Chris Stott, chief investment officer of Wilson Asset Management, has entered the housing bubble debate, arguing that there is no bubble because of the chronic undersupply of homes that has not kept pace with the growing population. From The AFR:

…is Australia in a housing bubble?

We don’t believe this is this case. Australia has not built the homes needed for our growing population in recent decades. The fact that we’re still facing an undersupply of homes means it is unlikely we’re in a housing bubble…

Rising house prices are being driven by growing demand from years of positive net migration. While the country has been too slow to cater for its own population growth, we have also failed to accommodate those who have settled here from other parts of the world…

Against this backdrop, home ownership will become even more unattainable for the next generation. It is likely Australia will follow the European path and become a nation of renters…

As we struggle to provide housing supply it’s hard to agree we’re in a bubble. A fall away in the macroeconomic conditions, reduced migration or regulatory intervention could slow current price growth and present issues over the medium to longer term.

Regular readers know my view: Australian housing is a bubble because valuations are not supported by the underlying fundamentals.

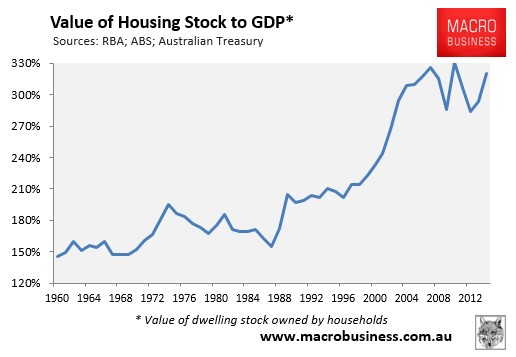

The total value of Australia’s residential dwelling stock owned by households was 3.2 times GDP as at December 2014. Further, it is rising fast and is only a smidgen off all-time highs (see next chart).

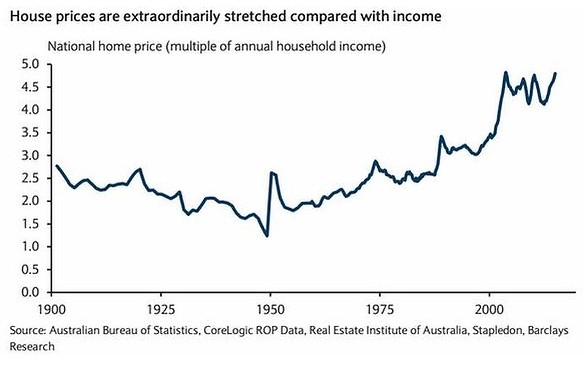

The same goes for valuations versus incomes, which are pushing all-time highs (chart from Barclays):

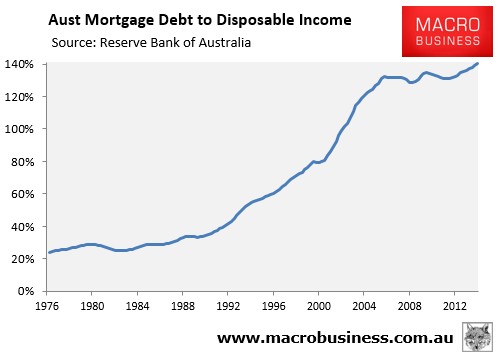

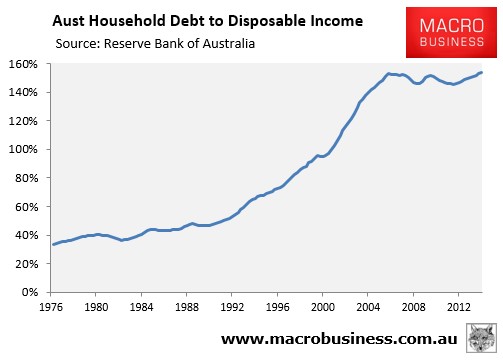

Then there is Australia’s household and mortgage debt, which also hit all-time highs in December 2014 (see below charts).

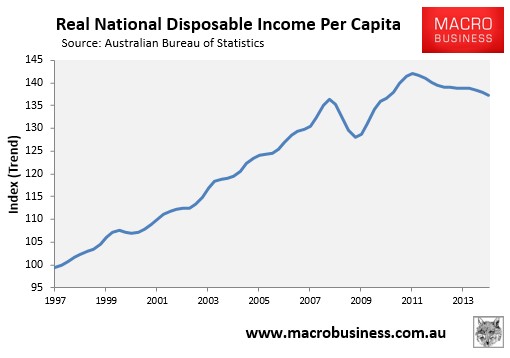

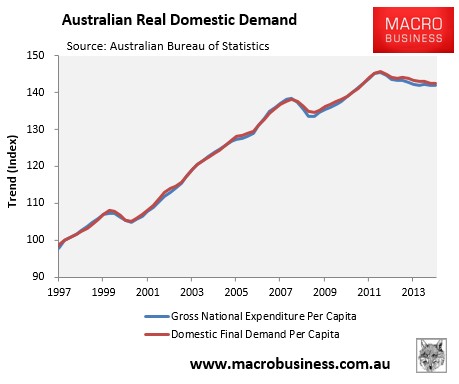

Sure, interest rates are at record lows, which are obviously supporting valuations. However, just as housing values and debt are pushing all-time highs, the mining boom is unwinding fast, causing real national disposable income and domestic demand to fall (see below charts).

Wages growth is also at record lows:

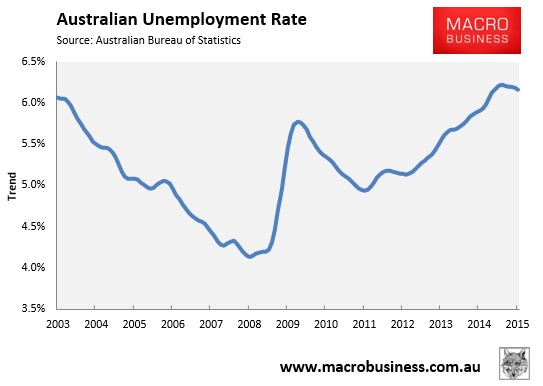

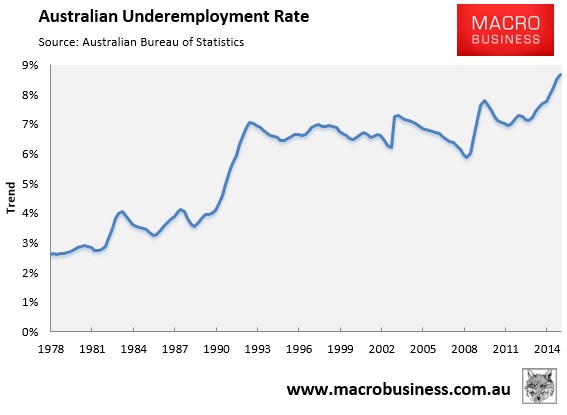

Unemployment and underemployment are also highly elevated (see next charts).

The outlook for the economy is also poor. The once-in-a-century mining investment boom will decline sharply over the next few years as large mining projects are completed. Then there is the ongoing income shock as the terms-of-trade retreats back to historical norms, not to mention the closure of the local car industry by 2017, which will further increase unemployment.

So we have an alarming situation where Australian housing, albeit led by Sydney and Melbourne, is already pushing all time high valuations and is speeding towards the (mining) cliff.

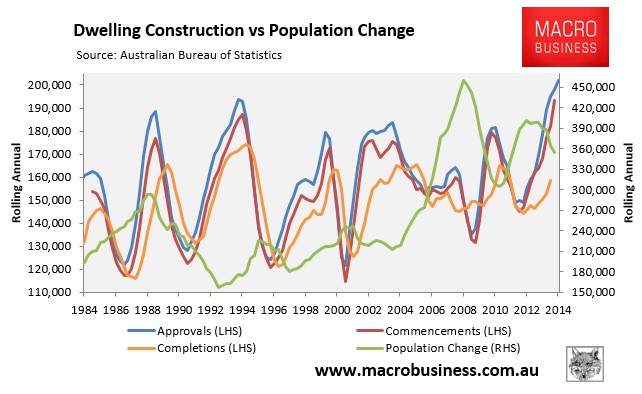

The undersupply argument is also weakening as dwelling construction lifts just as population growth falls (see next chart).

In any event, there is enough evidence from around the world that a perceived undersupply cannot hold-up prices indefinitely anyway.

General economic conditions can deteriorate, as seems likely to occur in Australia, causing unemployment to rise and the number of people per dwelling to increase as they group together to reduce their housing costs. Such actions can also turn a perceived housing shortage into a surplus.

The economic reality is that the demand for housing is highly changeable depending, largely, on the prevailing economic conditions. And when housing supply is unresponsive (‘inelastic’), these changes in demand feed directly into prices instead of new construction, making the housing market more volatile and prone to boom/bust cycles.

A classic example of this phenomenon is California, which had experienced lower rates of home construction than Australia, and was said to have a chronic housing shortage driven by continued high rates of household formation and inadequate construction.

Home prices still crashed there, as they did in Ireland, Las Vegas (see here and here) and many other places where land/housing shortages were said to exist.