From Capital Economics:

All the signs are that the four largest producers will continue to ramp up output (see Chart 4) in an effort to use higher volumes to offset lower values. The market will remain oversupplied this year, despite our forecast of a 15% drop in China’s production. However, by next year, we expect a more visible supply response to low prices. This will coincide with a somewhat stronger global economy, which should reduce the surplus in the market. We would not rule out deeper falls in the iron ore price over the next couple of months but are retaining our end-2015 forecast of $45 per tonne. We expect a modest recovery to around $55 by the end of next year as higher-cost output leaves the market.

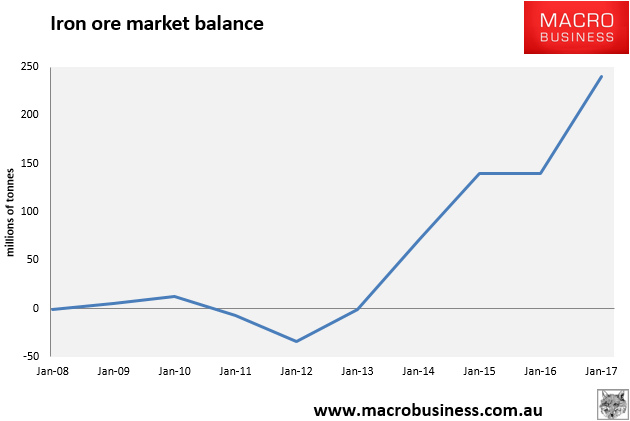

Stronger global growth? Would that be on Grexit, slowing China or US rate rises? As for an iron ore rebound next year, phooey. Nor the year after as supply continues to outstrip demand, here’s my chart: