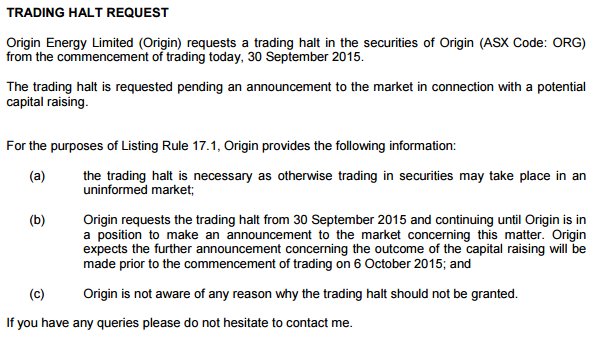

From the ASX:

Origin says it is undertaking “cash preservation” to preserve its credit rating. It has also cut it dividend for 2016/17and will sell $800 million in assets, aiming to reduce its debt burden to $9 billion by the end of FY17. The raising is at, wait for it, a 34% discount to the closing price at a disastrous $4 per share.

For what it’s worth, any fundie looking at this $2.5 billion raising should consider that the APLNG project will never see a return on its capital, is at intensifying risk of seeing a return on a cash basis only far into the future and is at severe risk of contract default or re-negotiation in its underpinning Sinopec supply contract.

$2.5 billion is not enough and won’t be the last.

Advertisement