It’s hysterical stuff today at Dad’s Army. Alan Kohler reaches for the Bible:

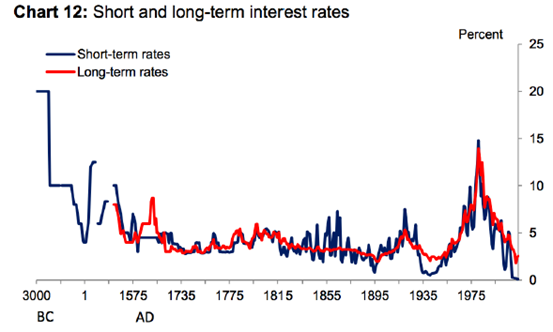

And when I say “ever”, I mean just that, as this amazing chart from a speech last week by the Bank of England’s chief economist, Andy Haldane, demonstrates. It shows global interest rates back to 3000BC, when construction workers started building Stonehenge, Troy was founded and Djet became the fourth Pharaoh of Egypt, replacing Djer, who passed away.

Interest rates have never, ever been this low.

So to sum up: savers and workers are being crushed; owners of assets are big winners.

Are they? Not according to Gotti today (or Kohler the other day, for that matter):

I am not forecasting that they will lead to a recession but we are in uncharted territory.

We will start with last night’s stark warning from ANZ Banking Group that investment in resource projects is set to fall from $76 billion in 2013 and $61 billion last year to just $10 billion in 2017…

…what might fill the gap is the unprecedented investment by the Chinese in apartment development, particularly in Victoria…This Chinese-led apartment boom is now vital to Australia, given the timing.

…But the voters don’t like the Chinese/Asian ‘invasion’ so Tony Abbott, desperate to salvage his position in the opinion polls, is planning to undertake a whole series of clampdowns on foreign buying…That’s likely to really hit the one thing standing between Australia and a recession

Advertisement

And is keeping that spiggot open a solution, Gotti? Self-evidently, not.

It’s not the content of these ramblings that matter, it’s the tone and narrowness of the perspectives. These are clunking cogs spinning off axis in a failing machine. Commenter Pfh007 summarised it beautifully this morning:

Expect it to get very incoherent as defunct economic models (Neo-lib attitudes to trade and capital) crash into the politics of recession (worried locals).

Exhibits

1. Mr Robb signing predatory capital inflow facilitation agreements (FTAs) to assist the FIRE industries that export – capital assets, industry, land and financial claims on public and private income AT THE SAME TIME as Abbott and Kelly try to hose down the issue in relation to residential real estate.

2. Population ponzi and guest workers (457 visa) and golden ticket migrants (SIV) AT THE SAME TIME as rising unemployment.

3. Residential Asset price pumping programs (ZIRP) AT THE SAME TIME as pumping supply to try to provide some employment options in residential construction.

The ability of the politicians to ‘hide’ the very real consequences of an economic model that involves supporting a standard of living with off shore debt (public and private) – “….interest rates will always be lower….” i.e. living on debt – is starting to fail.

The day middle Australia finally gets to the OMG moment is getting closer.

Beads of sweat on the brows of Treasurers, finance ministers and RBA governors are the best index.

Joe Hockey is already sweating bullets and I reckon even Mr Morrison looked a bit twitchy on the 7.30 report last night.

Advertisement

That’s it with a cherry on top. We’ve seen nothing yet. As Australia’s current account deficit model slowly comes apart, all manner of hysteria will rise. Pass the popcorn.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.