RIO has done itself proud in the its mid year update:

The FTSE 100-listed miner reported a pretax profit of USD1.74 billion in the first half of 2015, less than a third of the USD6.09 billion profit made a year earlier, as revenue fell to USD17.98 billion from USD24.33 billion.

Pretax profit before finance costs came in at USD3.66 billion, also considerably down from the USD5.88 billion profit a year earlier.

Earnings before exceptional items fell to USD2.92 billion in the first half of 2015, compared to USD5.11 billion. That beat analyst expectations, which were expecting earnings to come in at around USD2.43 billion, according to a consensus provided by the company.

Rio Tinto said the fall in commodity prices in the first half of 2015 decreased its earnings before exceptional items by USD3.62 billion compared to a year earlier.

Despite the dramatic fall in earnings, Rio Tinto stuck with its progressive dividend policy, increasing the interim dividend by 12% to 107.5 cents per share from 96.0 cents per share.

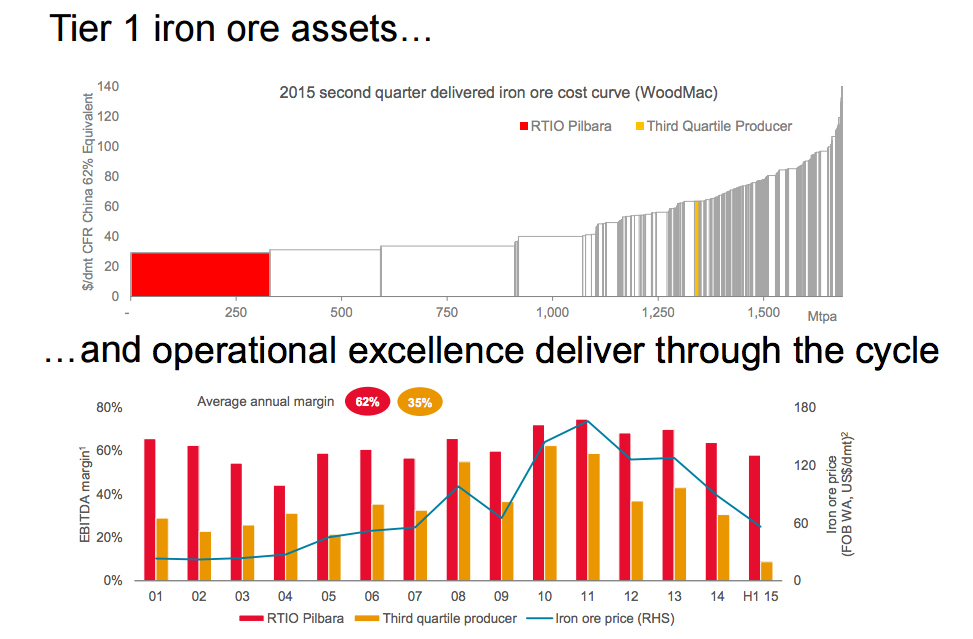

The highlights were good free cash flow, very low iron ore C1 cost at $16.20, a solid rebound in aluminium earnings to $793 million, good cost savings and more coming, good capex cuts and rising dividends.

All-in iron ore breakevens appear to have dropped all the way the $30 though margins continue to fall:

‘

It’s dynamic and excellent management in tough times. Shame it’s almost completely irrelevant.

Good God, why, you demand? And the answer is the same as always, because iron ore is toast.

RIO is simply leading everyone and everything on the cost curve further down and as costs come out they will be recycled back to Chinese customers as cheaper prices. The glut hasn’t changed. The outlook for it is no better. And the fate of RIO’s share price and ultimately dividend is unchanged as well.

RIO is an Olympic gold medal swimmer stroking against a debris filled tsunami. That is why it’s share price barely budged in London and any rally here is only another chance to build up more shorts.