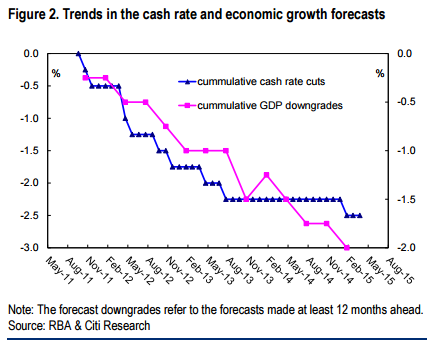

Will the RBA cut in May? Citi offers a great chart to show how in terms of the bank’s own “reaction function” that it should:

The chart shows how far behind the curve the bank is in its own terms. The next RBA opportunity to cut the growth outlook is in the May Statement on Monetary Policy (SoMP) three days after the next meeting. If it has any sense it will be cutting the growth outlook further. Consumer and business confidence is weakening, the terms of trade is literally collapsing, the capex outlook is terrible, the labour market is soft and likely to turn soggy in months ahead and the housing construction boomlet will peak in H2. The only positive (in the bank’s view) is strong house prices and they are confined to two cities.

Fiscal considerations are also poor with the Treasurer already declaring that the Budget will be mildly contractionary as well, though I expect they will try to backend load the austerity. The Budget is May 14 but the bank will certainly be informed in advance.