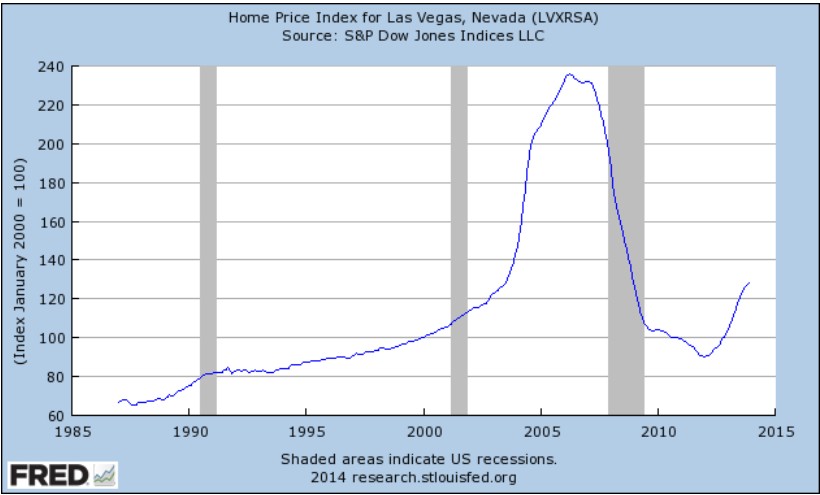

Las Vegas is home to one of the world’s largest housing bubbles/busts, whereby house prices rose sharply in the decade to 2007 before plunging more than 60% in the years following (see below chart).

In 2011, I wrote a detailed article, How Las Vegas gambled and lost, which placed the blame for Vegas’ housing bust on a unique combination of lax lending combined with rapid population growth and restricted land supply:

Advertisement

Certainly, if credit was less readily available, households would have been constrained in their ability to bid-up prices. But easy credit was only part of the problem. Another key driver of the rampant price escalation and then collapse was the way in which land was supplied for housing.

Throughout the 2000s, Las Vegas was the fastest growing metropolitan area in the United States with more than 1,000,000 population (see below chart).

However, despite there being ample developable land within 40 miles of the Las Vegas city centre to accommodate this population growth, the actual quantity of land available for development was heaviliy restricted by the federal government Bureau of Land Management (BLM), which owns around 90% of the land in Clark County, which contains the entire Las Vegas urban area. The BLM heavily restricted sales of land to the market in an effort to maximise revenues, causing builders and developers to bid-up land price in period auctions to ensure their supply of land for construction (called ‘land banking’).

Whereas the price of land for housing generally sold for $40,000 per acre in the late 1990s, toward the peak of the bubble, average land prices fetched ten times that amount. Obviously, this land price inflation was a principal cause of the house price escalation…

I also provided an except from USA Today in late 2006, which explained the supply situation in Las Vegas well:

LAS VEGAS — Flying into this desert metropolis is as deceiving as a mirage. From 10,000 feet you see empty land in all directions and swear the pace of suburban sprawl could go on unchecked.

You’d swear no end’s in sight to subdivisions stretching for miles beyond the Strip, enclaves of single-family houses that draw thousands of Californians and other migrants a year.

Look again. The valley that Las Vegas and 1.8 million residents call home is nearly built out. Mountains, national parks, military bases, an Indian community and a critter called the desert tortoise have Sin City hemmed in. At the current building pace in the USA’s fastest-growing major metro area, available acreage will be gone in less than a decade, developers and real estate analysts say.

Yet growth pressure and housing demand won’t abate. Greater Las Vegas will add 1 million residents in the next 10 years, state estimates say, and hit 3 million by 2020.

“You hear anywhere from a seven to 10 years supply at our growth rates and the valley’s full,” says developer Kenneth Smith of Glen, Smith and Glen…

A scarcity of land — or just as important, says Hal Rothman, a University of Nevada-Las Vegas history professor, the perception that it’s scarce — is driving prices skyward. “The result was a rush,” he says. “The situation is making a new valley around us, one that will be more crowded and expensive.”

Developers who 15 years ago paid less than $40,000 an acre are paying more than $300,000 today. In an auction of public land that went on the market last year, a developer paid $639 million for 2,655 acres…

Developers don’t expect land prices to fall. They’re packing houses in traditional subdivisions so close together neighbors can practically shake hands out their windows. Economics are moving developers toward a slow embrace of trends familiar elsewhere…

Advertisement

A recently released paper by Harvard economists provides further analysis on Las Vegas’ bubble/bust and shows how government interference in the land market, and perceptions of shortages amongst developers and buyers, caused Las Vegas land prices to bubble despite significant construction volumes – analysis that could just as easily be extended to Arizona, which faced similar land supply constraints.

Below are the key extracts.

We consider a city that faces a long-run growth barrier. Construction occurs as more and more people move to the city. Because of this growth, the city will eventually run out of space for development. The price of undeveloped land reflects investors’ beliefs about the future flows of people to the city.

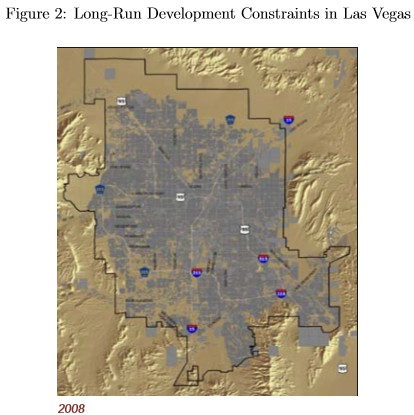

The long-run growth barrier comprises many factors—for example, geography, regulation, and transportation costs—that arrest development. For instance, Las Vegas faces a development boundary put in place by Congress in 1998. The Southern Nevada Public Land Management Act forbids the federal government from selling land to developers outside the boundary shown in Figure 2. During the 2000-2006 housing boom, many investors believed the city would soon run out of land. Land prices within this boundary rose from $150,000 per acre to $650,000 per acre from 2001 to 2006.

…speculation leads to a high construction house price boom when the city nears but has not yet reached the long-run development barrier. When a city nears this constraint, undeveloped land allows the city to accommodate the current shock through new construction. At the same time, investors take to the land market to speculate about the price of housing in the near future when the city will have run out of land. Because the price of housing reflects the current cost of land, speculation about future house prices drives up prices today…

Las Vegas during the 2000-2010 boom and bust provides a striking case of a high construction house price boom in an area approaching a development constraint. The ample raw land available in the short-run allowed Las Vegas to build more houses per capita than any other large city in the United States. At the same time, rampant speculation in the land markets caused land prices to quadruple between 2000 and 2006 and then lose those gains, leading to a boom and bust in the house prices. A single land development fund, Focus Property Group, outbid all other firms in every large parcel land auction between 2001 and 2005 conducted by the federal government in Las Vegas, obtaining a 5% stake in the undeveloped land within the barrier. Focus Property Group declared bankruptcy in 2009…

Around 2000, new technologies were developed that expand credit to low-income borrowers, raising housing demand throughout the country and in Las Vegas. Due to the regulations described in the Introduction and shown graphically in Figure 2, Las Vegas will run out of land in the next 20-30 years. Investors, anticipating this future development, scramble to get a hold of this remaining land, knowing that it will appreciate as the city continues to develop. These land investments are akin to buying property in an up-and-coming neighborhood before it gets popular…

Arguably, Las Vegas’ housing market bears some similarities to Melbourne’s.

Advertisement

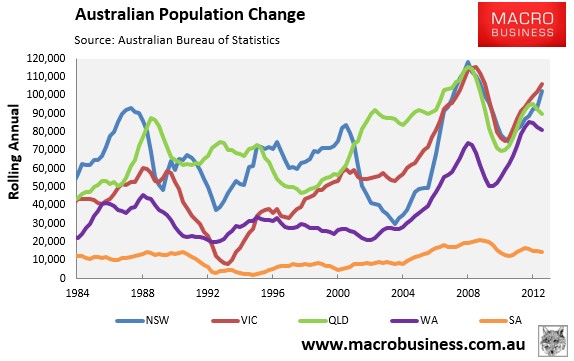

Like Vegas, Victoria (read Melbourne) has experienced the highest population growth in the nation (see next chart).

It also has an urban growth boundary in place, which has recently been set in stone by the State Government and could see developable land run-out within 30-years.

Advertisement

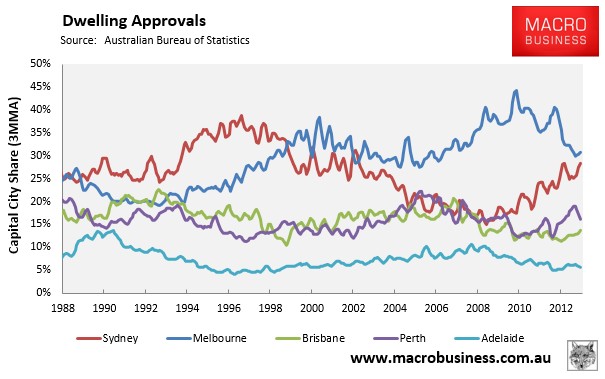

Finally, Melbourne has experienced the highest construction rates in the nation, accounting for 37% of all capital city dwelling approvals since the beginning of 2008, despite comprising only 28% of capital city households (see next chart).

Melbourne’s joint house price and construction boom, therefore, has shades of Las Vegas and Phoenix, arguably making it more exposed to a housing correction in the event that demand slumps.

Advertisement

As for policy lessons, the Harvard economists conclude with the following piece of wisdom:

From a policy angle, our paper shows that expectations of future constraints matter in a housing boom even more than short-run constraints…

We suspect that even if there are no short-run constraints, and even if most investors believe there will never be long-run constraints, a boom and bust can occur if some investors believe that future regulatory policy will limit city growth. City managers who wish to promote house price stability may want to be especially clear about future regulatory policy for this reason.

Advertisement

That’s another way of saying that urban containment barriers should not be enacted in the first place, since they can give the perception of shortages (or expectation of future shortages), leading to increased speculative behaviour.

It also helps to explain why markets free of regulatory constraints, such as Houston and Dallas Texas, never bubbled and busted, since speculative demand was never present.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.