We have an answer for all of those dills that argued a rate cut would kill consumer confidence. From Bill Evans at Westpac:

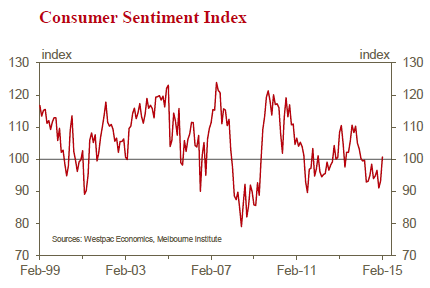

• The Westpac Melbourne Institute Index of Consumer Sentiment increased by 8% in February from 93.2 in January to 100.7 in February.

This is a much stronger result than we had expected. It represents the first time since February last year that we have seen a majority (albeit miniscule) of optimists over pessimists. It is also the highest level of the Index since January last year.

It is probably best to assess the progress by noting that the level of the Index is now 1% above its reading in April last year.

That was the last reading prior to the May Budget after which the Consumer Sentiment Index plummeted 6.8%. Up until today, confidence had struggled to make up any ground following that shock.

There have been a number of important reasons why consumer sentiment has been boosted. Firstly, the Reserve Bank cut the overnight cash rate by 0.25% in a move that was not widely expected in the media or by the markets. This lift in confidence should allay any concerns that rate cuts, in the current environment of record low rates, can be a negative for confidence. The idea that households would be unnerved by the implication that authorities might be responding to a surprise deterioration in economic circumstances seems to be strongly disputed by this result.

However, rates were not the only reason behind the big boost to confidence. Lower petrol prices and a surging sharemarket also appear to have had an impact. The 21% fall in average petrol prices over the last two months is the largest two month fall in prices since December 2008. Similarly, the 9.7% rise in the share price index since the January survey is the biggest one month rise in the sharemarket since August 2009.

The importance of these last two factors is highlighted by the surprisingly modest 0.7% increase in the confidence level of those respondents holding a mortgage – a group that is typically the most sensitive to interest rate changes.

However, not surprisingly, the rate cut has strongly boosted confidence in the housing market. The index tracking views on ‘time to buy a dwelling’ jumped by 9.7% to reach its highest level since February 2014. Similarly, the index of house price expectations jumped by 6.9% to reach its highest level since September 2014.

One concern around today’s results was whether the unrest in Government would weigh on sentiment. It certainly showed in a sharp fall in the confidence amongst Coalition voters but confidence of ALP supporters, third party voters and the ‘undecided’ was boosted sufficiently to deliver the overall positive result.

All five components of the Index increased in February. Views about finances were buoyant with the sub-index tracking assessments of ‘finances vs a year ago’ up 12% and the sub-index tracking expectations for ‘finances, next 12 months’ up 7.6%. The economic outlook also improved sharply with the sub-indexes tracking expectations for ‘economic conditions, next 12 months’ up 10.3%; and ‘economic conditions, next 5 years’ up 13.3%.

The sub-index tracking assessments of ‘time to buy a major household item’ was steadier, up only 0.5%.

A notable and disturbing aspect of the Consumer Sentiment Survey for the last two years has been the consistently high reading for the Westpac Melbourne Institute Unemployment Expectations Index. This has consistently signaled that respondents fear a significant lift in the unemployment rate and hence feel very insecure in their jobs. Undoubtedly that unease has been weighing on spending decisions and holding up the savings rate despite a squeeze on incomes. The Unemployment Expectations Index fell 1.9% in March. While that marks an improvement (lower readings indicate reduced fears of a rise in unemployment), it is a disappointingly modest one given the very weak starting point and the other very strong aspects of this survey.

The Reserve Bank Board next meets on March 3. When Westpac revised its rate view on December 4 we expected consecutive rate cuts in both February and March. The February cut has been delivered and the Bank, in setting out its growth and inflation forecasts in its February Statement on Monetary Policy (SoMP), has almost certainly guaranteed a follow up cut by assuming a further cut when formulating those forecasts. Markets fully expect that cut to be delivered by May.

This survey definitely points to improved confidence in the housing market and the Bank did note in its Statement that: “housing market developments will need to be watched closely”.

However the impact of the improvement in confidence more generally needs to be tempered. The initial positive sentiment response to rate cuts can often dissipate in following months.

The ongoing unease around employment security and likely soft growth in incomes also suggests the rise in confidence will see a more muted impact on spending.

For now, we are comfortable to maintain our original call for a follow up move in March, particularly given the Bank’s comfort with its initiatives in the regulatory sphere (the SoMP noted: “The Bank is working with other regulators to assess and contain economic risks that may arise from the housing market”).

However we recognize that a perfectly respectable case can be made for the Bank to pause for a month or two to assess developments in the housing market.

The most important point is that February is not the end of this rate cut cycle with another cut extremely likely over the next three months.

Never underestimate the impact of rate cuts on the Australian mortgage addict! However, as good as this sounds, I expect it to fade fairly quickly without more rate cuts. The sharemarket will stall without further easing given it’s only running on a lower yield environment. It plunged on the release!

I don’t expect a resurgent housing market, either, just support to slow the decline in growth.

Advertisement

The survey was taken across all of last week so will not have picked up all of the political chaos. Having said that, you never know, consumers may love the end of austerity much more than they hate Abbott.

Another sugar hit to pass in time. The Aussie largely agreed rising a lousy 14 pips, thankfully.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.