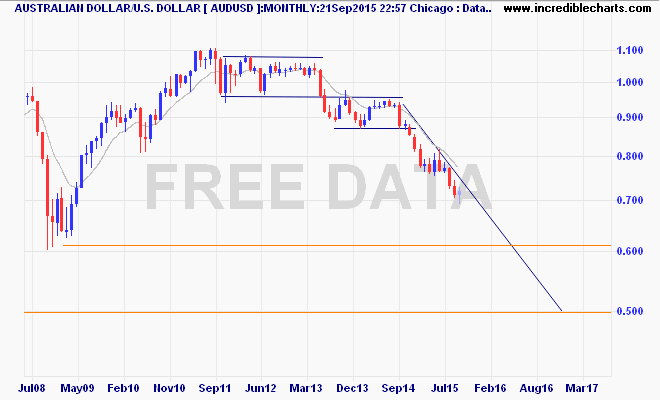

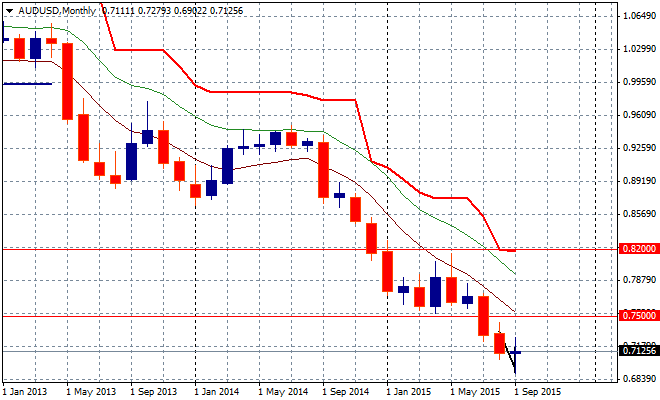

First with the Australian dollar, currently around 70 cents against the USD, the time to short is now. Additional or missed entries should be made at the break of the 60 cent level on a weekly or monthly close:

There are three types of exits to be made here and the most important is when the call has been wrong, because this will determine how much you could lose using this strategy. In the last twelve months, average monthly volatility of the Australian dollar has ranged between three and four cents. It has exceeded eight cents twice in the last ten years, once during the GFC and again during the first Greek crisis.

Therefore the first exit to make is when monthly volatility breaks out at three times higher than the current average, or approximately 12 cents ( 82 cents just above the 2015 high) as shown on the monthly chart of AUDUSD below:

This is highly unlikely as all probability points to a rebound of no higher than 75 cents with all the macro and fundamental forces pointing down. This was the major support level throughout 2015, which cracked in July as Chinese market ructions from their slowing economy spread across commodity based securities, including the Australian dollar.

A slightly more prudent entry would be to build half the hedge position now and then a second entry on a break below the key level of 70 cents. Another option is to exit on a break above the 75 cent level, but this is a very low probability.

The second exit to make is taking profit at or just above the 60 cent mark. This corresponds to the GFC lows and could form a base over several months as this nadir is absorbed and consolidated by market forces. This could also be a partial exit by reducing size by 50% or so and letting the rest ride.

The final exit is a complete rout down to 45 cents, a level not seen in over a decade before the start of the Chinese boom. This could take some time, perhaps several years and this factor needs to be considered.

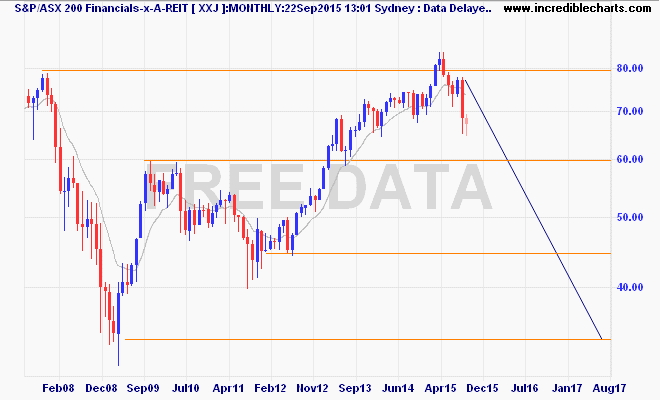

Shorting the banking sector is a similar play but entails more volatility and has some other key factors involved.

Technically, going short now in any of the banks, or if we look at them as a whole using the XXJ Financials Index (ex-property) is a higher risk, but potentially huge reward. Although the XXJ has suffered a near 25% correction from its highs, there is still a long way to fall.

The real entry should be on a weekly or monthly close below the 6000 point level, which corresponds with the $60 per share mark for Commonwealth Bank. This level wipes out all of the nominal gains in banks since the RBA started its easing cycle and equates to the temporary top on the reflation trade in 2009. A more aggressive entry could be initiated on the more local level at 6400 points but this may just be a false break due to dividend payout volatility, which is approaching in the coming months.

A subsequent entry or take profit point is the next key level at 4500 points, the lows experienced in the 2011-2012 correction and a significant fall from grace for the banking sector. As a key level it will provide ample opportunity for bargain hunters to swoop in and if combined with a likely rate cut, could see a large bounce in bank stocks, but not above the 6000 point level.

Another key entry point is if any bank announces a cut to their dividend and/or significant capital raising. This is a clear and present danger to bank capital and security and will cause a huge shock in the market, resulting in volatility that will cause all banks stocks to slump.

For the exit strategy, if the trade is wrong a loss should be taken if prices go back to above the 7900 point level, which corresponds to approx. three times monthly volatility from current prices and the former high.

Like the Australian dollar rebound, this probability is low, although a rally up to that level should not be unexpected on any rate cut by the RBA, as the market confuses a short term boost with a long term trend that goes against bank profitability.

The final exit should be undertaken at the 3000-3300 point level, at around GFC lows but this could take a year or even longer to eventuate.

Combining both approaches, by being half short AUDUSD and half short Australian banks may provide another hedge in and of itself. While the factors behind the fall in each security are identical, markets may react in other ways or through exogenous forces like a Chinese stock market rally, a temporarily falling USD or a ban on short selling of stocks.

Tailored Strategies

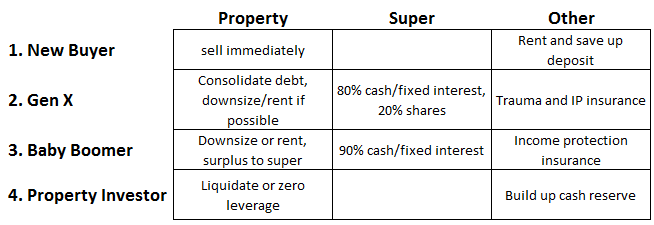

Those without surplus capital to risk, or prefer not to take the above approach still need to protect the value of their house. In this section, we’ll go over tailored strategies that fit four different types of homeowners and investors over the three probabilities outlined above.

New homeowner

A typical first home buyer just bought a house in Melbourne or Sydney at a very high LVR, possibly with only 5% down and no other wealth, apart from some meager super at hand. What to do when that equity evaporates in even the best case scenario?

A best case scenario of zero nominal increase in house prices means treading water and having a large level of debt stress throughout this period. Constant employment will be a must to service the loan and maintain equity, thus reducing labour mobility and career prospects significantly. Remember there’s more at stake here than just your deposit! This could be too big a stress to handle and can be eliminated by renting, thus saving at least 40-50% of the consumer cost of having a home and giving you a far better chance of building real equity.

The optimum strategy is simple – sell the house, discharge the mortgage and rent a property. Selling near or at the top of the market and having the ability to do so is a far better opportunity than the clear threat of not being able to sell at all during the downturn or outright collapse, when everyone is trying sell. The worst position to be in is having no home, but still having to pay off a mortgage in negative equity as the firesale price minus transaction costs do not cover your initial mortgage. The main weakness to this strategy is the likelihood of wiping out any built up equity in transaction costs. This temporary setback must be weighed against the risk of literally throwing interest money down the sink over the next five to ten years as your contemporaries who rent are able to both save money and move around looking for employment, including overseas.

Gen X with mid LVR, but sizeable mortgage requiring dual salaries to service

This cohort has bought in the last ten years or so, likely to have a small family and is dependent on two salaries to both service the mortgage and pay for burgeoning education and childcare costs. This is the hardest strategy to ascertain for a variety of reasons, mostly psychological.

Simply selling and walking away may not be the best option, particularly finding suitable rental accommodation within the same area for schools and employment, let alone the emotional capital. The decision to remain a mortgage holder must be weighed against other financial issues, namely credit card and other personal debt in the face of higher probability of unemployment. Consolidating higher interest personal debt into the home loan and paying this down as mortgage rates find a near bottom (approx. 3 to 3.5% standard variable) will cushion the equity blow and allow for better cash flow.

Increasing insurance options, including both trauma and income protection should be part of this plan, in addition to rebalancing super away from equities and into cash/fixed interest. If selling the home is an option, buying a downsized property straight away or after a period of renting as options open up and prices fall should be highly considered. The key point is to protect the equity within the home and the ability to service it. This will include substantial reductions in discretionary spending to plow back into the home loan.

Preservation is key here due the timing of career/family, where unlike a younger homeowner, the peak earning years are (supposedly) only just around the corner.

Baby Boomers a few years from retirement, most wealth in home with low/zero mortgage

While this may be considered the least at risk cohort, the opposite is true. Most baby boomers either own their home outright or have a small mortgage, yet the average superannuation balance at retirement doesn’t exceed $200,000, so that is where almost all their “wealth” literally resides. A fall in house prices, which will be correlated with a stock market rout, will see both values plummet. This is the time to downsize before you are forced to. While this must be weighed against the emotional capital of selling the family home, you must think of the future instead of the past and create a real nest egg, and not one made of bricks and mortar.

The optimum strategy is to sell the family home, buy outright or rent a smaller house, pay off all debts and place the excess in cash and/or make additional contributions to superannuation. With super, asset allocation must change to that of low risk, including cash and bonds, with only a very small percentage – less than 10% if possible – in international shares and domestic, but AUD exposed companies. Income protection insurance is vital for this cohort, as their ability to earn an income is key in the years remaining to retirement. This can be paid in super, or outside where its tax deductible too.

Property investor with negatively geared portfolio

The most exposed to financial ruin, property investors in all cases need to quickly turn their portfolios into zero leverage or straight cash, depending on overall debt. There is no place for negative gearing in the years ahead as capital gains are off the table and income cannot be wasted on paying a dividend to your property. Rental yield will become the key determinant of investing in property.

But this doesn’t mean take property off the table. Buyers with large cash reserves will be the only investors or homeowners able to get any loans in the post-crash scenario, with LVR’s probably brought back down to 75% or even half due to stricter if late macroprudential controls.

Conversely, the investor must be prepared for all kinds of regulatory “juicing” of the property market, including possible selling controls, ultra low interest rates and incentives for first home buyers. The market will be increasingly controlled and intervened by regulators and authorities wanting to re-ignite the property bubble.

Focusing on positive yield, which should be well in excess of that available in cash, bonds and most other securities, even stocks, will be in the property investors favour. Capital gains will come eventually, but only after a very long period, and remember that we are all dead in the long run.

Disclaimer: This report is not a recommendation or advice to buy or sell any particular product or service. It does not take into account the specific needs of an investor, who needs to seek professional advice from a qualified financial adviser. Contracts for difference (CFDs) are leveraged products where you can lose more than your initial deposit.

Update: Due to the feedback from Members, a follow up report addressing the details, alternatives and other discussions around this report will be published shortly. Thank you for your feedback!