The Property Council and the Real Estate Institute of Australia (REIA) enlisted ACIL Allen Consulting to write a report that attempts to debunk so-called myths that Australia’s negative gearing laws are having a deleterious impact on housing affordability and the Budget, and do nothing to boost housing supply nor improve rental availability and affordability.

The report polishes all the usual arguments. Let’s examine the key ones.

First, the report argues that middle income Australians, rather than high income earners, benefit most from negative gearing:

Advertisement

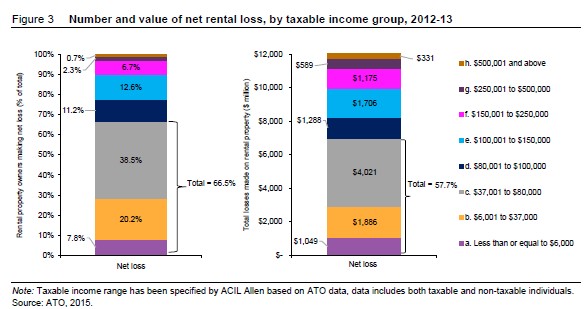

…negative gearing benefits a range of Australian households by providing all individuals with an opportunity to invest in property, not just those in higher income brackets. Two thirds of property investors who benefit from negative gearing earn a taxable income of less than $80,001 a year. Furthermore, while individuals with incomes higher than $80,001 claim around 42 per cent of the total value of losses on investment property, those earning less than $80,001 a year claim the majority (58 per cent of total value of losses in 2012-13). The data also shows that the majority of investors own only one property and this has not significantly changed over time.

ATO Taxation Statistics show that in 2012-13 there were 1.97 million individuals who owned a rental property, of which around 1.26 million declared a net rental loss.2 Around 67 per cent of those that declare a net rental loss have a taxable income of $80,001 or less.

The report’s claim is categorically false. Negative gearing is used predominantly by higher income earners.

Taxable income is what is left after legitimate deductions such as negative gearing are accounted for. For example, if someone earning $89,000 a year in 2012-13 claimed the average negative gearing loss of $9,558 that year, then their taxable income would be reduced to $79,442, thus making them appear to be a lower income earner than they actually were, and bringing them within the report’s arbitrary $80,000 threshold.

Advertisement

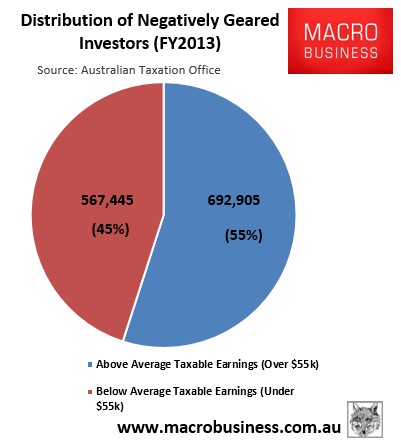

Moreover, the average taxable income in 2012-13 was only $55,228. Therefore, the paper’s $80,000 threshold for a middle income earner is blatantly mis-leading, since it it nearly 50% above the average taxable income level.

If it was true that middle income earners were the primary users of negative gearing, then we would expect to see the majority of users earn less than the average.

However, the ATO statistics clearly show that 55% of negatively geared investors in 2012-13 earned above the average taxable income level (see next chart).

Advertisement

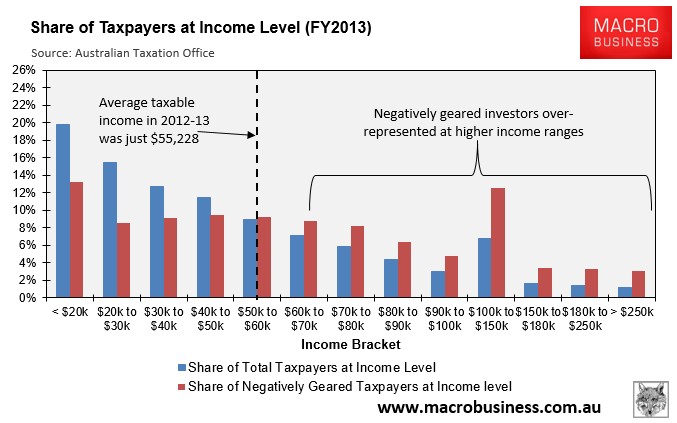

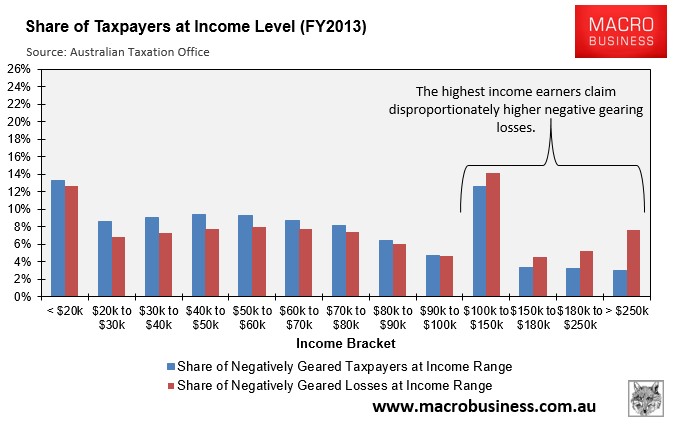

The ATO statistics for 2012-13 also shows that the number of negatively geared taxpayers was significantly under-represented at the lower taxable income levels and over-represented at the higher taxable income levels (see next chart).

Advertisement

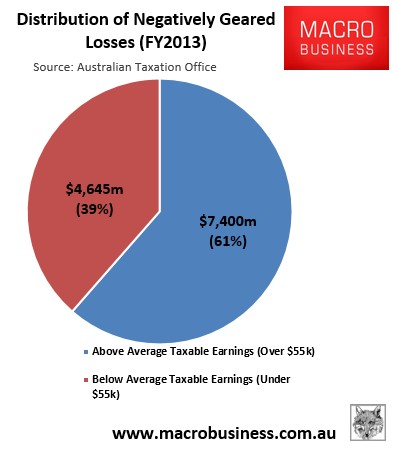

The picture gets much worse when the dollar value of losses, rather than the number of users, is examined. As shown in the next chart, those with taxable earnings below the average of $55,228 claimed only $4,645 million, or 39% of the total negative gearing losses in 2012-13, with those earning above average claiming $7,400 million, or 61% of total negative gearing losses:

Moreover, the breakdown by income range shows that higher taxable income earners claimed an even higher share of the negative gearing losses in 2012-13 (see next chart).

Advertisement

Therefore, based on the ATO statistics, which understate the magnitude of the issue because negative gearing lowers taxable income, the claim that most people who access negative gearing are middle-income Australians is false. 55% reported earnings above the average taxable income in 2012-13, with their share of losses at 61%, even after their reportable incomes were reduced by more than the average due to negative gearing deductions.

The use of negative gearing also increases with income, and the value of losses claimed even more so.

Advertisement

Next, the report tries to argue that capital gains tax (CGT) concessions also mostly benefit so-called middle income earners:

The 50 per cent discount on capital gains was introduced to eliminate the taxation of nominal gains (see Section 2.3). Eliminating the taxation of nominal gains seeks to provide individual taxpayers with the incentive to invest in order to earn a capital gain and bolster savings and economic growth.

The ATO data for 2012-13 shows that individuals across all income ranges benefit from the CGT discount, with 57.1 per cent of the approximate 389,000 individuals who paid CGT earning a taxable income of less than $80,001.

First, the report’s claim that the 50% discount on CGT “was introduced to eliminate the taxation of nominal gains” is wrong. Prior to the introduction of the 50% discount in 1999, only ‘real’ profits on asset sales were taxed, since they were indexed by changes in the CPI. However, the 50% discount on nominal CGT gains for assets held for more than one year did made the regime far more generous for property investors given Australia’s low inflationary environment.

Advertisement

As for the report’s claim that most CGT concessions are utilised by middle income earners (again, wrongly denoted by those with taxable incomes below $80,000), I have not taken the time to crunch the figures. However, I will leave it to the Australian Treasury to explain why the argument is categorically wrong [my emphasis]:

…the total effective concessions on capital gains income are significant. Both the indexation and discount methods have provided a strong incentive towards financial investment in products which provide significant capital growth, such as shares or property, rather than in products which primarily provide income streams, such as bonds. The concessionary treatment of capital gains income is arguably the primary motivation for financial investment in negatively geared real estate, which aims to shift all of the investment return into the capital gain on the eventual sale of the asset…

Taxable net capital gains income tends to be received by individuals at the higher end of the income distribution. Around half of total taxable net capital gains income reported for 2011-12 was received by taxpayers whose other taxable income was above $180,000 (the top tax rate threshold). For the 2011-12 year the average statutory rate of tax on taxable net capital gains income was 30.9 per cent, compared to the overall average rate of around 22.2 per cent.

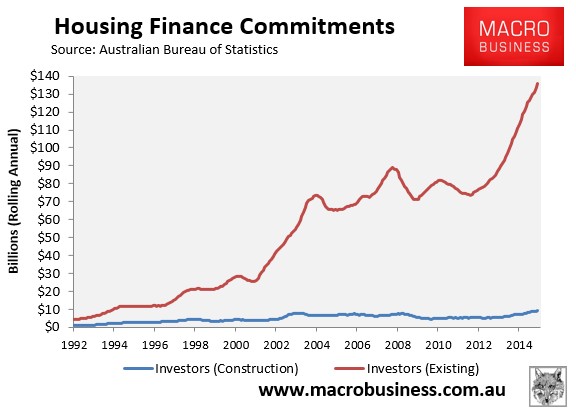

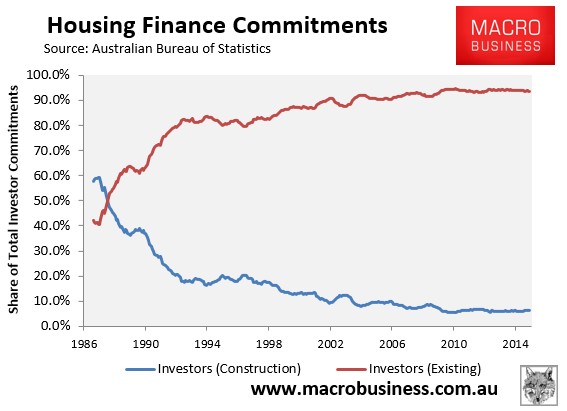

Next, the report tries to counter my claim showing that negative gearing does little to boost actual housing supply, since over 90% of investors purchase existing homes rather than new construction (see below charts).

Advertisement

Hence, my argument is that negative gearing is merely substituting homes for sale into homes for let. Thus, if negative gearing was abolished, it would not harm overall rental availability and affordability since investment properties sold by investors would be purchased by renters (or other investors). In turn, these renters would become owner-occupiers, thereby reducing the demand for rental properties, and leaving the rental supply-demand balance (and rents) unchanged.

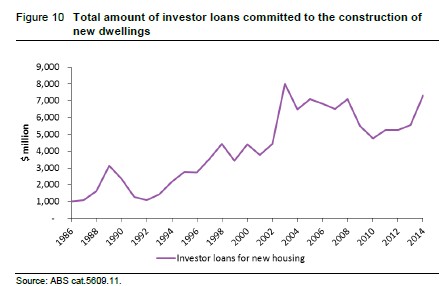

To counter this claim, the report resorts to the ultimate in statistical trickery by trying to assert that negative gearing has driven a more than seven-fold increase in investment in new construction:

Advertisement

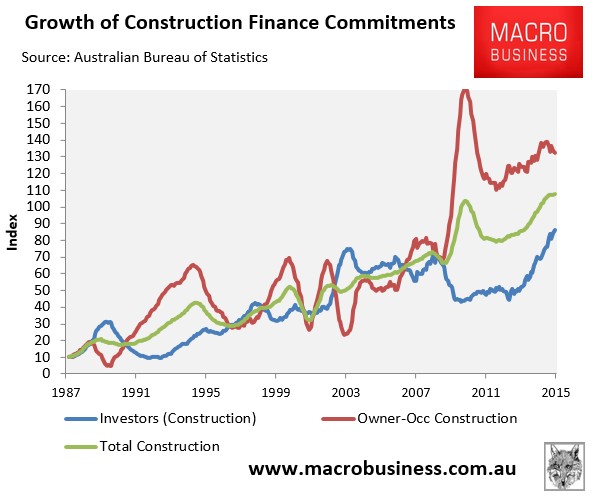

While the proportion of loans for investors towards the construction of new housing has remained relatively constant at around 30 per cent over the last 30 years or so, the absolute amount of investor loans committed to new housing has increased over time. In 1986, total investor loans for the construction of new housing were approximately $1 billion; this amount increased by more than seven-fold to $7.3 billion by 2014 (see Figure 10).

Many of these property investors would have made the decision to invest in rental property (regardless of new or established) reflecting many factors including the ability to deduct net rental losses made on their investment. Had negative gearing not been available, it is almost certain that total investment in property, regardless of whether new or established, would have been lower. Investment loans for new housing grew at a significant rate after the reintroduction of negative gearing concessions in late 1987.

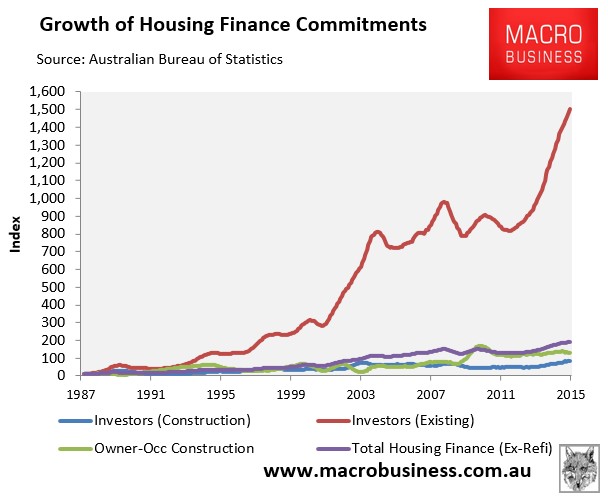

A more than seven-fold increase in the nominal dollar value of housing construction by investors sounds impressive until it is compared against the other forms of housing finance (see next chart).

Advertisement

That’s right. Since negative gearing was reinstated in 1987, the value of loans to investors in new construction has been dwarfed by loans to investors in existing dwellings. Even worse, they have also lagged the overall value of housing finance commitments (ex-refinancings), as well as owner-occupied investment in new construction (see next chart).

Given the above facts, it is highly misleading to claim that negative gearing has encouraged new construction when every other form of finance has grown even stronger since negative gearing was reinstated in 1987.

Advertisement

And given this false claim, the report’s conclusion that rents would lift by up to $10,000 if negative gearing was abolished makes absolutely no sense, given it does not support housing supply.

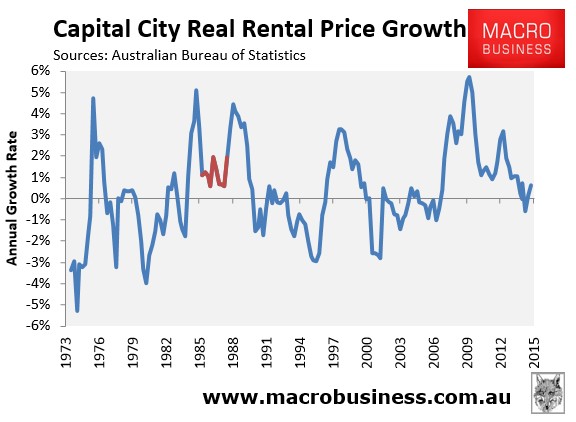

The claim is also not supported by historical experience. When negative gearing was temporarily quarantined between 1985 and 1987, there was no discernible impact on rents, with rental growth nationally higher both before and after negative gearing’s removal (shown in red):

Advertisement

To make matters worse, the report then contradictorily tries to argue that restricting negative gearing to newly constructed dwellings, as flagged by the ALP, would actually make the supply situation even worse and force-up rents:

… limiting negative gearing and the 50 per cent CGT to new dwellings would be a negative shock to the market which would likely result in upward pressure in prices. It is also possible that property investment would be skewed to outer suburbs where employment opportunities are scarce and where transport infrastructure is poor…It is likely that there would not be sufficient new dwellings to soak up a shift in investor demand towards new dwellings, which indicates that the measure would encourage many investors to exit the rental property market…

In addition, the policy measure would pit a large number of investors against aspirant owner occupiers in the relatively small new dwelling market…

Given these factors, the proposed tax change is likely to impose upwards pressure on the prices for new dwellings…

It is notable that there would likely be significant community unhappiness if there was a widespread and enduring displacement of the opportunity for first home buyers to actually own a new dwelling as a result of the proposed policy reform…

In summary, removing negative gearing and the 50 per cent discount on CGT for investment in existing residential property would probably increase investor demand for new dwellings, displace owner occupier buyers and stall further investment in established dwellings. If new housing supply is weak, higher rents and higher new dwelling prices would be expected…

Limiting negative gearing and the 50 per cent discount on CGT to new dwellings would be bad policy. It risks stalling investment in existing property and higher rents.

Seriously, you cannot make this stuff up. After wrongly arguing that negative gearing has boosted new construction and pushed down rents, the report then tries to argue against targeting negative gearing at new construction because it would stall overall housing supply and push-up rents and prices, whilst also locking-out first home buyers (as if the existing laws are not doing this already!). Talk about one almighty contradiction.

Advertisement

The report then tries to debunk the claim that negative gearing and the CGT discount encourages unproductive investment into housing, arguing instead that housing is just as productive as anything else:

…housing is about much more than just bricks and mortar. It satisfies the essential human need for shelter, security and privacy…

Housing is also a significant part of the national economy and an important source of employment…

…housing is the major source of wealth for Australian households. Housing serves two important functions for households: it acts as a savings and wealth-building vehicle for owner occupiers and investors, and it produces a flow of housing services that households consume.

The value of housing services can be directly quantified by rental yields for investor properties and imputed rent for owner-occupied dwellings. If the value of property assets did not appreciate over time to produce a cash return, then it would be correct to label them ‘unproductive’. However, the reality is that many residential assets do earn a real rate of return in the long-run…

Housing is a productive asset. It serves the valuable purpose of providing shelter to people, acts as a savings and wealth building vehicle for owner occupiers and investors, and produces a flow of housing services that households consume.

The report has clearly confused the positive return to home owners from economic rents with genuine productive investment that improves the competitive position of the economy and improves overall living standards.

Advertisement

Additions to the housing stock are productive in that they provide additional shelter to the community. But when capital flows predominantly into existing housing, as has been the case with negative gearing, then it is unproductive investment.

Here’s a question for ACIL Allen Consulting: If Australian housing values were to double due to a sudden flood of capital into housing, would this make Australia more productive? Similarly, if Australian house prices were instead half their current value (and household debt was materially lower), would Australia be less productive? Of course not.

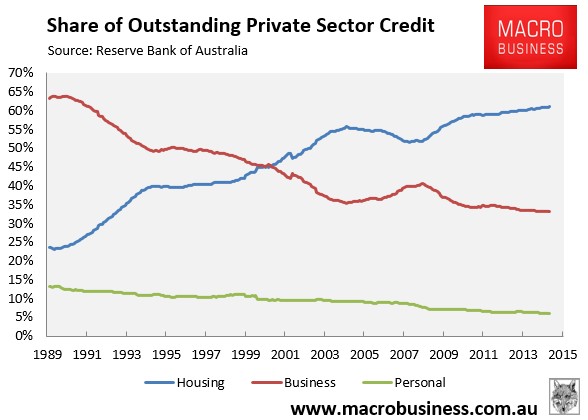

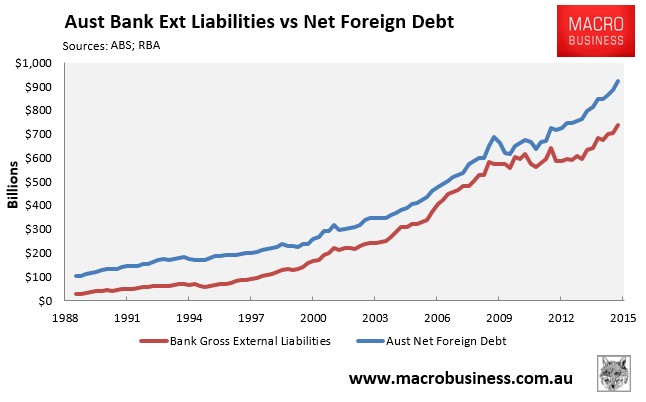

In fact, one could credibly argue that the diversion of bank loans and capital into housing (see next chart) has starved businesses of funds, damaging the nation’s productivity.

Advertisement

The banks’ heavy offshore borrowings, which have been used to pump housing, have also dramatically increased Australia’s net foreign debt, which is also a drain on the nation’s resources.

Advertisement

The same could be said about the escalation of land costs across Australia, which has unambiguously lowered productivity, due to the deleterious housing policies (including negative gearing and CGT discount) run by Australia’s various levels of government.

Finally, the claim that negative gearing and the CGT discount “acts as a savings and wealth-building vehicle for owner occupiers and investors” is not credible when an economy-wide view is taken.

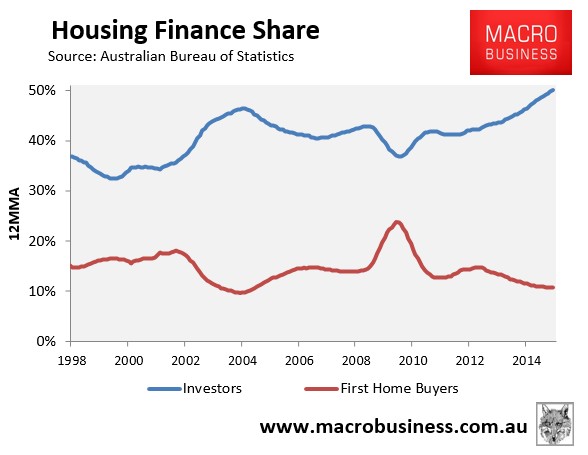

Blind Freddy can see that all negative gearing and the CGT discount are doing is using taxpayer subsidies to push-up house prices (see next chart) and turn would-be home owners into renters – hardly a desirable outcome from a budgetary or social perspective.

Advertisement

Clearly, ACIL Allen Consulting also does not care about the financial security of young Australians who are being locked-out of the housing market due to the orgy of investor participation (see next chart), or are being forced to undergo a lifetime of debt servitude.

Advertisement

If negative gearing and the CGT discount were unwound, there would be less pressure on house prices and younger Australians would not need to devote as much of their lifetime’s earnings to pay-off a home.

Surely, the financial situation of ordinary Australians would be improved materially if they were not required to pay-off some of the world’s biggest mortgages, due in part to egregious policies like negative gearing and the CGT discount?

Overall, the ACIL Allen Consulting report fails on every level to make the case for retaining negative gearing and the CGT discount.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.