Yesterday, while reading Interest.co.nz’s Top 10, I came across an interesting article published last month in The Economist, which explained how for decades banks in developed nations have been boosting mortgage lending at the expense of businesses, hurting entrepreneurship and productivity in the process:

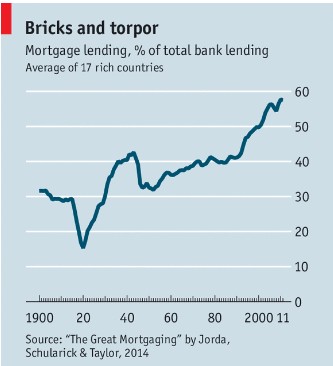

… the traditional view that banks primarily lend to businesses is out of date. In 1900 only 30% of bank lending was to buy residential property; now that figure is around 60% (see chart). Since the 1970s virtually the entire increase in the ratio of private-sector debt to GDP around the world has been caused by rising levels of mortgage lending. Corporate borrowing has remained flat. Far from channelling money to companies, modern banks resemble “real-estate funds”… in which long-term mortgage lending is funded by short-term borrowing from the public.

The full text of this article is available to MacroBusiness subscribers

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.