China has entered the iron ore war and how! From the AFR, Li Xinchuang, President of the China Metallurgical Industry Planning Association, is about to release an official forecast for Chinese steel consumption:

Li is forecasting Chinese steel consumption to fall by a little over 20 per cent to 560 million tonnes by 2030.

Add in a projected 50 million tonnes of exports, and you are very close to the 600 million tonnes Garnaut cited.

…by 2030 they predict China will only require about 900 million tonnes of iron ore.

That’s 600 million tonnes less than the peak forecast by BHP and Rio.

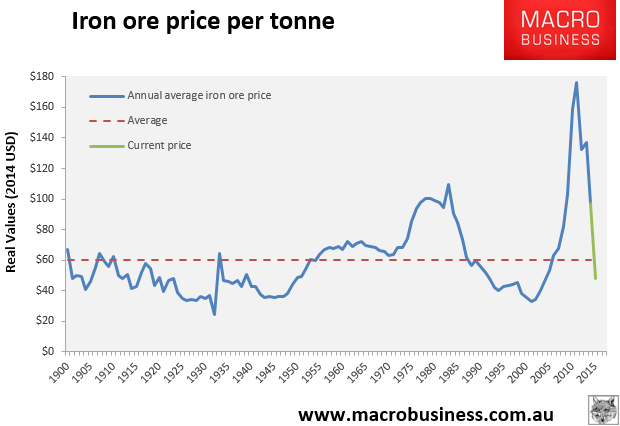

And no mention of the inevitable rise of scrap, either, which is both more clean and more cheap. For perspective, here’s the long term iron ore chart:

Remember that these are annual averages. There are long periods in between with lower prices. If dirt is headed back to its intrinsic value then we are going to see prices in the low teens again before this is over, though not immediately one would think.

Yesterday we heard rumour of new subsidies for Chinese iron ore miners, today it’s the roll back of other taxes as well, from the Global Times:

China will reduce resource taxes on iron ore to aid industrial upgrades and ensure sufficient supply, the State Council said Wednesday.

Resource tax on iron ore will be reduced from 80 percent of the taxation payment base to 40 percent, effective on May 1 this year, said a statement released after an executive meeting of the State Council presided over by Premier Li Keqiang.

More production cuts are coming but not to China! Which brings us to this peach from the Minerals Council of Australia:

Australia (MCA) has rejected the notion of capping iron-ore production in the Pilbara in the hopes of alleviating the price crash. MCA CEO Brendan Pearson pointed out to the Committee for Economic Development of Australia that Australia accounted for only 20% of global iron-ore production.

If iron-ore production were to be capped at 2010/11 levels, about A$50-billion in export revenue would be lost within just three years. “That is like losing our third-largest export – education – every year for three years. If we apply that logic to the current financial year, the one-year loss to export earnings could be about A$25-billion.

I guess Twiggy hasn’t paid his membership. The important figure for iron ore supply is seaborne production of which Australia constitutes around 66%. The MCA went on:

Pearson added that while China’s steel production was expected to fall for the first time in 35 years during 2015, projections by financial institutions suggested that this production would recover to about 15% above the 2015 level by 2020. “Australia’s commodity forecaster expects iron-ore exports, in real dollars, to be back at A$80-billion by 2019/20, up from an expected A$60-billion this year.”

Mining for consent in the big iron campaign to destroy all.