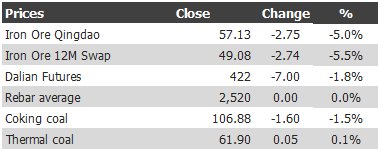

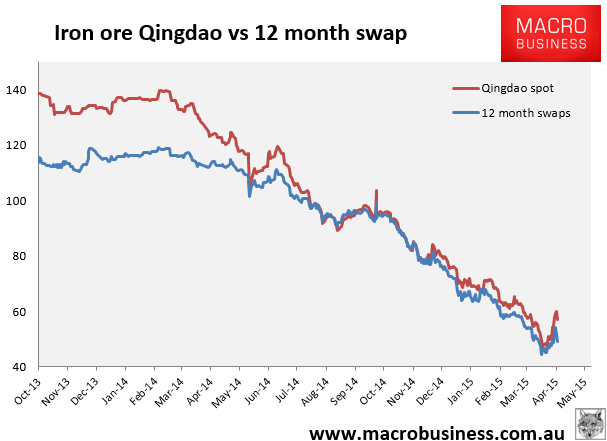

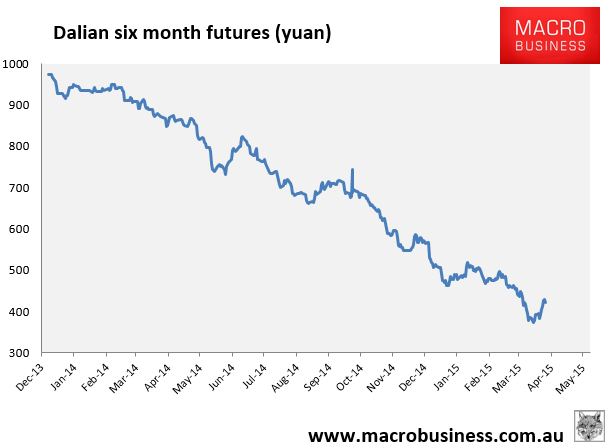

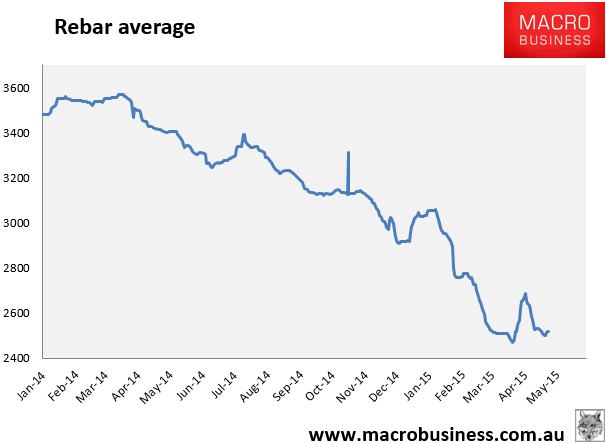

Here are the iron ore charts for April 29, 2015:

Spot was smashed with Tianjin benchmark down 3.9% to $56.90. Paper has reversed course spectacularly with Dalian down another 7 points overnight to be trading now at 415. Rebar average did not update but futures were pulverised.

Reuters has texture:

Chinese steel mills replenished run-down inventories of iron ore as prices of the raw material scaled higher, with buyers relying more on imported cargoes.

“Prices have rebounded substantially as the recent rout in spot prices forced the shuttering of a significant portion of higher cost marginal producers,” Sucden Financial analyst Kash Kamal said in a note.

“However, many industry players view the recent rally in iron ore prices as being overdone as the fundamentals still remain off balance.”

“Chinese mills have bought cargoes in recent days and we might see a pause. Sales of steel is not so good and mills still have a lot of stocks,” the trader said.

Forget fundamentals. This rally was a pump and dump when mills got short enough of ore and market players pulled sales. They’ll restock a bit and then we go lower. Or, we go lower while they restock. Nothing has changed.

In news, Cliffs is bleeding:

Headed by chief executive Lourenco Goncalves, an outspoken critic of the iron ore expansion strategy of Rio Tinto and BHP Billiton in a falling market, Cliffs said its sales margin for the March quarter was US26c a tonne.

That was down from a more respectable $US24.11 a tonne in the previous corresponding period…

…It forecast full-year production from Koolyanobbing of about 11 million tonnes. It said the cash cost of the production was expected to come in at $US35-$US40 a tonne, reflecting the benefits of cost cutting and favourable exchange rate movements.

Another dead duck but it’ll take time. Anglo has been downgraded:

In a statement yesterday, S&P said it had lowered the corporate credit ratings on the company to BBB-/A-3 from BBB/A-2 and the South Africa national scale rating to zaAA from zaAA+. The outlook is stable.

It said the stable outlook reflected its view of the limited downside to the rating over the coming 12 to 18 months, supported by the company’s expectations that it will complete its divestment programme by the end of 2016.

…Historically, the iron ore division was the main contributor to Anglo’s Ebitda, making up about 30 percent in 2014.

“Under our new price deck, we project material drops in the contributions from Kumba Iron Ore, the owner of Anglo’s legacy iron ore assets, and from the new Brazilian greenfield mine Minas Rio,” S&P said.

Expect the outlook to change to negative again. Kumba is low cost but Minas Rio is very expensive. Big writedowns are coming there and a rush to increase volume to lower unit costs.