Through cost out, FX and oil price Fortescue has stayed ahead of the declining iron ore price. Our positive stance relies on the iron ore price rising; FMG can survive at lower prices but the investment case is compromised. Contrarian OW retained, with attention firmly on the iron ore market.

Where do we see breaking point now? At a US$63/t spot price (scenario pg 4) the US$46/t all-in cost we project, which includes tax, interest and dividends, leaves a US$1/t margin. This carries a ~US$3/t buffer on the spot freight price so a sub-US$60/t iron ore price is where things become untenable in our view.

The revenue non-mismatch: Using quarterly realised price and volumes there was a US$124mn, or US$1.5/t, shortfall in revenue (US$4.8bn). The difference being some FOB sales, which net off at the cost line, and quotational pricing which should normalise over time.

Still has cash in reserve: A tax payment catch-up came in below the provision, due to a favourable FX translation and extra prepayments saw FMG end the half with US$1.5bn in cash. In this context retaining a modest dividend was reasonable in our view. Gearing is still high at 50% (ND/ND+E), but holding back US$0.2bn in dividends wouldn’t change this.

Where could FMG surprise? Further cost-out or incremental sales, as we have flat assumptions for both. The Iron Bridge JV gets almost no value in our NAV – successful commissioning of the 1.5Mtpa pilot plant would be an incremental positive. Further prepayments incoming used to reduce debt would also be beneficial.

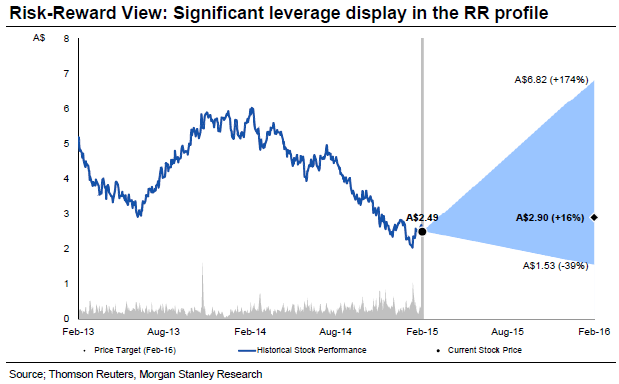

That’s all gobbledygook, really, if the iron ore price rises it will fly for sure on its reduced cost base. But the price has to stay high to deliver the earnings, which is very unlikely, so the percentage play is surely to short spikes not go long dips.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.