More Efficient Ways for the System to Solve for Growth

Westpac believes that a more sustainable way of ensuring the system can best support growth in periods of higher credit demand is to increase the source of high quality bank funding to support lending. Banks with more, higher quality deposits will have more funds available for intermediation (and, in turn, to support economic growth). In Westpac’s view, the primary long-term solutions for increasing the sources of higher quality funding are:

equalising the tax treatment between bank deposits and debt instruments with other competing savings options; and

encouraging the investment of superannuation funds in bank deposits and fixed income securities. An increase in the source of high quality funding to the banking system means that Australian Banks have the capacity to lend to small and medium enterprises, at a reasonable cost, to foster increases in productivity, innovation, employment and wages.

Tax Equalisation of Bank Deposits and Debt Instruments Taxation plays a significant role in savings decisions. The Henry Review noted: ‘There is considerable evidence that tax differences have large effects on which assets household’s savings are invested in. Based on an examination of the literature and OECD data, the OECD concluded that while low-income individuals respond to tax incentives with more savings, for high-income individuals in particular savings are diverted from taxable to tax-preferred savings (OECD 2007)’.

In summary, encouraging investments in bank deposits and other debt instruments:

will likely reduce Australia’s reliance on offshore wholesale funding – which is more volatile and unreliable, particularly in times of stress;

will provide a higher quality more sustainable funding base – which is also acknowledged by the regulators9 ; and

should encourage higher levels of national savings to support economic growth. We believe that providing an appropriate level of harmonisation of tax relief for bank deposits and debt instruments with other forms of savings will at least lead to a greater allocation of savings in bank deposits.

For example, it may encourage investors to redirect some excess superannuation contributions to this form of savings and will also provide a more stable source of retirement income.

Response Question 19 To what extent is the rationale for the CGT discount, and the size of the discount, still appropriate?

Westpac’s view

The current CGT discount was introduced in 1999 and allows individuals to discount a realised capital gain by 50 per cent provided they have held the asset for 12 months. Superannuation funds are also able to claim a discount of 33.3 per cent. Prior to the introduction of the CGT discount, indexation and averaging applied to capital gains meaning that only real gains were subject to tax.

We note the concern that the current 50% discount after only 1 year is not appropriate as it does not strike the right balance between removing the impacts of inflation, while discouraging speculative ‘asset flipping’ behaviour. We believe it is appropriate that the tax arrangements for long term savings neutralise the effects of inflation on asset prices, so that only real increases in income are taxed.

However, we recommend considering an adjustment to the current arrangements for capital gains to align the tax treatment with other savings options.

This would support the goal that investment decisions are not taken on the basis of after tax outcomes and would improve overall equity between investors at differential marginal tax rates. It may also moderate the concentration of debt-funded risk-taking in property investment.

We note that if the Henry recommendation for harmonisation (or some variation thereof) was adopted there would be a reduction in the present CGT discount rate. If that was to occur, we would advocate that existing assets be grandfathered. Whilst this would add some complexity, it is appropriate on the basis of treating taxpayers fairly. APRA has introduced a new Liquidity Coverage Ratio (LCR), which require banks to hold increased levels of liquids assets to meet a 30 day liquidity stress scenario. Under these rules, there is a clear distinction between different types of deposits, and how much a bank can lend from them. The best type is retail, which will allow a bank to use 95% of the value for lending to customers. The least valuable is short term from other financial institutions, which will not allow any lending.

Response Question 21: Do the CGT and negative gearing influence savings and investment decisions, and if so, how?

Westpac’s view

We note that the Tax Discussion Paper focuses on the impact of negative gearing on housing investment. However, negative gearing is not unique to the property market as investors in shares and most businesses in Australia are also able to access negative gearing.

We agree with the observations in the Tax Discussion Paper that negative gearing, in itself, does not cause a tax distortion. However, it is important to note that negative gearing does have an impact as leverage allows more people to enter the (housing) market. Although the tax treatment of rent, property expenses and capital gains are important considerations, there are other, potentially more significant drivers behind people’s decisions to invest in the property market. The major one being capital growth.

In our experience, investors exhibit certain rational behaviours meaning they take account of a range of factors, both tax and non-tax related. To illustrate, our experience shows that investors prefer a lower Loan to Valuation Ratio (LVR) at origination than owner-occupiers10 , and are sensitive to upfront costs such as lenders mortgage insurance. Gearing is therefore kept at reasonable levels notwithstanding the potential for a larger negative gearing benefit. Investors typically avail themselves of deposit offset accounts and investor repayment behaviour is comparatively strong thus reducing the investor’s negative gearing benefit.

In summary, investors are generally not geared to the maximum extent possible for the purpose of maximising their tax benefit.

Although it is difficult to accurately identify the proportion of investors that are negatively vs positively geared, we estimate average LVR levels to be in the range of 45%-55% and this indicates to us that the a significant number of investors’ property assets are moving away from being negatively geared.

Property is also seen as an attractive investment in Australia . Another potential factor underpinning investor activity is the impact on values (and therefore capital growth) created through scarcity. Significant demand for housing stock is being driven by national population growth (see graph below) consistently exceeding new dwelling approvals, particularly over the last decade.

We are not aware of any authoritative literature validating the effect of any proposed change to limit or abolish negative gearing and, to that end, further modelling and analysis is required. We note that the Senate Committee report on Housing Affordability recommended the Treasury carry out a study of the influence of negative gearing and the CGT discount on housing affordability and consequent impacts on the rental market. We agree that such a study would help to inform further consideration of this issue.

As we have noted elsewhere in our submission, retaining the CGT concession together with harmonised tax treatment across other forms of savings and investment options would ameliorate concerns as to the influence of tax concessions on investor decisions.

Westpac makes a number of pertinent observations here.

Australia’s peculiar tax laws have made investment into housing a relatively attractive proposition via a combination of high tax rates on savings in addition to generous tax concessions like negative gearing and capital gains tax discounts. As a result, demand for housing in Australia is much higher than it otherwise would be.

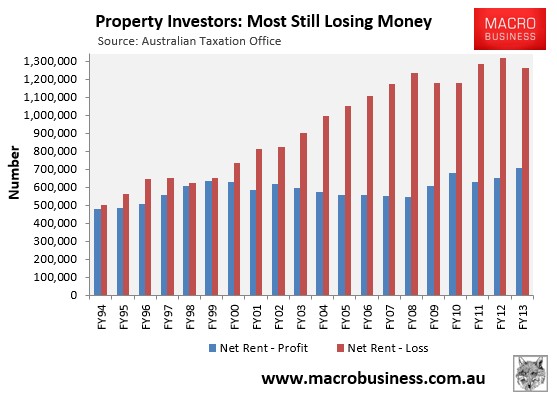

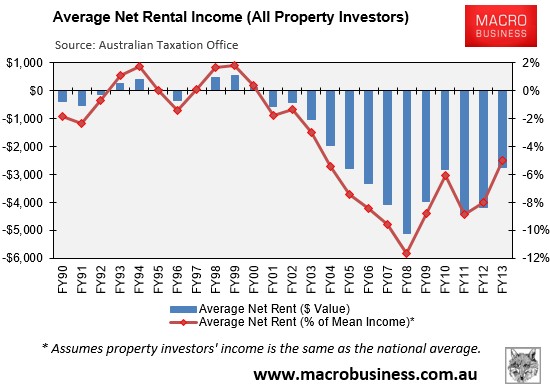

The combination of Peter Costello’s capital gains tax (CGT) cut with negative gearing was undoubtedly also a major trigger for the rise of the fifteen year property bubble, as evident by the below charts:

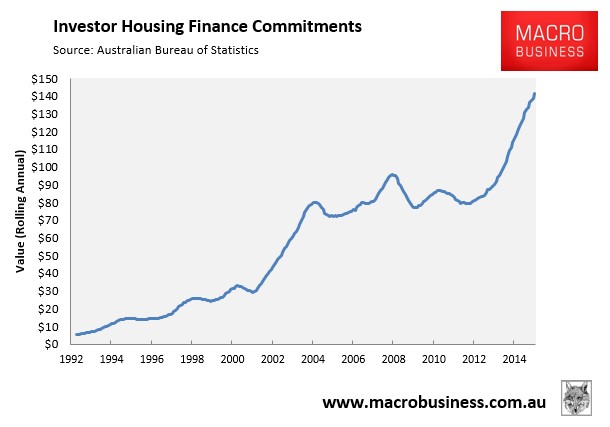

Prior to CGT being cut in 1999, aggregate net rental income was roughly zero and there was a similar number of property investors negatively and positively geared. Since then, negatively geared investment has exploded, as has the value of investor loans (see next chart).

Even Megabank wants out of the ponzi. Only politics stands in the way.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.

Although it is difficult to accurately identify the proportion of investors that are negatively vs positively geared, we estimate average LVR levels to be in the range of 45%-55% and this indicates to us that the a significant number of investors’ property assets are moving away from being negatively geared.