Labor’s indefensible stance on the Aged Pension has been reaffirmed, with the party stepping-up its campaign against the Government’s and the Greens’ sensible deal to reverse the Howard Government’s 2006 reforms that greatly loosened the assets test to qualify for the part Pension.

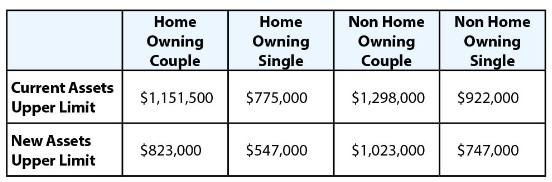

In 2006, then Treasurer Peter Costello announced that the taper rate by which the Aged Pension is phased-out would be halved from $3 per $1,000 of assets over the threshold to $1.50. This change greatly relaxed the assets test for the Pension, and led to the ridiculous situation whereby retiree home owning couples with $1.15 million in other assets, and home owning singles with $775,000 of other assets, could still qualify for the part Aged Pension along with the Pensioner Concession Card.

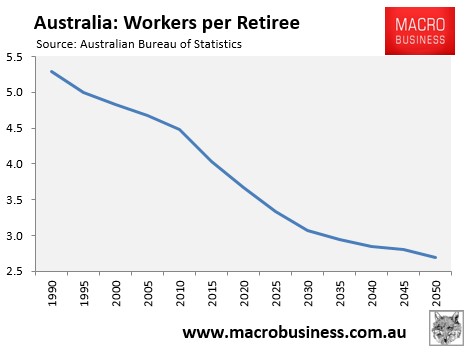

In effect, a large number of wealthy retirees were suddenly permitted to qualify for welfare – an unsustainable and inequitable situation given the rapid ageing of the population and the projected diminishing number of workers available to support them (see next chart).

Under the Government’s sensible reforms, backed by the Greens, Peter Costello’s changes to the taper rate will be reversed. However, while some wealthy retirees with significant financial assets will no longer continue receiving the part Aged Pension (but will keep their concession card):

The Government will provide additional funding to pensioners with fewer assets:

The Government’s and the Greens’ deal is expected to save the Budget (and younger Australians footing the bill) some $2.4 billion over four years, whilst improving the lot of pensioners without significant assets. It is a policy no-brainer.

And yet, the Labor Party still believes the reforms are unfair, and are now running the below campaign poster:

Moreover, Labor shadow ministers, Tanya Plibersek and Jenny Macklin, penned the following in response to deal between the Government and the Greens, attempting to show why the reforms are so unfair:

A lot of women today are part of the “sandwich generation”. They’re looking after kids or grandkids, but they’re also helping out their parents…

Younger people see the stress that their parents face and think it’s unfair…

Part-pensioners are people who have worked hard all their lives and managed to save money for their retirement so they don’t get the full pension…

These are people who have done exactly what they’ve been asked to do: save for retirement. Now the government says they should spend their savings before they can get a decent pension.

The changes the government is suggesting mean some single pensioners will lose more than $8,000 a year – a quarter of their yearly income of $36,000.

Some couples will lose approximately $14,000 a year…

But think of the part-pensioners you know. Many of them have saved hard and denied themselves luxuries all their lives. Many came to Australia decades ago with nothing, or left school early and worked 6 or 7 days a week. By definition, these people are income poor. They’re not living on easy street.

Play the violin, Tanya and Jenny. The thing you need to explain is why you think it is appropriate that home owning singles and couples with up to $775,000 and $1,151,500 in financial assets respectively should continue to receive welfare? The Aged Pension is a safety net, not an entitlement – something you both seem to have forgotten.

As for your concerns about the so-called “sandwich generation” – generation X. Surely their lot would be improved if they were not required to pay increasing amounts of tax to support older people with significant means that are well capable of supporting themselves?

What you both fail to acknowledge is that a retiree couple that has $850,000 in financial assets (in addition to their homes), and thus fails to qualify for the part pension under the new reforms, has more than enough means to receive an adequate standard of living in retirement without the help of fellow taxpayers.

Even if their investments merely kept pace with inflation, they could withdraw $40,000 a year for 21 years in today’s value before their funds would run out. This is a significant amount of money given they have no mortgage to pay, no tax to pay, and no dependents to support.

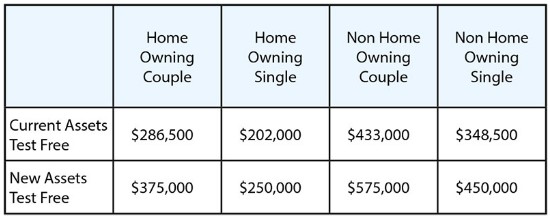

Add in the fact that they would soon start receiving the part pension, which would turn into the full pension once their funds fall below $375,000 (in today’s value), and their lot improves even more.

Let’s also not forget that the couple can also take advantage of the Government’s Pension Loans Scheme – a state-run reverse mortgage scheme that allows eligible retirees to borrow against their homes to receive payments from the government equivalent to the full Aged Pension.

The interest rate through the Pension Loans Scheme is only around 5%, repayable upon their estate or sale, so it is highly affordable.

With the Aged Pension costing the Budget some $40 billion this financial year, growing by 7% annually, and the ratio of workers supporting the elderly shrinking (see above chart), the system as it stands is utterly unsustainable and inequitable from an inter-generational perspective.

One would have thought that a party that purports to represent the ‘battler’ would enthusiastically support the Government’s pension reforms, rather than expecting younger Australians, many of whom will never be fortunate enough to own their own homes, to continue subsidising oldies with significant assets.