In this week’s email newsletter, available for free by signing-up here, SQM Research’s managing director, Louis Christopher, provides a nice summary of the state-of-play of the Australian housing market in the wake of the recent changes to investor mortgage policies by the Australian banks:

Over the last three weeks. And in the last week in particular, there have been some key announcements that will likely have a meaningful impact upon the housing market. The screws have been further tightened and this time we think they will have an impact. To recap the major changes include:

• A requirement for banks to hold 2% more capital (compared to risk weighted assets).

• A requirement for banks to lift risk weights on home loans, meaning the banks will not be able to leverage as much from their home loan assets as they were before.

Banks have responded by:

• Announcing capital raises

• Lifting interest rates on investment property loans

•Reducing loan to value ratios on investment property loans and locations considered higher risk

• Increasing the servicing requirements (e.g A loan service test on a higher theoretical interest rate).

• Not allowing tax benefits from negative gearing to be used as income.

Clearly the changes will knock out most of the weaker borrowers, which is what the changes are designed to do, besides strengthen the balance sheets of the banks. But will it move existing property investors to the exits?

The cumulative effect of these changes will now most likely dampen demand from property investors. The announcement last week of interest rate increases was probably the final nail. Indeed, trusted sources on the ground including agents and mortgage brokers in Sydney are informing me of would-be buyers now holding back.

We also note the recent decline in Sydney auction clearance rates to just back below 80%. Nevertheless clearance rates in the mid to high 70’s is still suggestive of strong market.

It should also be noted that SQM expects total residential property listings have surged in July, though the final result will not be known until early August.

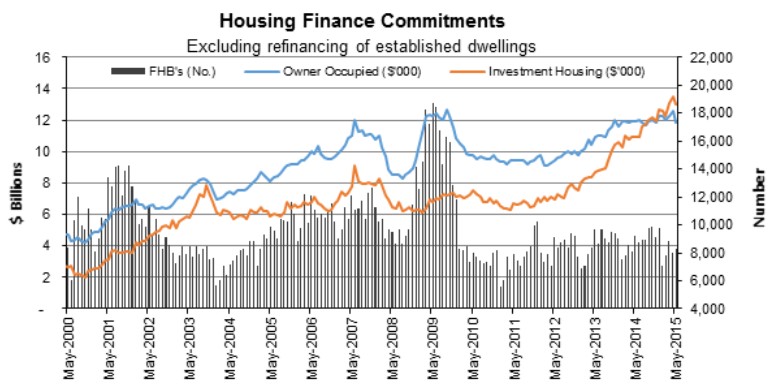

As we know the recovery in the housing market, particularly for Sydney has been investor driven. It’s a good time to re-publish the following chart, which does clearly illustrate how investor have dominated this recovery.

The problem is, property investors can be a fickle bunch. A number of them are momentum driven. Buy when the market is moving higher and sell when the market is heading lower. Forget about the fundamentals and the emotional attachment. It is the capital gain and preservation of that gain that counts. Contrast this with first home buyers and owner occupiers who tend to not care (as much) for the market ups and downs. They tend to be longer term holders. They tend to sell and buy on an upgrade/downgrade or when servicing improves/deteriorates.This makes for a market they may well be more volatile than previous cycles.

Even so, is there enough here to create a full blown crash? No way. We would still need to see a lot more action from the banking sector than these initiatives before that happens. I believe rates would need to go up by at least 1.5% and at a time when there is some type of massive supply overhang on new stock. Neither seems likely at this point in time.

Needless to say the probabilities have now rapidly increased of a housing market slowdown which could be commencing now.

Overall, a good assessment that is hard to disagree with. There is also the prospect that the new stricter foreign ownership regime, which come into effect from December 2015, could materially dampen foreign buyer demand.

The point I will add is that this “soft landing scenario” has a potential flaw. Employment is likely to take a big hit over the next two years as mining investment tumbles, the car industry shuts, and the dwelling construction boom reverses. Thus the moment house prices stall, underlying economic weakness will manifest. In such an economic context, a housing “soft landing” could turn hard rather quickly.

Advertisement

Further, there is the reasonable likelihood that an external shock will manifest sometime over the next two years, pushing-up bank funding costs; although the exact timing and cause of such an event is impossible to predict.

On another minor note, I disagree with Louis that Australian housing is in “recovery”, given house prices nationally are at all-time highs in real (inflation-adjusted) terms, against incomes, and against rents.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.