by Chris Becker

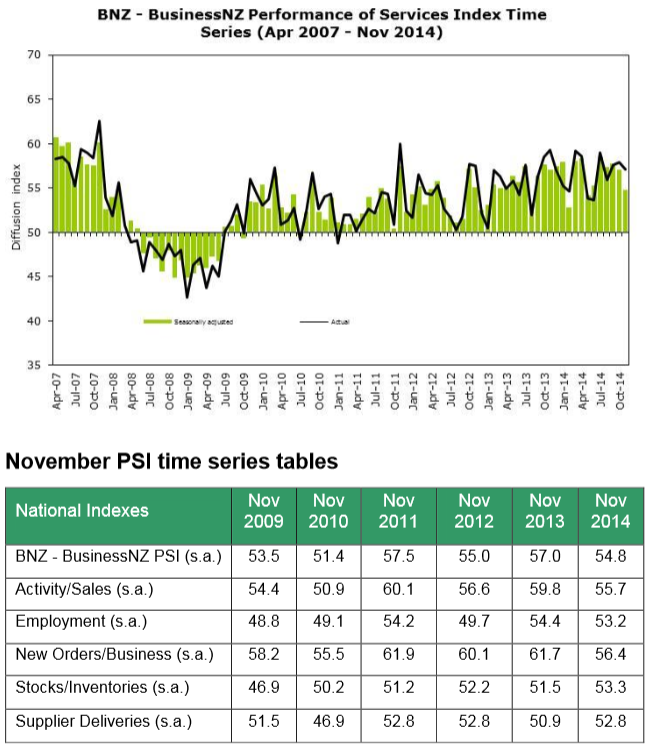

More evidence this morning that the NZ economy has a little more robustness post-mining boom with its performance of services index (PSI) print for November released this morning, expanding again:

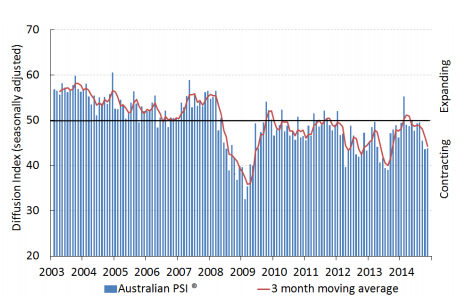

It paints a stark picture compared to that of the latest Australian PSI in November, which printed at 43.8 and is still in terminal decline:

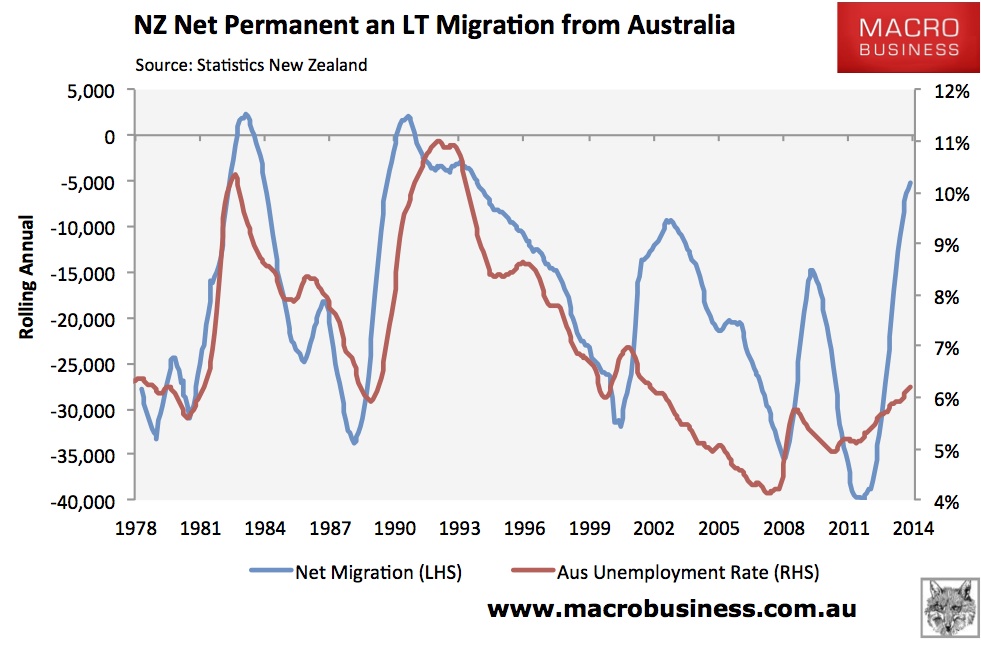

Net migration is helping immensely here, adding to services demand alongside the NZ property bubble (particularly in Auckland):

More interestingly, there’s been a sharp return of Kiwis to the homeland from the usual No.1 emigration destination, Australia, which historically correlates with our unemployment rate, although this time, its leading:

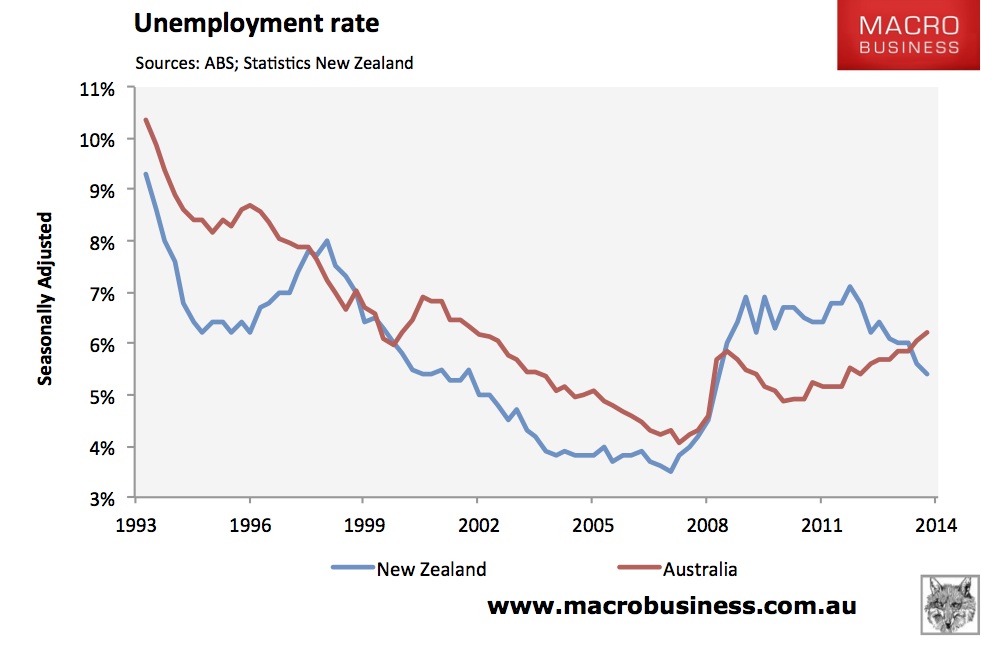

Indeed the Kiwi jobless rate has now crossed below, which goes someway (plus the interest rate differential) to explaining why AUDNZD is finding new bottoms:

Again, the AUDNZD cross is leading the economic divergence and may harbour suggestions of parity on the way as the situation is quite simple: the RBA is more likely to cut first.

I do recall a certain analyst suggesting investing in New Zealand a few years ago when AUDNZD was in the 1.20s….