In a superb case of sell side wackness, Citi has today downgraded ORG to neutral:

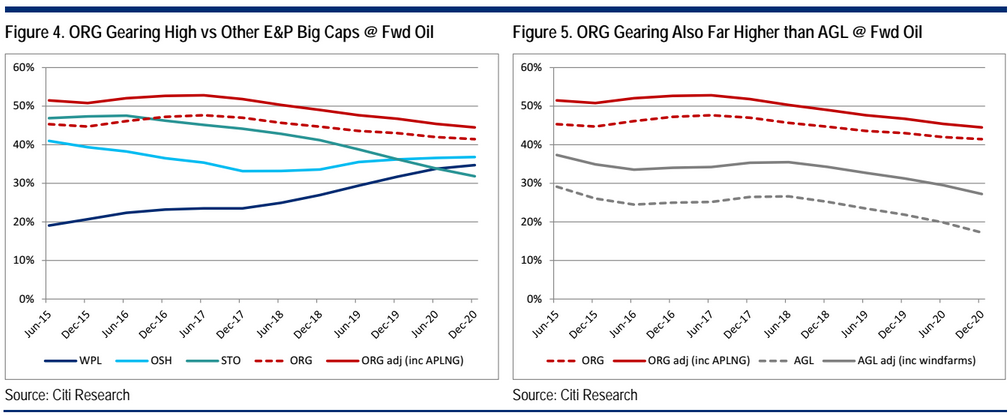

Company risk has increased, premium to peers unfair — While investors have long been focused on the outlook for STO’s balance sheet we think that the outlook for ORG deserves just as much if not more attention from investors. Its credit rating is 1 notch below STO and AGL, but with materially higher gearing and unlike STO no active plan to fix the balance sheet. ORG’s Energy Markets earnings growth outlook is flat and the Contact sales increases leverage to oil and therefore volatility.

Credit Metrics challenged but can be protected — We think that ORG wishes to remain investment grade but we don’t think that a rating downgrade would be catastrophic to the electricity business (we explain why inside). We also think ORG can retain its credit rating from APLNG raising external debt to refund shareholders.

But gearing to remain stubbornly high — ORG’s gearing will likely remain above 45% inc APLNG out to 2020, above E&P peers (av 31% in FY17) and Utility peers (av 26% in FY17). De-gearing is very slow at fwd oil prices, exacerbated by ~A$200m pa cashflow drag from forward oil sales being repaid over 6 years from FY16.

So how can ORG fix its balance sheet? — We think ORG could look to sell a small 5% interest in APLNG, Perth basin gas assets and/or could look to monetize infrastructure. However, we think that with ~A$2.5-6bn of disposals required to bring gearing down to a more sustainable 30-40% by the end of FY18 asset sales are unlikely to be enough, with an equity raising a risk, absent of higher oil prices.

Downgrade to Neutral, TP 22% lower to A$7.54/shr on higher risk profile.

It’s at $7 already, for heaven’s sake, and falling fast. Who is going to buy 5% of APLNG with its single contract risk? Hint: nobody.

The real story here is that APLNG is next to worthless with its debt load and at some point ORG will have to recognise the fact.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.