Back in April, the Paris-based Financial Action Task Force (FATF) on money laundering released its scathing report on Australia, which found that Australian residential property is a haven for international money laundering, particularly from China. The report also recommended that Australia implement counter-measures to ensure that real estate agents, lawyers and accountants facilitating real estate transactions are captured by the regulatory net:

Australia remains at significant risk of an inflow of illicit funds from persons in foreign countries who find Australia a suitable place to hold and invest funds, including in real estate… Australia is seen as an attractive destination for foreign proceeds, particularly corruption-related proceeds flowing into real estate…

Large amounts are suspected to be laundered out of China into the Australian real estate market. China and other countries within the Asia-Pacific region were also seen as likely sources of corruption proceeds that are laundered in Australia…

Of great concern is that Australia has not brought real estate agents within the AML/CTF [counter-terrorism finance] regime…

Most DNFBPs, including real estate agents and legal professionals, are… not subject to AML/CTF controls or suspicious transaction reporting obligations, even though they are highlighted as being high-risk for ML activities…

The authorities should place more emphasis on pursuing ML investigations and prosecutions at the federal as well at the State/Territory level.

Australia’s draft rules on anti-money laundering (AML) affecting real estate were released in 2007, but have been all but ignored by the federal government ever since. By contrast, Australia’s financial and gambling industries have been subjected to AML rules.

Fancy that. If somebody wants to set up an account to place a $10 bet at Sportsbet, or invest $1,000 into a managed fund, then they must provide sufficient identification under the Anti-Money Laundering and Counter-Terrorism Financing (AML) Act. But if they want to launder $2 million through an Australian home, few questions are asked.

Not surprisingly, then, dodgy foreign money has gushed into Australia’s homes, helping to price young Australians out of home ownership.

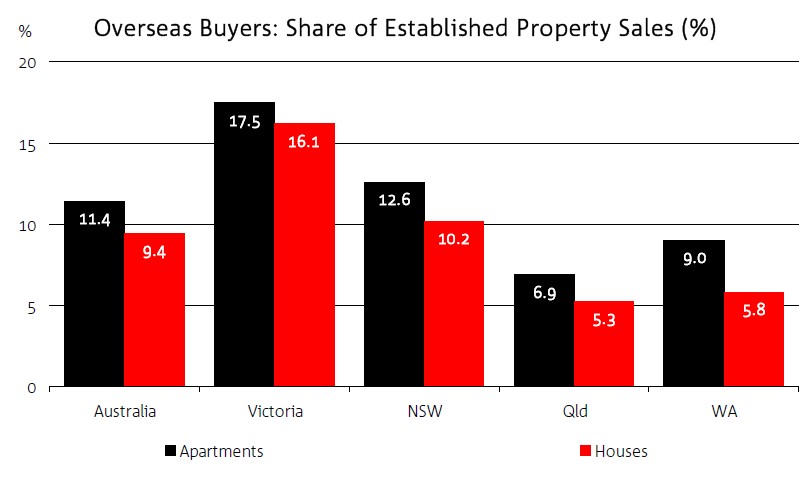

Indeed, the huge share of established homes selling to foreign buyers, contrary to Australia’s foreign investment regime, suggests the problem is rife, particularly in Melbourne and Sydney:

As noted last month by Nathan Lynch, Head Regulatory Analyst for Australia & New Zealand at Thomson Reuters, Australia’s AML regulator, AUSTRAC, is hamstrung in what it could do in relation to real estate under the AML Act. There is no obligation on professional facilitators, such as real estate agents, lawyers or accountants, to report suspicious transactions, which is in contrast to Australia’s banks, casinos and bullion dealers:

The FATF report identified real estate as a “high risk” sector for laundering and said AUSTRAC had little power over several crucial industries, including real estate agents, accountants and lawyers. The assessors found that offshore organised crime groups were using “professional facilitators” to launder their criminal proceeds through Australian real estate. Australian housing is viewed across Asia as an attractive vehicle for parking illicit funds, particularly among corrupt officials, the report found…

AUSTRAC’s surveillance efforts are also being frustrated by the fact that money launderers will often use unregulated entities as a “first point of contact” to help disguise their source of funds. If a criminal makes a suspicious cash deposit into a real estate agent or lawyer’s trust account, for example, the suspicious transaction is not required to be reported to AUSTRAC. Reporting entities, such as banks, are required to report transactions of this type within three business days of forming a suspicion. Lawyers are only required to report threshold transactions under the legacy Financial Transaction Reports Act 1988, not suspicious matters, while real estate agents have no reporting obligations.

“One thing that we consider is that lawyers, accountants and real estate agents are often a first point of engagement for clients — particularly for clients and customers who are looking to establish a company or a trust. They don’t go to the bank first, they go to someone who is capable of setting that up for them,” [Bradley Brown, acting national manager for strategic intelligence and policy at AUSTRAC] said.

Tightening Australia’s anti-money laundering rules makes perfect macro-economic sense, since it would take the heat out of housing, lower financial stability risks, and allow the RBA to lower interest rates further than would otherwise be possible, putting downward pressure on the dollar.

One wonders how long the Australian Government can continue to ignore this issue in light of the growing international pressure and financial stability risks.