From the wise people at PIMCO:

After re-engaging policy support in February following an 18-month hiatus, the Reserve Bank of Australia (RBA) wrong-footed many in the market by keeping policy on hold in the two subsequent board meetings. So was February’s decision a “one-and-done” policy event or the start of a more aggressive easing cycle? We believe the truth lies somewhere in the middle: We view recent policy meetings as a temporary pause in a protracted easing cycle as Australia contends with its secular transition away from mining-led growth. Given this outlook and market pricing, we think the best expressions of this macro view are via a short position in the Australian dollar rather than aggressive duration positioning, and taking advantage of wider cross-currency spreads to add some global credit exposure to portfolios hedged back to the Australian dollar.

Policy re-engaged

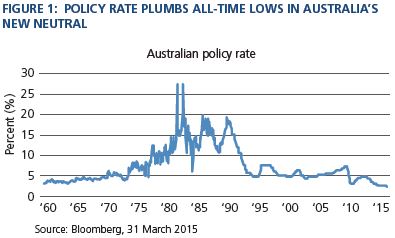

Following the flood of monetary policy easings around the world in early 2015, the RBA added its stimulus to the global punch bowl by lowering the cash rate to an all-time low of 2.25% in February (Figure 1). We think there are three important points that investors should take away from these events.First, it is clear that the “emergency” policy setting of 3.00% during the crisis in 2009 is now closer to Australia’s New Neutral policy rate (see the May 2013 Australia Perspectives, “Filling the Hole We Have Dug”). Second, the growth headwinds that Australia faces from both the declining prices for its exports (primarily iron ore and coal) and the declining level of mining investment are secular in nature and likely to persist for a couple of years yet. And third, due to the implications of global monetary policy for Australia’s exchange rate, the RBA is as much a passenger in this global cycle as it is a driver. In the RBA’s own words, “A lower exchange rate is likely to be needed to achieve balanced growth in the economy.” (7 April 2015 Monetary Policy Statement). We agree, and, unfortunately, this reality means the RBA has little ability to swim against the global monetary policy tide.

So what to make of February’s rate cut and the likely path for future policy? Given our view of the secular nature of Australia’s growth headwinds, February’s policy decision is unlikely to be the final installment of this cycle. However, we think the easing cycle will likely be protracted in nature rather than pre-emptive and aggressive. This is because the evidence suggests that growth is in fact rebalancing, but not yet at a pace quick enough to maintain stable employment and prices.

Growth rebalancing or growth reversal?

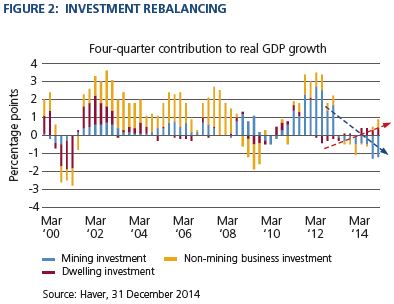

If the growth rebalancing had stalled or, worse, reversed, then this would clearly argue for a more aggressive and pre-emptive policy response from the RBA. So what picture emerges when we sift through the macro data?First, looking directly at the composition of private investment, Figure 2 clearly shows a gradual rebalancing away from the resource sector, with housing construction and non-mining business investment adding 0.9% to real GDP growth in 2014 ‒ close to, but not quite, offsetting the 1.2% drag from lower mining investment.

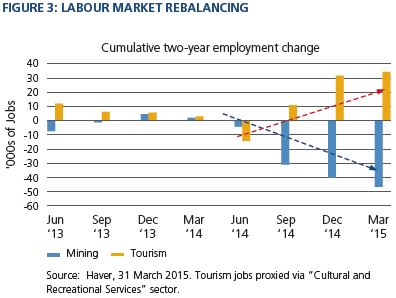

This slow rebalancing is also visible in the breakdown of employment growth by industry over the past two years. For example, as Figure 3 illustrates, the rebound in tourism jobs (+34,500 over the past two years), which has been aided by the decline in the Australian dollar, has almost, but not quite, offset the number of jobs shed in the mining sector over the same period (-46,300). Once all the other sectors are included, employment growth is clearly positive but not strong enough to absorb the growth in Australia’s labour force, resulting in a gradual rise in the unemployment rate.

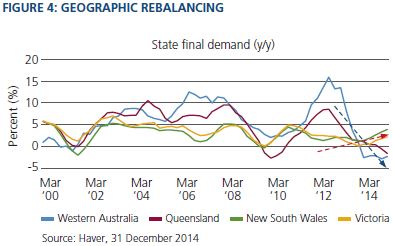

Finally, the rebalancing can be seen in the geographic composition of Australia’s real GDP growth. Figure 4 shows the acceleration in final demand growth that the two largest non-mining states (New South Wales and Victoria) are enjoying in response to the decline in interest rates and the exchange rate. Indeed, the growth in final demand in New South Wales, Australia’s largest state, has reached its quickest pace since the crisis rebound in 2010. However, once again, this is close to, but not quite, offsetting the growth drag suffered by the two large mining states (Western Australia and Queensland).

So it seems clear that regardless of how you cut the macro data, the story is consistent: Growth in Australia appears to be rebalancing, not reversing, but the rebalancing is occurring at a glacial pace that is not yet robust enough to maintain stable employment and prices.

Therefore, our baseline view incorporates a protracted easing cycle in Australia, but risks to this outlook are clearly skewed to the downside. The RBA is faced with an extremely complex set of policy options as it attempts to support the non-mining economy without exacerbating imbalances that are already present in the housing market and household balance sheets. And as we head toward the next federal budget announcement in May, there appears to be little prospect of policy support from the fiscal side. Add to this an external environment where the country’s largest trading partner, China, continues to slow and it becomes very difficult to imagine a scenario in which Australia’s growth surprises on the upside.

Investment implications

With an outlook characterized by domestic growth rebalancing too slowly, elevated policy risks and slowing growth in China, where do we see the best investment opportunities currently?Our preferred way of expressing the downside macro risks in Australia is via a short position in the Australian dollar versus the U.S. dollar. Although we think the RBA will ease policy further, this outlook appears reasonably priced into bonds, with interest rate markets indicating that the policy rate should reach 1.75% in 12 months. Being short the Australian dollar versus the U.S. dollar should also be advantageous when the U.S. Federal Reserve exits its zero interest rate policy, expected in 2015.

We also think adding euro- and U.S. dollar-denominated corporate bonds to Australian portfolios on a fully hedged currency basis is an attractive way to add credit exposure in the current environment. A reasonably constructive global growth backdrop should continue to support credit markets, and the recent widening in cross-currency swap basis spreads gives portfolios the potential to lock in additional yield when hedging the currency exposure back to the Australian dollar.