Europe is toying with the end of the global business cycle. We don’t know whether the Grexit, which now appears more likely than not, will result in GFC 2.0 but it is certainly possible. Much Greek debt has been passed from the private to the public sector over the past four years but you just never know in contemporary financial markets. That’s the problem, risk is so dispersed and capital so slim, that any credit event of magnitude threatens another daisy chain of defaults that puts everyone under suspicion.

If Greece defaults, and if I were them it I’d make it a doozy, then Europe is going to enter some kind of banking intermarket freeze, peripheral bond yields are going to spike, core rates collapse, and global borrowing costs for anyone externally funded shift structurally higher. Following on, global stock markets are going to take it in the neck.

We have various QE’s in play to help contain the fallout and markets could get through this without a repeat of the GFC if the European banks have prepared appropriately. As Delusional Economics writes today, this may, in the end, instead be a longer term issue of a fatal blow to the European Central Bank. After all, if it can be defaulted upon what’s the point of the entire contemporary monetary system on the Continent? So, I’m not sure exactly how much ECBQE will be worth at this point. Quite a lot still, one would think, as its death will be chronic not acute.

Nonetheless, it the Grexit transpires we are surely going to see a flight of capital to the most trusted institutions and stores of value. That means US Treasuries, the US dollar and the Japanese Yen. This will be reinforced by the Fed suddenly getting a lot more patient on tightening cutting its bond market a break. On balance I think we can expect the US dollar to rise anyway as falling equities, the threat of trade disruption and the flight to quality drive it up.

Gold will be interesting to watch. If Armageddon fear has not yet taken a hold then it should fall. If it rises then all bets are off.

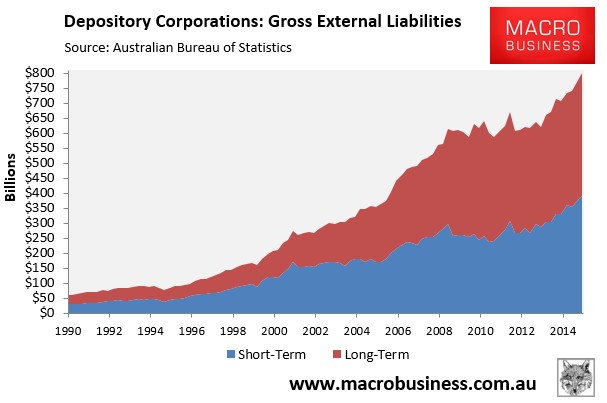

For Australia the next great test of our own half-broken financial system and economic model will be upon us. The current east coast housing boom is inescapably externally funded:

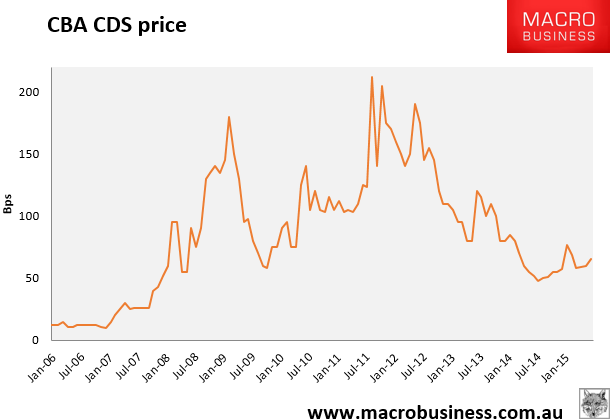

Bank wholesale funding costs will jump. As of Friday, CBA CDS (a proxy for bond yields) was trading at 65.5 basis points over swap but that’s going to rise, a lot if the Grexit goes badly:

At somewhere around 120bps, borrowing becomes uneconomic and the banks enter liquidity stress. Non-bank lenders cut out even lower. More rate cuts, earlier, are inevitable. The bond market is going to rally hard (for a while anyway) and the Australian dollar is going to fall, a lot if the Grexit is disorderly.

These outcomes may be complicated or delayed this week by the Chinese easing but they are fighting a losing battle with growth. If Europe does get bad then China will stimulate further but not before its trade takes a big hit. I can’t see the Shanghai bubble surviving a global shakeout, either, though you never know in the short term. On balance, Chinese easing does not stack up as protection against a Grexit. Commodity prices will take another sharp leg lower.

Rising bank funding costs also bring into play the Budget and the AAA rating. On that front, the Weekend Australian had an important interview with Standard and Poors:

Risks to Australia’s AAA credit rating are diminishing with ratings agency Standard & Poor’s reassured by the passage of budget savings measures and confident that domestic banks could withstand any downturn in the housing market.

However, the pressure for more austerity remains:

“We’re still looking to government to find savings elsewhere…New spending on disability and other commitments on the horizon, to get the budget back into sustainable balance if not surplus does mean they need to reduce structural growth in other areas.”

It also reiterated the usual warning:

…Although Australia has a much lower government debt than other AAA-rated countries, Mr Michaels said it had greater vulnerability because of its persistent current account deficit which makes it dependent upon external financing.

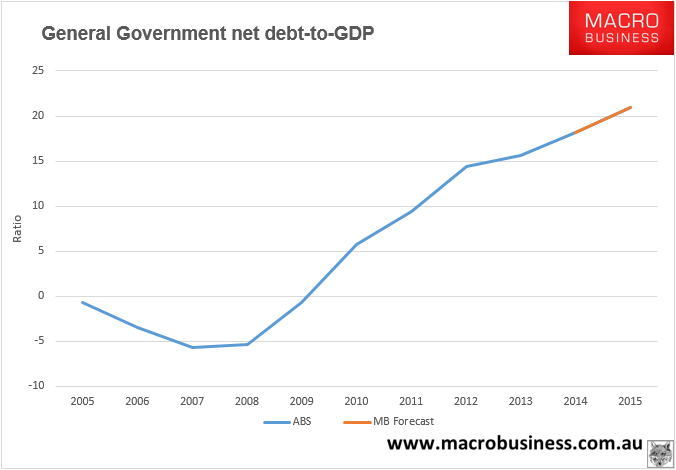

The good news is that with the recent thawing in the senate the Budget outlook has improved a little. Here is the up to date MB chart of net general government debt to GDP:

Recall that 30% is S&P’s threshold for retention of the AAA rating. MB estimates that we’re currently sitting around 21%. Safe for now but not if the European crisis triggers an end-of-cycle event. Our stimulus options are much more limited than 2007, with perhaps half the capacity after the event and the need to tighten much earlier afterwards.

In summation, the Australian economy is in no state to take on another global shock. We are only halfway through the terms of trade adjustment triggered by China’s slowing with huge falls still ahead in capital spending. The major offset for domestic activity uniquely hinges upon the confidence of consumers and a rampant housing bubble in the east that is implicitly externally funded and reliant upon low international interest rates for private markets. Even a moderate shock, one that pushes the ASX down to say 4500 points, triggering household and speculator caution, and a period of higher bank funding costs, will expose the underlying weakness in the economy and unemployment will rise sharply. We will be in a proper recession in the blink of an eye.

So, what are the scenarios?

1. A clean Greek exit

- European banks have prepared appropriately and the shock lasts six weeks. Global share markets correct 10%, peripheral bond yield jump higher but QE holds them together;

- the Australian dollar falls into the high 60s, bank funding costs rise but do not lock-up, the economy stutters but rate cuts prevent housing from toppling over. Bank funding costs crimp profits but the banks hold back some of the rate cuts to boost margins;

- the economy stumbles on at stall speed as unemployment creeps higher, increasingly vulnerable as we wait for the next shock.

2. A moderate Greek exit

- Some European financial entities have punted long on Greek bonds and are suddenly insolvent. Global share markets fall 20% as the European financial system part freezes and QE only holds back outright panic;

- the Australian dollar tanks to 55 cents as bank funding costs rocket, the economy stalls and emergency rate cuts to 1% can only soften the housing correction. The government loosens the purse strings as a recession ensues;

- the economy enters a zombie state in and out recession for the next 3-5 years as unemployment grinds inexorably higher, housing steadily deflates despite every fiscal effort to keep it up. The RBA supports banks via its limitless liquidity mechanism but they remain capital constrained as they chew through rising bad debts and lending standards tighten permanently;

- the economy is supported by net exports and a low Australian dollar which slowly rebuild tradables. Again, all this will accelerate dramatically when another shock arrives.

3. A Graccident

- losses are sufficient to push the European financial system into crisis and it spreads worldwide. Global share markets plunge 50% and all peripheral global bond yields shunt higher. ECBQE is rendered moot;

- the Australian dollar crashes to 45 cents, bank funding costs leap and the Australian Government guarantee is forced to become explicit once more;

- house prices crash, interest rates fall straight to 0.5% and the Government unleashes a $30 billion stimulus;

- the sovereign rating is stripped within a year and funding costs refuse to come down. House prices keep falling and don’t stop until down 30-40%. Unemployment crosses 10% and keeps rising and Australia enters its worst recession since the Great Depression. WA enters an actual depression. The Budget is forced to bail out the big four banks by nationalising the LMIs and public debt rockets to 50-60% of GDP within three years.

- the Australian economy resets via a much lower real exchange rate.

Any way you look at it a portfolio prepared for a Grexit will:

- be short the Australian dollar;

- limit or erase exposure to housing, banks and the consumer and,

- exit equities and go long cash.

In short, the answer to the question is Australia ready for GFC 2.0 is a resounding “no”.