The Reserve Bank of Australia’s (RBA) Statement on Monetary Policy, released on Friday, contained an interesting extract examining the forces behind Australia’s low wages growth:

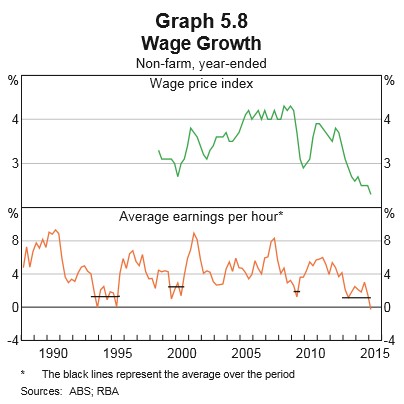

Labour cost pressures are weak and most indicators of wage growth have declined further in recent quarters. The Wage Price Index (WPI) increased by 0.5 per cent in the March quarter and by 2.3 per cent over the year – the lowest annual pace since the index was first published in the late 1990s (Graph 5.8). Other wage measures, such as average earnings per hour, suggest that the recent period has been the most protracted episode of low wage growth since the early 1990s.

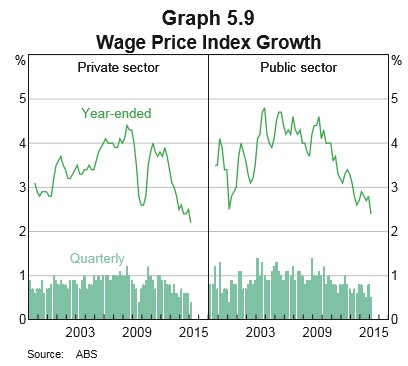

Low wage growth continues to be broad based across sectors, industries and states. In the March quarter, the private sector WPI recorded its lowest quarterly pace of growth since the global financial crisis, to be 2.2 per cent higher in year-ended terms (Graph 5.9).

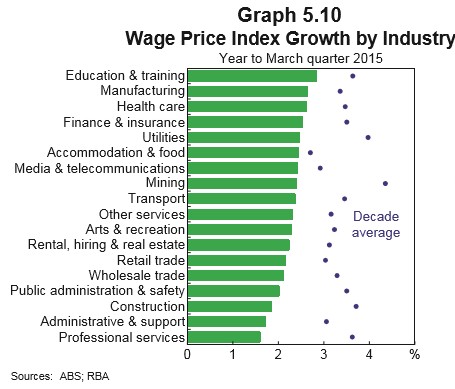

Public sector wage growth was also low at 2.4 per cent over the year. Public sector wage growth has been particularly low in the Australian Capital Territory, although this is partly temporary as many federal public sector workers have not had wage increases since their enterprise bargaining agreements expired last year. New agreements are now being reached in some cases, although negotiations are ongoing for others. Nationally, wage growth has continued to decline in a range of industries, and all industries have experienced wage growth below their decade averages (Graph 5.10).

According to business liaison and surveys of firms and union officials, growth in wages is widely expected to remain low over the year ahead.

Several factors explain the decline in wage growth, including an increase in spare capacity in the labour market, low inflation expectations, the substantial decline in the terms of trade over the past couple of years and the need for the real exchange rate to adjust to improve international competitiveness. Nevertheless, the extent of the decline in wage growth has been unusually large relative to changes in measures of spare capacity in the labour market, such as the unemployment rate. Compared with previous episodes, increased labour market flexibility may have provided firms with more scope to adjust wages in response to a given change in demand for their goods and services. In any case, very low wage growth appears to have contributed to more employment than would otherwise have been the case.

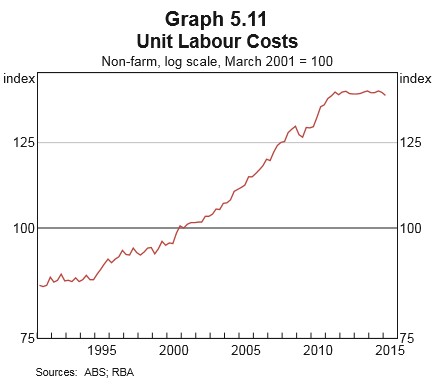

Unit labour costs, which adjust wage growth for changes in labour productivity, have been little changed for almost four years, as productivity growth has broadly matched earnings growth (Graph 5.11). The fact that unit labour costs have not changed significantly is assisting with the process of the economy adjusting to the lower terms of trade. There was little growth in measured labour productivity over the year to the March quarter, although average productivity growth has been higher since the start of 2011 than it was over much of the previous decade. Information from liaison suggests that firms continue to focus on cutting costs and improving productivity.

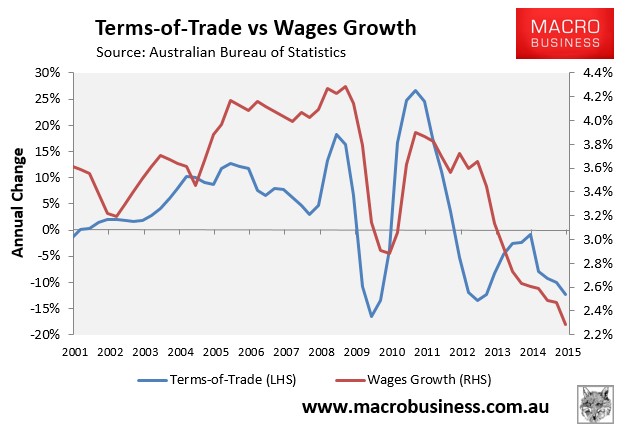

For mine, the falling terms-of-trade best explains Australia’s low wages growth (see next chart).

Advertisement

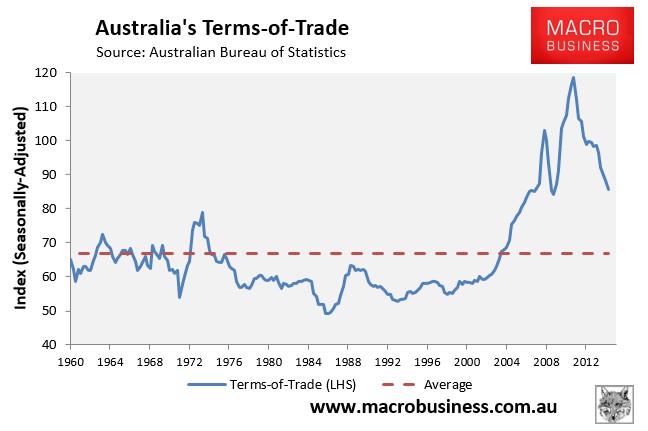

And with the terms-of-trade still way above historical norms (see next chart), and expected to continue falling, wages growth will remain anaemic.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.