by Chris Becker

Its hard to predict, especially the future, but there’s a combination of factors out there, embiggened by the RBA’s rate cut debacle yesterday, that suggest the top is in for bank stocks.

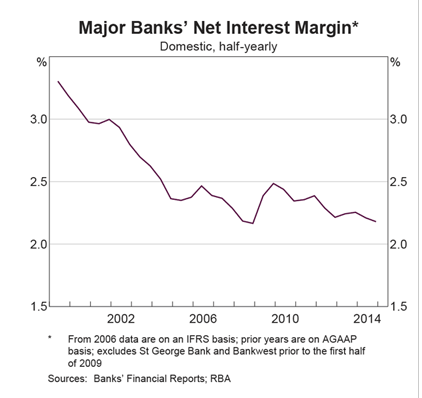

Let’s count them off. Three of the majors have reported flat profits this week as they struggle to combine record low interest rates into meaningful (read:profitable) mortgage growth, even as property prices continue to surge. The crux is funding and pressures on capital ratios, as net interest margins continue to be squeezed: