The FT had an interesting piece on the one of the world’s largest commodity funds over the weekend:

The troubled BlackRock World Mining investment trust has taken on a new co-manager, cut fees, imposed stricter investment guidelines and apologised to shareholders after a year of steep underperformance.

The 21-year-old trust, whose lead manager is the veteran commodities investor Evy Hambro, shed 26.4 per cent of its net asset value in 2014, against a 13 per cent fall for the Euromoney World Mining index, making it the worst year in its history.

…the fund had recovered strongly from previous dips in performance, such as during the global financial crisis, and added that it “offers some value for contrarian investors”.

Mr Hambro and Ms Raw said: “Last year we had expected an improving world economy to support commodity demand, and in turn commodity prices. Sadly, supply growth managed to overwhelm demand and resulted in many commodity prices falling sharply.”

Wrong. This is not a GFC event and three factors are in play in the mining bust with excess supply only one half of one of them. Even if global growth improves (which is highly questionable) its constitution is changing. As developed economies rise from their knees, China is very obviously slowing and shifting to less commodity-intensive growth and will need less of everything that is dug up in the future (with the exception of foodstuffs):

The build-out in the supply of hard commodities was based upon a very different forecast for investment than what has transpired leaving everything in enormous oversupply.

The second reason is that the US dollar is in a secular bull market adding a monetary headwind to commodity prices. It will ebb and flow but even as the business cycle matures and we enter the next global shock it will soar. This is reason alone to wait on buying miners, but even after the next shock and QE4 the US will still very likely be the economy in the best shape globally, meaning the dollar can run for a long time:

The third reason derives from the first two and is, ironically, one in which Evy Hambro is a key player. In the past cycle, markets went nuts for commodities, redefining them as a discrete asset class worth holding for higher prices across the cycle. This led to enormous derivative-based hoarding which must now unwind as the reality of the boom and bust cycle bites:

These three reasons mean hard commodity prices face unusually large structural headwinds in demand, supply and finance overlaying the cycle. There will be a time to buy to benefit from cyclical volatility but you can expect commodity producers to underperform the broader market for another full business cycle so it’s not a buy and hold play. Mr Hambro is the wrong side of a super-bust and it’s going to get worse for him.

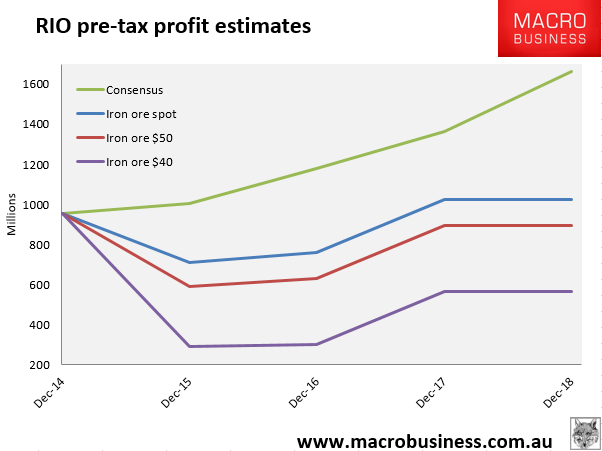

One of BlackRock’s largest holdings is the roughly 8% it has in RIO shares. That has held up well so far given the headwinds but with iron ore plunging to the mid-$50 and twelve month swaps now into the $40s, RIO’s future profits are going up in smoke:

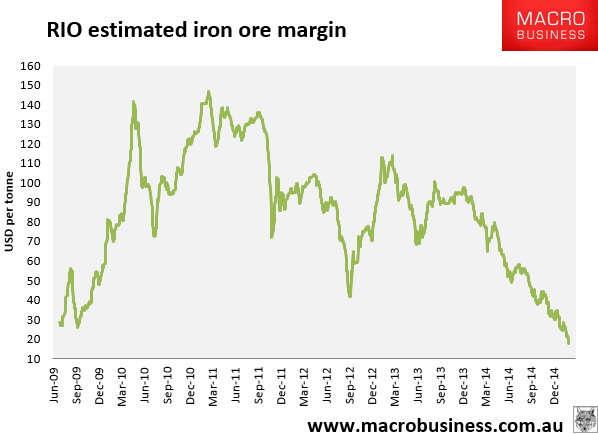

If current prices hold and assuming $2 billion in non-iron ore profits (which is generous), RIO will have an after tax profit of $4.5 billion, barely enough to cover the dividend. Iron ore is 80-90% of RIO’s profit and its margin is collapsing:

Does that look like RIO cost-out is keeping pace with iron ore price falls? We’ve crashed from a 300% margin per tonne at the 2011 peak to a 30% margin today. That may seem still fat. But there is an asymmetric impact for price falls at this level. At 300% a $1 fall was irrelevant, now, every time the price falls the same amount the margin is hit 6% and it get bigger with each fall. The RIO share price has held up on the yield trade that is suppressing risk pricing but in reality risk around RIO is exploding.

The same points can be made for thermal and coking coal and a bunch of industrial metals. As mining’s structural adjustment plays out the only three investment plays that makes sense are short, shorter or shortest.