China released its Jan/Feb data last night (which is combined to overcome CNY distortions) and, boy, did it underwhelm. Industrial Production came in at 6.8% y/y versus 7.7% expected and down from 7.9% in December:

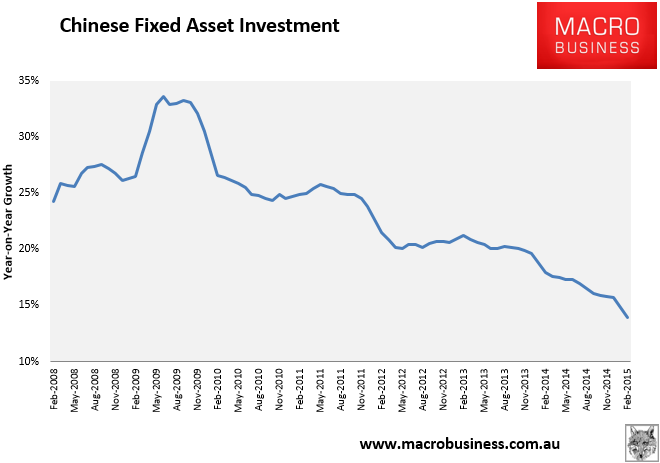

The really crucial measure for Australian bulk commodity exports, steel production, came in at -1.5% y/y. Driving that, fixed asset investment growth is falling fast, in at 13.9% y/y versus 15% expected and down from 15.7% in December:

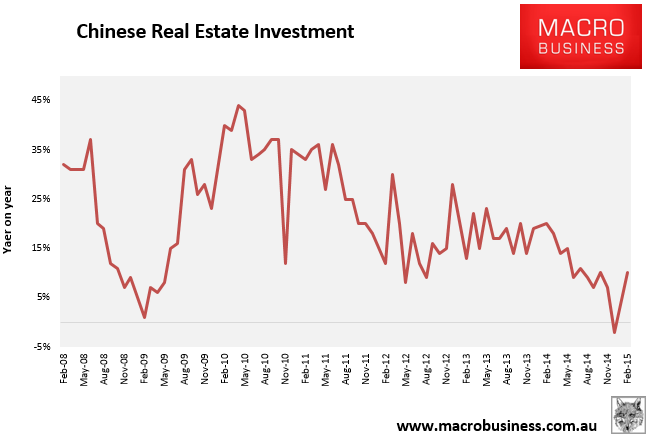

Real estate investment is still falling as well. China’s housing sales in the first two months of the year slid 16.7%y/y with sales at 498 billion yuan versus 598 billion last year. Growth in property investment also slowed to 10.4% versus 19.3% growth a year earlier. But that was at least a big rebound from December’s sub-zero result. For 2014, property investment rose 10.5% so the first two months were consistent with last year’s growth rate. However, new residential and commercial starts fell 17.7% and floor area fell 10.7% for the comparable period:

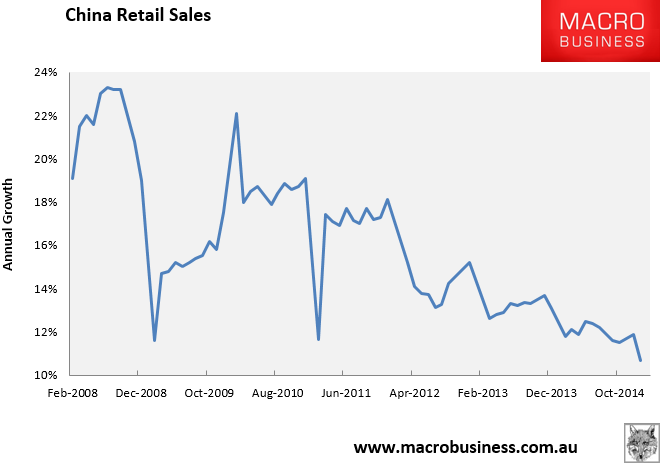

Even nouveau China as represented in retail sales were weak, coming in at 10.7% y/y versus 11.6% expected and down from 11.9% in December, though is some questions around the role of the falling oil price:

As you can see in the charts above, the first two months are often something of a data reset from which slowing tends to ease. But more stimulus is still very likely with these figures. Even so, the lack of traction from stimulus to date suggests strongly that the “about 7%” growth target will be at the bottom of any rough range, perhaps at 6.5% for the year ahead.

This is not what you’d describe as a “hard landing” in aggregate. There’s no sudden stop going on. But the slowdown in the specific areas of the economy important to Australia – investment growth and industrial production around steel – is much worse, especially in real estate which appears headed for 5% growth or below this year from 30% plus a few years ago, as well as real falls in steel activity.

None of the glass half-full bluster about China growing from a bigger base can distract from the fact that this is, in effect, Australia’s China entering a hard landing.