The Grattan Institute has released a working paper entitled Property Taxes, which makes a welcome addition to the debate about how to best reform Australia’s tax system.

The paper correctly notes that property taxes – which are levied on the value of property holdings – are the most efficient taxes available to the states, since they are immobile and do little to change incentives to work, save and invest.

It argues that a low-rate, broad-based property levy using the council rates base could raise about $7 billion a year for state and territory governments through an annual levy of just $2 for every $1000 of unimproved land value, or $1 for every $1000 of capital improved property value.

Under such a regime, a homeowner would pay a levy of just $772 a year on the median-priced Sydney home, valued at $772,000, or $560 a year on the median priced Melbourne home valued at $560,000. People with low incomes and no wealth would pay nothing, whereas low-income retirees with high value houses could defer paying the levy until their house is sold.

Advertisement

The paper also proposes that higher property taxes be used to fund the reduction and eventual abolition of state stamp duties on property, which are are among the most inefficient and inequitable taxes available to states, and their revenues are inherently volatile.

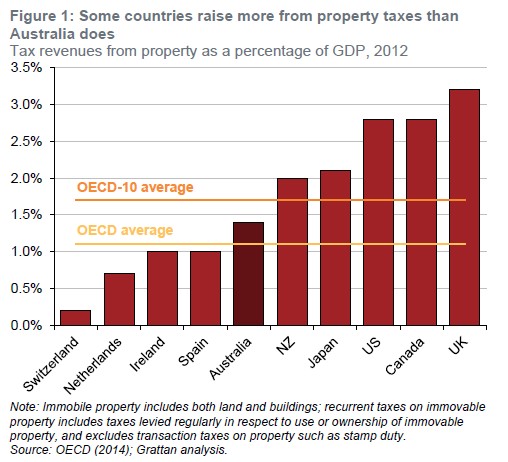

Despite frequent claims from the property lobby, Grattan argues that property taxes in Australia are actually relatively low – at least when compared against the major developed nations (see next chart).

Advertisement

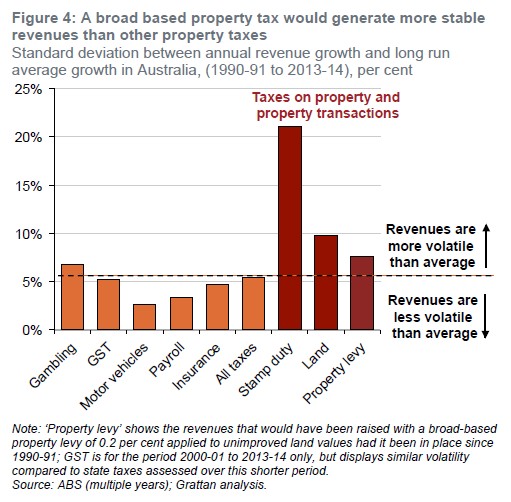

However, revenue from stamp duties is highly volatile, which makes budgeting more complex (see next chart).

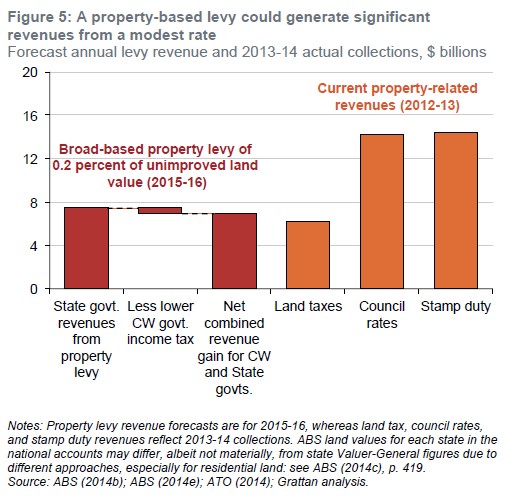

Moreover, rather than levying huge bills on the small minority of people that purchase a home in a given year, a property-based levy could generate significant revenues from a modest rate, thereby spreading the tax burden more fairly (see next chart).

Advertisement

Grattan also argues that a property-based tax levied on the unimproved land value would have no impact on rents:

Potential buyers of property will reduce how much they are willing to pay by the future cost of property tax payments. Therefore the tax liability is capitalised into the property value. For example, a 0.2 per cent levy on unimproved land values would be expected to reduce land values by between 3 and 6 per cent.

A levy on unimproved land values would have no impact on rents. If a landowner tried to pass on the tax by charging higher rents, some people would decide not to rent, thereby lowering rental demand and causing rents to fall back again.

Advertisement

However, a tax levied on capital improved values could increase rents very slightly by marginally reducing housing supply:

A levy on capital improved property values might lead to small rent rises, since it would discourage some investment in new improvements and therefore affect the supply of housing. Over time, landlords are likely to pass on to renters some of the additional costs that the levy imposes on improvements. Yet as Figure 9 shows, the impact on rents is likely to be small as the levy would have only a very small impact on the returns that accrue from investing in new improvements.

I won’t go over all the reasons why shifting the states’ tax base from stamp duties to property-based taxes is a good idea, since these were explained on Monday.

Advertisement

What I will say is that a tax based on the unimproved land value is far more efficient than one based on the capital improved value, since it would not discourage construction.

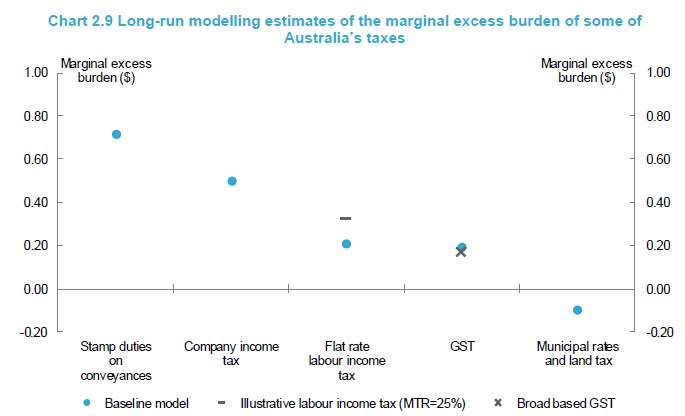

Such a tax would also provide the added benefit of creating positive efficiencies as money raised from foreign and domestic landowners is spent entirely on domestic households. As noted by recent Australian Treasury modelling:

… broad-based land taxes, such as municipal rates, have a low economic cost (Chart 2.9). This is because land is immobile (unlike other capital) and cannot be moved or varied to avoid tax. The model applies this assumption to both domestic and foreign ownership of land. Land taxes paid by foreign and domestic landowners are only redistributed to the domestic households, providing a benefit to Australian households and generating a negative marginal excess burden for a broad-based land tax shown in the chart.

Advertisement

Overall, the Grattan Institute has produced an excellent piece of research that provides a blueprint for the reform of state taxes. Let’s hope it gains the attention that it deserves, rather than a load of negative articles published in the Domain section of Fairfax.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.