From APRA chairman Wayne Byers today:

Sound Lending Practices for Housing

When we made our last appearance, we were still contemplating potential actions with respect to emerging risks in the housing market. We have since written to all authorised deposit-taking institutions (or ADIs) encouraging them to maintain sound lending standards, and identified some benchmarks that APRA supervisors will be using in deciding whether additional supervisory action – such as higher capital requirements – might be warranted.

I would like to emphasise that, in alerting ADIs to our concerns in this area, we are seeking to ensure emerging risks and imbalances do not get out of hand. We are not targeting house price levels – as I have said elsewhere, that is beyond our mandate – and we are not at this point asking banks to materially reduce their lending. We have identified some areas where we have set benchmarks that we think will be useful indicators of where risk could be building, and in doing so, will help reinforce sound lending practices amongst all ADIs. We are currently assessing the plans and practices of individual ADIs and, over the next month or so, will be considering whether any supervisory action is needed. So far, our discussions with the major lenders have suggested they recognise it is in everyone’s interests for sound lending standards to be maintained. But we shall see – we are ready to take further action if needed.

Financial System Inquiry

Beyond this immediate issue, we are also giving thought to the more fundamental issues in relation to ADI capital contained in the recommendations of the Financial System Inquiry. There are two key influences on how we will proceed on these issues: first, the submissions made through the Government’s consultation process, and second, the work still underway on a number of related issues in the international standard-setting bodies, particularly the Basel Committee on Banking Supervision.

Helpfully, the FSI and the international work are pointing us in the same direction. There are, however, complexities in the detail that we need to work through carefully. In terms of timing, we do not need to wait for every i to be dotted and t to be crossed in the international work before we turn our minds to an appropriate response to the FSI’s recommendations. But it will be in everyone’s interests if, over the next few months, we are able to glean a better sense of some of the likely outcomes of the international work before we make too many decisions on proposed changes to the Australian capital adequacy framework.

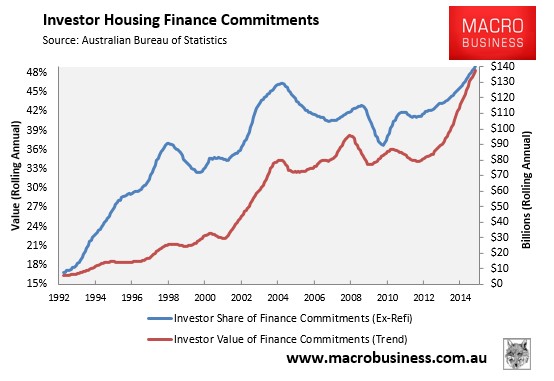

It’s no wonder the RBA is leaking no cut. This is incredible dithering. Recall the chart for perspective:

No macroprudenital tightening yet and no move on Murray Inquiry recommendations, either.

The bubble is wildly our control, still accelerating in Sydney, is holding the entire tradable economy hostage and threatening the turn the post-boom adjustment into a monumental crash.

But APRA appears to have turned from systemic risk manager to bubble manager for fear of bringing the economy down.

That will not end well.