During Howard’s second and third terms, he oversaw a huge expansion of Australia’s migration program based on permanent and temporary entry. Increasingly temporary and student entry became the main paths to permanent migration…

It may be true that a temporary foreign worker takes a job that otherwise may have gone to a local — even to a union member — but that foreign worker creates demand, which generates more employment. They need to be housed, fed and supplied with the countless consumer goods and services that keep the economy turning. Numerous economic studies, including by the Productivity Commission, have shown migration programs create at least as many jobs as they displace…

During the global financial crisis, unions called on the Rudd government to cancel the temporary migration program, but it continued at an elevated rate, as did the overall migration program through 2009, reaching a record 310,000 people in that year…

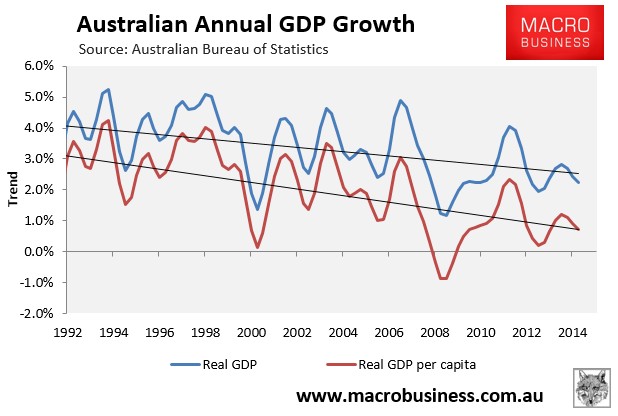

Australia had quite a steep recession in per-capita terms — output per person fell by 2.4 per cent.

However, a retailer who is selling less to every customer will not lay off staff if more people are coming through the door.

The influx of migration stopped unemployment rising higher and a genuine recession…

This elasticity in the labour force — with the size of the temporary workforce ebbing and flowing according to labour demand — helped Australia to get through the unprecedented terms of trade boom without inflation, saw it sail through the GFC without recession and is helping it to adjust now to a slowdown in the economy that in earlier times would have seen unemployment rise far higher.

Let’s dissect Uren’s arguments one-by-one.

First, the claim that “foreign worker creates demand, which generates more employment. They need to be housed, fed and supplied with the countless consumer goods and services that keep the economy turning”?

It is true that growing the population is an easy way for businesses to sell more goods and services. Immigration also gives businesses access to lower cost workers. And there’s less need to become more efficient when your customer base is growing inexorably. Rather, just sit back and watch the profits flow.

Take, for example, Australia’s banks, which get the double bonus of not just having more consumers to sell debt to, but also extra demand for housing, which helps to support house prices and their loan collateral, especially given the urban consolidation policies operated by Australia’s states.

But what is completely missing from Uren’s analysis is that while the big end of town is a clear winner from rapid population growth, it doesn’t wear any of the costs. That is borne by everyone else.

It is you and I that will be forced to spend more time in traffic jams as Australia’s infrastructure – already straining after a decade of rampant immigration – fails to keep up with population growth.

It is you and I that will be called upon to pay for expensive new infrastructure (e.g. roads, rail and desalination plants) in a futile bid support the rapidly growing population.

It is our children that will be required to live in smaller and more expensive housing, often further away from the CBD, as more people flood into our major capital cities.

And it is our children that will be called upon to once again ramp-up the immigration intake once the current batch of migrants grows old and needs support – the very definition of a ponzi scheme.

Where is the acknowledgement of these costs from Uren, or the admission that rapid immigration can actually lower productivity by diverting investment away from productive areas (see my previous post)?

Uren also seems to believe that the extra spending on imported goods and further blowing-out the current account deficit is somehow good for the economy.

Next, there’s Uren’s claim that:

During the global financial crisis… Australia had quite a steep recession in per-capita terms — output per person fell by 2.4 per cent.

However, a retailer who is selling less to every customer will not lay off staff if more people are coming through the door.

The influx of migration stopped unemployment rising higher and a genuine recession.

The extra migrants may have boosted demand, but they also boosted labour supply, so their impact on overall unemployment is highly debatable. Indeed, the RBA last week acknowledged that falling immigration has held the unemployment rate down. So how does it follow that lifting immigration during the GFC also lowered unemployment?

At least Uren has acknowledged that Australia did in fact experience a recession in per capita terms during the GFC. In fact, per capita growth has been trending down strongly:

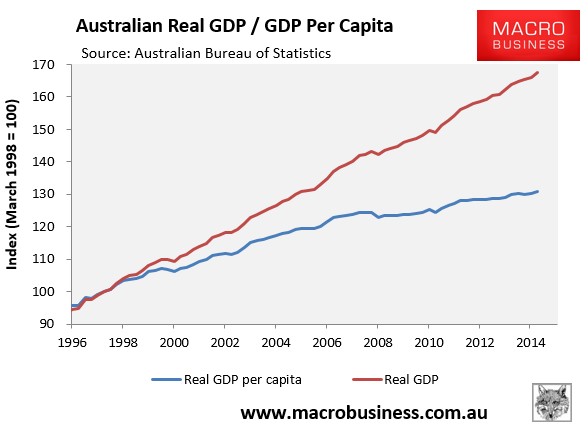

And the main thing supporting headline GDP growth is high immigration.

Indeed, since the GFC, 70% of Australia’s growth in headline GDP has come from growing the population, rather than improved productivity:

Effectively Australia’s high immigration program has maintained the illusion of growth. But what is the point of growing the economic pie if everyone’s share of that pie is not increasing sufficiently?

Finally, what do we make of Uren’s claim that:

This elasticity in the labour force — with the size of the temporary workforce ebbing and flowing according to labour demand — helped Australia to get through the unprecedented terms of trade boom without inflation, saw it sail through the GFC without recession and is helping it to adjust now to a slowdown in the economy that in earlier times would have seen unemployment rise far higher.

“Helped Australia to get through the unprecedented terms of trade boom without inflation”. Nope.

When infrastructure and housing investment fails to keep up with population growth, it places upward pressure on inflation, requiring higher interest rates, which can then damage productive sectors of the economy. As explained in a 2011 speech by the Reserve Bank of Australia’s Phil Lowe (summarised here), these factors were certainly in play in the late-2000s, when rapid population growth placed upward pressure on rents, as well as caused a big surge in utilities prices as the capacity of the system struggled to keep pace with the growing demand, requiring costly new investments.

“Saw it sail through the GFC without recession”. Not in per capita terms, which is what matters to the average Australian.

“Is helping it to adjust now to a slowdown in the economy that in earlier times would have seen unemployment rise far higher”. Absolutely, which is exactly what lower immigration does. So why did you claim earlier that “the influx of migration stopped unemployment rising” during the GFC? You have contradicted yourself, Mr Uren.

While not mentioned by Uren, I will also add once again that Australia earns its way in the world mainly by selling its fixed mineral resources (e.g. iron ore, coal, natural gas, and gold). More people means less resources per capita. A growing population also means that we must deplete our mineral resources faster, just to maintain a constant standard of living.

It’s about time that Australia’s economists and policy makers acknowledged that high immigration is not an economic bonanza, and is in fact more likely to damage productivity and living standards. Ross Gittins has done so, as has the The Australia Institute’s chief economist, Richard Denniss.

If all Australia is doing is growing for growth’s sake, pushing against infrastructure bottlenecks, diluting our fixed endowment of minerals resources, and failing to raise the living standards of the existing population, where is the benefit?