From Twiggy Forrest via Junket Jen at the AFR:

“When has market share strategy over shareholder returns ever helped a company? What BHP and Rio are doing is buying – at massive cost – expansion capacity even when the higher commodity price justification for such investment has evaporated. It’s as though they are stuck in a time warp, unable to move with the changed circumstances. Over time, it will be seen for what it is – egos before commonsense.”

Fortescue’s total all-in costs are around $US43.50 a tonne, for example. The target is to get that down further to between $US35 to $US37 a tonne this year. And, FMG always prides itself on its ability to consistently exceed its targets.

“That will make Fortescue’s cash costs at least as competitive as BHP and Rio, so you have to ask what their strategy is –because it’s not about making adequate profits,” Forrest fumes.

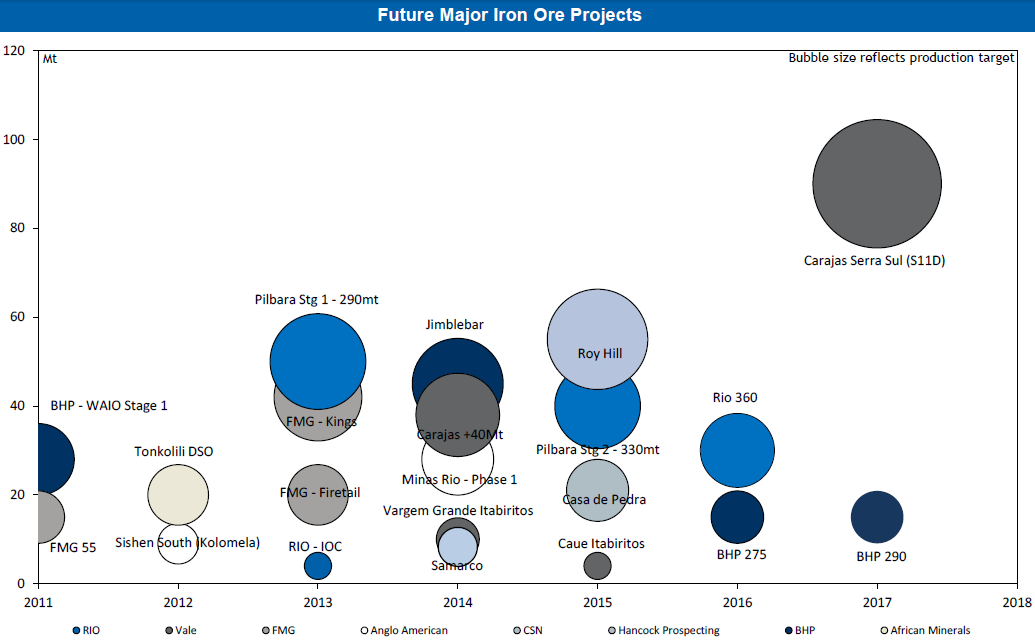

Alas, no it won’t. That’s not the grade-adjusted breakeven, which is more like mid $50s. And it’s not BHP and RIO doing it either. It’s BHP, RIO, FMG, Anglo, Sino, Roy Hill and Vale:

This is clearly part of a political economy blame game to cover what is coming next for FMG.