Greece and its Euro area counterparties continue to work within a tight schedule to avert a disorderly outcome. Our base case remains that some new accommodation will eventually be found between Greece and the European authorities. But risks of an accident remain. Even if an agreement to extend the programme is reached this week, the gap between the demands of the Greek side and the programme requirements is very large.

If tensions turn systemic, EM assets likely to see pressure

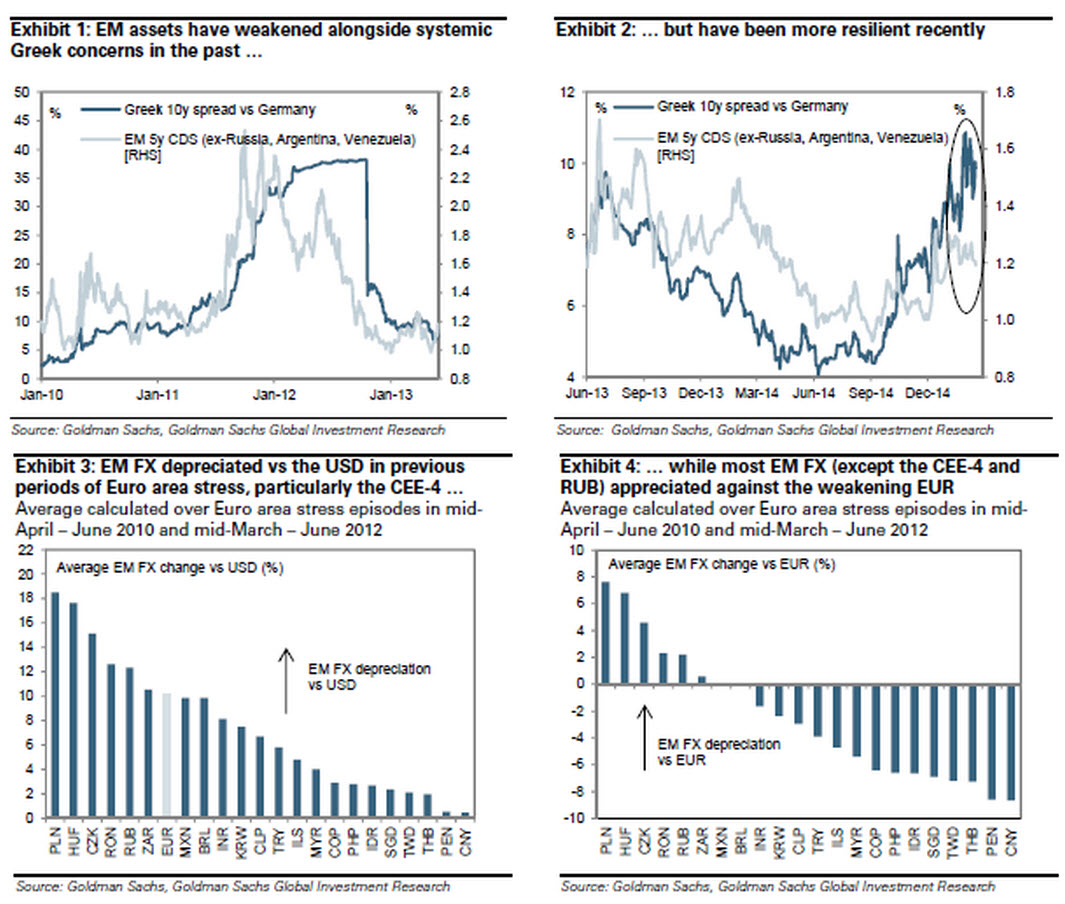

Even as Greek concerns have escalated, risk markets have so far traded in a resilient fashion, treating those concerns as effectively isolated to Greek assets. But in previous episodes of acute Euro area stress in 2010 and 2012, a wide range of EM assets came under pressure, especially CEE FX and CDS. Hungary was the hardest hit across all asset classes.

To hedge Greek risk, long $/CEE

Among EM, $/CEE has seen the largest moves in times of Euro area stress. This has reflected a weakening EUR and EUR/CEE moving higher. Specifically, the HUF and PLN are likely to depreciate against the USD in the medium term as policymakers welcome weaker currencies in the fight against ‘lowflation’, and would move even more rapidly if Greek risks do become systemic. Locally, the entry levels are also attractive given the rally in EUR/CEE in recent weeks.

Hedging Greek risks in EM assets

Euro area sovereign and financial risks rising again

The nearly constant barrage of headlines reporting comments from Greek and Euro area policymakers is indicative of the renewed deterioration in sovereign risk. Greece and its Euro area counterparties continue to work within a tight schedule to avert a disorderly outcome. Our base case remains that some new accommodation will eventually be found between Greece and the European authorities. But risks of an accident remain as commercial bank deposit outflow and a shortfall in tax collections can precipitate a critical situation in the interim. Even if an agreement to extend the programme is reached this week, the gap between the demands of the Greek side and the actual programme requirements is very large.

The situation is fluid, and if an agreement is reached quickly to extend the Greek bailout, then broader asset markets (including in EM) should stay largely unaffected. But we continue to receive questions on how EM investors can consider hedging the risks of a more messy outcome – that either leads to a ‘no man’s land’ where Greece is without the funding that comes along with a programme or, in the worst case, an outright exit from the common currency. In these latter outcomes, with systemic risk likely to increase, EM assets would come under pressure.

Three weeks ago, we described how in previous episodes of Euro area turmoil, on average EM bond yields tracked the move lower in G3 yields as demand for safe assets spiked, whereas EM credit spreads widened, EM FX weakened versus the USD and EM equities came under broad pressure (see ‘Taking one step back’, EM Weekly: 15/03, January 29, 2015). That said, both EM and G3 bond yields are now at much lower levels – which makes the argument for being long EM fixed income more debatable in the current context. In this EM Weekly, we drill further down within EM FX, CDS and equities to evaluate the relative performance across countries over those previous episodes to help identify how best to protect portfolios against an escalation in Greek risks.

The EM asset experience in the 2010 and 2012 episodes of Euro area stress

Even as concerns around the extension of the Greek programme have escalated, risk markets have so far traded in a resilient fashion, treating those concerns as effectively isolated to Greek assets. But in previous episodes of acute Euro area stress, a wide range of EM assets came under pressure as risk traded poorly. Below we study the two previous episodes of Euro area stress in 2010 and 2012 to assess how different EM assets were affected on average. Euro area stresses were also elevated in 2011, but in that episode it is harder to distinguish between the impact of the Euro area worries and the US debt-ceiling crisis, which played a major role in roiling markets.

Starting with EM FX, Exhibits 3 and 4 show the average moves versus the USD and the EUR over the two periods when Euro area stresses were at their most acute: mid-April to early June 2010 and mid-March to early June 2012. Exhibit 3 shows that in these ‘risk-off’ periods, almost all EM currencies depreciated versus the USD. In relative terms, the largest average depreciations were recorded in the Central and Eastern European region (PLN, HUF, CZK), followed by a couple of the high-yielders (RUB, ZAR) in the European time-zone. The MXN and BRL were most affected in the LatAm region, whereas NJA currencies outperformed.

Most EM currencies appreciated versus the EUR (Exhibit 4), which is unsurprising given that the Euro area was the epicentre of the shocks at these times. But, notably, the CEE-4 currencies saw meaningful depreciations versus the EUR, even as the EUR itself was depreciating. The geographical proximity and the strong trade and financial linkages of the CEE region to the Euro area meant that currencies there have tended to bear the brunt of Euro area crisis episodes.

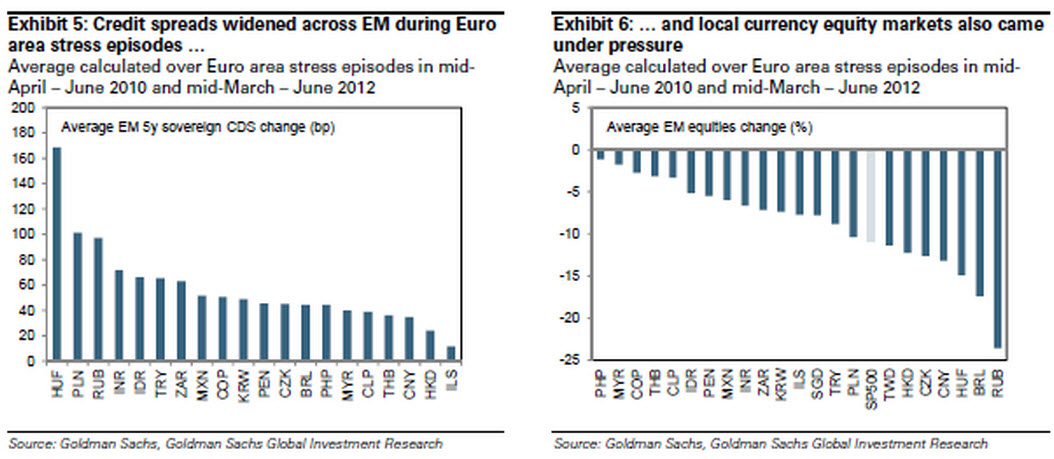

Turning to EM CDS, we find some similar patterns (Exhibit 5). On average across the two episodes, Hungarian 5-year CDS saw the largest widening (170bp), followed by a smaller but still significant widening of about 100bp in Poland and Russia, and then by the rest of the high-yield complex. Again, NJA CDS spreads in general were the least responsive to Euro area risk. Within EM equities (Exhibit 6), Russian equities were the hardest hit, with nearly a 25% decline, and CEE equity markets were also more negatively affected than the rest of the EM complex. The outperformance of NJA is less stark in this case, with a number of major markets, including China (H-Shares), Hong Kong (HIS) and Taiwan (TWSE), all seeing double-digit percentage declines.

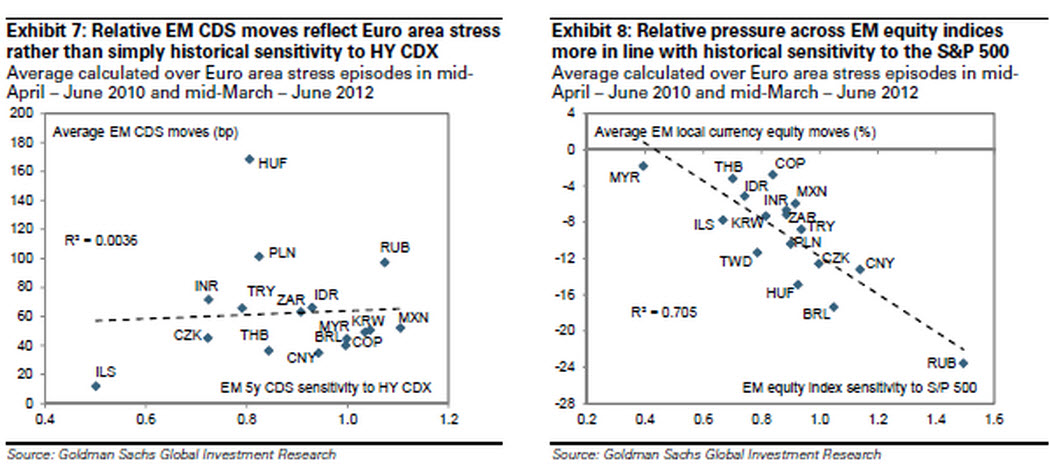

Setting these moves in credit and equities in individual EMs against their historical sensitivities to benchmark DM indices suggests that in the past there has been more idiosyncratic pressure in the credit space relative to equities. Exhibits 7 and 8 show that, whereas the relative pressure across EM local currency equity indices is more straightforwardly reflective of the historical sensitivity to the S&P 500 index, the relative EM CDS moves are more idiosyncratic. In other words, the relatively large movers here –such as Hungary, Poland and Russia – offer a more targeted and less market-dependent way to hedge Euro area risk.

Taken together across all three asset classes, Hungary was the hardest hit, while the rest of the CEE and Russia experienced a similarly strong negative performance overall in their asset markets through these periods of heightened Euro area stress.

$/HUF and $/PLN weakening our preferred ways to hedge Greek risks

At the current juncture the market appears to be making a couple of assumptions: first, that the ongoing disagreements between the Greek government and the Eurogroup represents the typical political posturing that has tended to take place in advance of eventual eleventh hour agreements; and, second, that in the event that agreement cannot be reached by the end of February, the upgraded EU toolkit, including the OMT and the soon-to-be-initiated sovereign QE, will keep market pressures from spilling over into the rest of the EU periphery, and by extension into the broader market.

Our read of the situation is less sanguine on both counts. An eventual agreement between the Greek government and the Eurogroup is still our base case, but we worry that the gap between the current programme on offer and what would be acceptable to a majority of the Greek parliament is very large. In addition, market pressure has often been the forcing variable in the past in helping to close this gap, so paradoxically the absence of broader market pressure is likely to make an eventual agreement that much less likely. In the event that an agreement cannot be found, and ‘Grexit’ becomes a serious possibility, we would expect systemic concerns to affect markets more broadly than currently. As Francesco Garzarelli discussed (in Global Markets Views: ‘Systemic risks posed by Greece set to peak at month-end’, February 17, 2015), even if peripheral bonds are shielded from the fallout by the ECB’s purchases, we would expect the EUR and stocks to come under downward pressure, and credit spreads to widen, reflecting the downside risks to a fragile economic recovery in the Euro area.

Given the results documented in the previous section, our preferred way to hedge these risks would be through long $/CEE positions. In previous episodes of Euro area stress, the combination of the EUR moving lower versus the USD and EUR/CEE moving higher has meant that $/CEE has tended to see the largest moves across the EM FX complex. Even setting aside Greece-related risks, our forecasts call for EUR/USD to move to 1.11, EUR/PLN to weaken to 4.22 and EUR/HUF to weaken to 320 in 6 months, as policymakers in these economies welcome or actively seek weaker currencies in their fight against ‘lowflation’. This implies that the HUF and PLN are likely to weaken against the USD in the medium term based on macro and policy considerations, and if Greece-related risks turn systemic, the weakening is likely to be even more rapid. Finally, given the rally in EUR/HUF and EUR/PLN over the past three weeks, locally the entry levels are also much more attractive.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.