Goldman Sachs has had a go at estimating major miner margins going forward:

We believe the benefits from the current phase of cost out are more likely to accrue to the customer (through lower prices) than to the shareholder (throughmargin stability or expansion).

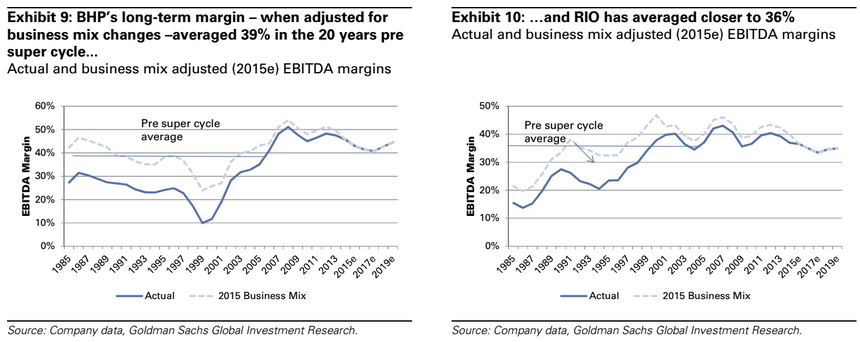

To illustrate this point, in this report we identify the differential between long-run historical (30 year) group margins for BHP and RIO…

Goldies has been the best sell side shop on the iron ore price by some distance but has not been bearish enough on prices. It is the same here.

Although a thirty year time frame can be viewed as “across the cycle” for the purposes of margin modelling, a little common sense will tell you that including ten years of the greatest mining boom in history is going to favourably distort margins a little, even coming off the back of a long cost-out period.

Advertisement

I expect major miner margins to collapse to historic lows over the next five years as excessive supply is worked off in just about everything, despite (and perhaps even because of) a more focused business mix than earlier periods.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.