A new report by the Actuaries Institute finds that the tax burden and private health insurance costs facing younger generations will rise dramatically in order to pay for the health needs of an escalating number of older Australians:

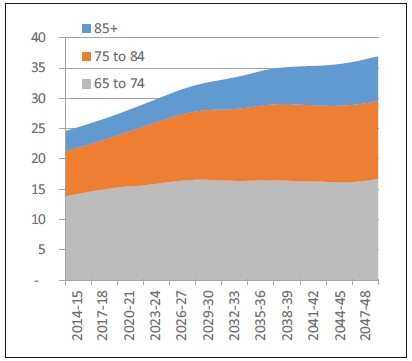

Health care costs rise dramatically with age – health expenditure for an 85 year old Australian is more than four times that for a 50 year old. By 2049-50 the number of Australians over 85 will more than triple…

Ageing is the most predictable factor which will influence future health expenditure. It is a key factor that affects our ability to fund health care…

Our population is predicted to live significantly longer and forecasts indicate that spending on health care across all levels of government is expected to grow from 6.5% to 10.8% of GDP over the next 50 years…

Health care remains almost entirely funded on a pay-as-you-go basis and largely through general taxation. Pre-funding of future health care needs is virtually non-existent.

Total expenditure on health goods and services in Australia was an estimated $147.4 billion in 2012–13 (9.7% of GDP). Currently 68% of health expenditure is funded by Australia’s various levels of government…

Some intergenerational cross subsidy is an inevitable part of our health care system (as it is with other services) but the cost on the working population through taxation needs to be addressed in order to protect the quality of Australia’s health care services and system.

Working age people will be supporting the health care costs of an increasing number of older people. By 2049-50, there will be twenty people aged 75 and over for every 100 working age people, compared to ten now. For the over 85s, where health care costs rise dramatically, there will be seven people aged 85 and over for every 100 working age people, compared to just three now.

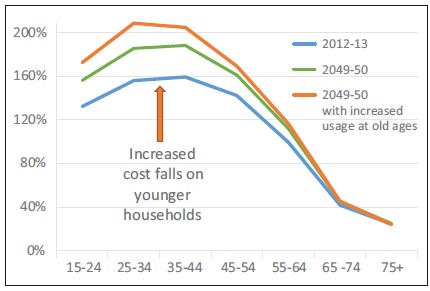

Without policy action, the working population may be paying almost double their own health expenditure to subsidise older Australians compared to a current rate of 1.4…

The report then outlines three possible reforms to help cope with the rise in demand for health services by older Australians:

encouraging older generations to work longer;

establishing health savings accounts; and/or

drawing on retirees’ wealth to self-fund healthcare costs.

Advertisement

On the last option – drawing on retirees’ wealth to self-fund health costs – the Actuaries Institute notes:

By 2030, almost half of household wealth will be in the hands of the over 65s. This fact leads to the question does it make sense, and is it equitable, to ask this cohort to pay more to help fund future health care costs? The major reforms to the funding of aged care – Living Longer Living Better – which came into law on 1 July 2014 focus on just this issue. These reforms include a greater emphasis on ‘user-pays’ with increased means testing arrangements along with fee caps and lifetime limits.

The challenges in health care provision are unique, and a ‘user-pays’ approach could lead to higher mortality and poor health outcomes. Solutions to address this question will need to be equitable, practical and acceptable to the community whilst ensuring that all Australians have access to free or low-cost health care, consistent with Medicare’s aims.

While I agree with the thrust of the Actuaries Institute‘s report, in my view there is a simpler and fairer solution to coping with Australia’s rising health costs.

Advertisement

First, reform the tax system, so that the base is broadened and the burden is shifted away from workers (via inexorable rises in personal income taxes) towards consumption (e.g. raising/broadening the GST, along with compensation for the poor), wealth (e.g. land taxes), and resources (e.g. greater resource rents taxes).

Second, close Australia’s inequitable and poorly targeted tax concessions – such as on superannuation, negative gearing, and capital gains taxes – which deprive the federal budget of many billions of dollars in tax revenue, and overwhelming benefit richer, older Australians (increasing the burden on younger workers in the process).

This way, the tax load required to pay for older Australians’ health costs will be spread more evenly across the population (and across the generations), rather than merely slugging the young.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.