Back in May 2008, nobody — especially regulators — had a clue about what was causing crude oil prices to spike to $100-per-barrel-levels, and mostly everyone was inclined to either blame “China” or “speculators” or some combination of the two.

But Michael Masters, a portfolio manager at Masters Capital Management, had a simple proposition. In the Senate committee hearings organised to figure out exactly what was going on, Masters testified that it was his belief that a new class of investor — one he dubbed the passive “index speculator” — had bulldozed his way into the market and distorted the usual price discovery process.

This index speculator, he argued, differed to the usual sort in two major ways; their strategy was as immense as it was predictable, involving a simply huge allocation of dollars across 25 key commodities in routine bursts. And, he added, “while the commodities markets have always had some speculators, never before had major investment institutions seriously considered the commodities futures markets as viable for larger scale investment programs.”

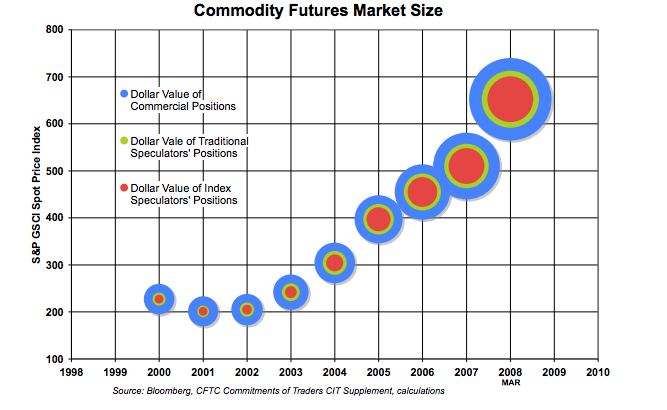

His testimony included the following chart (click to enlarge):

But as Masters explained to FT Alphaville on Monday, the core part of his argument was always based on the notion that prices respond to order flows irrespective of whether they are speculator or hedger driven. Furthermore, he added, the inelastic nature of the oil market has always meant it can take a very long time — people’s entire careers — for imbalances to be corrected, something that understandably allows for serious mispricings to last a very long time.

“There’s a temporal difference between speculative flows and price formation, and supply and demand flows,” Masters said. “It takes a long time for supply to be added, even if the price goes from $30 to $50, it takes management a long time to believe that the price is going to stay there. It may take them a year or two to actually add supply.”

In the past, every time crude got as high as $30, he said, the market would add production very quickly. But this only meant the price would instantly spring back to $10. This, over time, created a sequence of affairs that taught producers to ignore the $30 production pressure point, leading to a sort of self-imposed production strike until prices were high enough to really make producing more volume truly worth while. These factors, Masters said, were magnified when risk-averse passive investors decided about the same time that commodities were something they could invest in as a speculative asset.

And that’s really where we are today, according to Masters. At a stage where innovation has corrected a historic imbalance, and produced efficiencies which won’t just disappear overnight. If anything, he noted, such efficiencies might accelerate, meaning it’s probably a mistake to bet on a price recalibration any time soon.

“Efficiency and innovation, when price falls, it accelerates, because necessity is the mother of invention,” Masters said. “Even if the investment only spits out quarters, or even nickels, you don’t turn it off. And that’s really the debate that is going on right now.”

In other words, real global money moved into commodity hoarding. And that build prices to epic highs as Chinese demand acted as a real force on demand and the falling US dollar added a monetary tailwind.

These are classic bubble dynamics. A kernel of investment truth, pumped up by wildly easy credit, then rising to extremes simply because prices are rising, the last made all of the more obvious by the asset in play having zero yield.

As both the underlying demand story and the easy credit are now in reverse (relatively speaking) so too is the hoarding, and price discovery to the downside is the new name of the game.

Bubble meet bust.

The commodity super-bubble and bust

David Llewellyn-Smith

Wednesday 4 February 2015

Advertisement

About the author

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

Advertisement