Speaking after the benchmark price for iron ore fell to a record-low US$44.10 on Thursday, Li Xinchuang, president of the China Metallurgical Industry Planning Association, said weak demand from property and infrastructure construction would shrink steel output 2 per cent. Production may fall even more than that if exports falter because a softening global economy.

The iron panic is on. From the AFR:

…The dramatic reversal in China’s steel output comes as analysts including Xi Xiangchun, the chief information officer at research group Mysteel cautioned the worst was not over for iron ore.

“China’s steel demand is still declining, steel mills are in the red and supply is going up. Why would the price go up?” he said. “We haven’t seen the bottom yet. The iron ore price will see a continuous fall this year and next. We might see some rebounds in between but the general trend is down.”

Correct! And from the SMH:

Now economists are warning that Commonwealth government tax receipts could shrink by another $6.5 billion over the next two years – with implications for federal budget deficit – if the iron ore price remains near its record low.

Westpac senior economist Justin Smirk says the record-low price, at $US44 a tonne, is actually worth far less than the $US48 a tonne assumption that underpins key economic forecasts in the federal budget.

He says the real iron ore price is closer to $US36 a tonne, once freight costs and exchange rates are taken into account, with serious ramifications for Commonwealth tax receipts and the deficit.

That also means that a gloomy theoretical scenario in the budget papers – showing a multi-billion dollar hit to revenues if iron ore prices lose $US10 a tonne in value – is already threatening to come true.

But that pales next to the WA calamity, from the ABC:

The drop in the iron ore price to levels below Western Australian Government forecasts spells trouble for the state ahead of a decision on a possible ratings downgrade, analysts have warned.

Overnight the iron ore price dropped below the US$47.50 per tonne forecast in the 2015-16 WA budget, to a 10-year low of $US44.10 a tonne.

Each US$1 decline in the iron ore price puts a $70 million hole in the state budget, with falls to levels far below the Government’s forecast last year leading to a large deficit.

Standard and Poor’s placed WA’s AA+ credit rating on negative watch in April, with a decision on whether it will be downgraded now expected imminently.

“This will be absolutely critical to what Standard and Poor’s looks at because this is so important to the budget of Western Australia,” business commentator Tim Treadgold said.

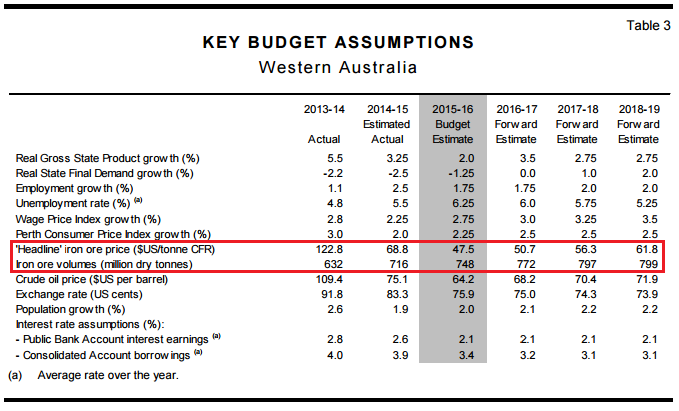

The downgrades for WA will be far worse yet. Here is the Budget:

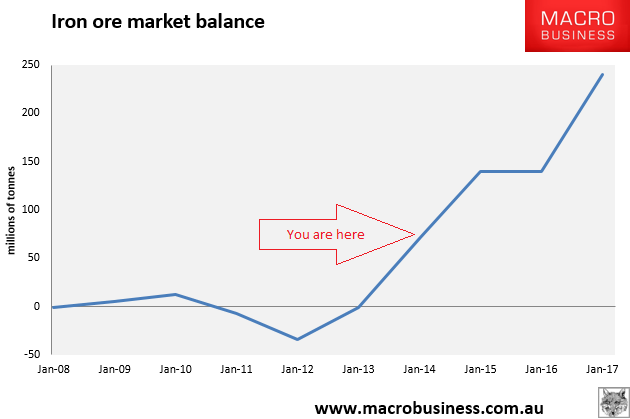

Look at the forward prices. Yet iron ore is going to fall to a point of next-to-zero profits for miners and next-to-zero revenue for the Budget for the next 3-5 years. The glut has barely begun:

Dirt is gonna be cheap, cheaper and cheapest! So you can safely ignore this crud from Bloomie:

“It has to bounce,” Atlas Iron Ltd. Managing Director David Flanagan said in an interview in Melbourne on Thursday before the price data was released. “It’s not so much a reflection of the physical trade any more, it’s about confidence and fear and happiness about the future.”

Atlas, which closed and then reopened its mines this year as iron ore seesawed between bear and bull markets, is prepared to halt its mines again, said Flanagan. As Atlas sells some of its output forward, the company’s new point for suspension may be under $40 a ton on a realized basis, he said.

And the AFR:

“The new normal is volatility,” he told Fairfax Media in Melbourne. “We could see iron ore trade in a range back up to $US70, and how low could it go? – it might go to $US40.”

Does that chart look like it’s all sentiment to you, or that when AGO does finally shut its doors for good its absent 15 million tonnes will matter at all? No. Volatility will persist while the shakeout does but eventually the market will calm down. The real price we need to reach is low enough not to blow AGO’s hand full of dirt aside but to put FMG’s 160 million tonnes out of business. That’s going to be around $20 for while and then rise to perhaps $30 when its restructured and much smaller or gone.

That brings us to the majors ridiculous dividends, also from the AFR:

BHP and Rio both adopt what they describe as progressive dividend policies, which just means the objective is to match or better the previous dividend. The strategies were largely in response to investor demands that the diversified miners introduce some capital discipline after painful write-downs.

…Arnhem’s Neil Boyd-Clark said the dividend strategies had been questioned extensively.

“We have been consistently advised by both companies that UK investors in particular are very supportive of their dividend policies,” he said.

“The idea of a progressive dividend policy for companies operating in cyclical industries is somewhat anathema to Arnhem. However, the best time to make a change is clearly not when you are forced to do so due to a lack of alternative options, but rather when you are in a position of strength.”

Give that man a cigar. The dividends are doomed. Cash flow from iron ore is going to dry up completely. The gap will be filled by debt for a while but when there’s enough cover, the next global shakeout perhaps, the dividends will be junked.

As the media fixates on the latest gyrations in price let us briefly recall how we got ourselves into this position. It was us that:

And as it all goes into reverse, what comes next do you reckon?