Nothing terribly new here but illustrative of the shift away from poor Fortescue. Charlie Aitken’s Bell Potter has downgraded FMG today from buy to hold. I can’t offer more than that given I’ve been cut from Charlie’s mailing list but it seems to me in some way important given his steadfast support of the failing miner.

As for US bonds, the AFR plays catch up:

US investors are selling out of billions of dollars of Australian mining companies’ bonds and loans as plunging iron ore and coal prices makes it less likely they’ll get paid back.

The US bonds issued by miners Fortescue Metals Group and St Barbara and mining services companies Emeco and Ausdrill are trading at discounts to par value of between 74¢ and 85¢, according to Bloomberg data.

The paper losses reflect a change in fortunes for Australian miners that seized on the opportunity to raise money created by the convergence of rising commodity prices driven by Chinese growth and cheap funding as a result of US quantitative easing.

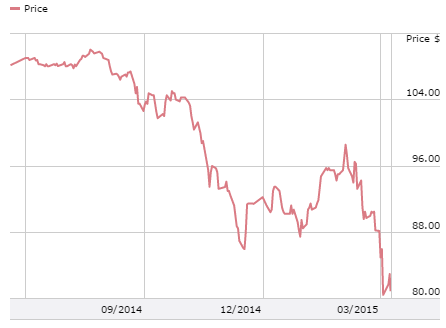

Old news of course but here are the latest charts, for 2019:

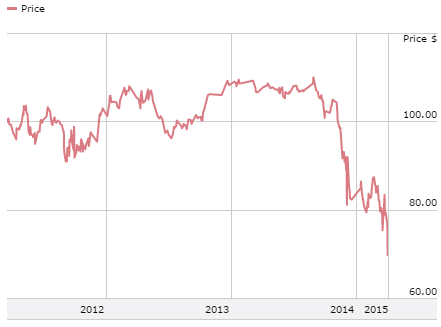

And even worse, 2022:

What’s interesting about this is that the longer the maturity the lower the rate of recovery, which is the opposite of consensus earnings forecasts from equity shops. Can’t both be right!