After her dreadful defences of negative gearing in July and September (thoroughly debunked here and here), The Australian’s Judith Sloan has returned with another abusive post aimed squarely at us “lefty” doomsayers that dare question the merits of Australia’s famed tax expenditures on investment property.

Let’s take a look at Sloan’s latest installment:

HERE we go again. If only the government were to ditch negative gearing on residential real estate then our budget woes would disappear…

Who is calling for this? The Fairfax dailies — whose diminishing number of readers without doubt own geared rental properties at a much higher rate than the population.

Way to start with the strawman arguments, Judith. Who has claimed that Australia’s budget woes would “disappear” if negative gearing was abolished? No one that I know of. Yes, ‘abolishing’ negative gearing would certainly have a positive budget impact – $2 billion per annum according to the Grattan Institute – but it is no budget panacea.

As for your claim that the campaign to abolish negative gearing is some kind of Fairfax conspiracy, get a grip. Did you not read the Final Report of the Murray Financial System Inquiry, which argued for the removal of negative gearing and capital gains tax concessions on investment homes, with David Murray himself claiming that these concessions “drives up prices” and “does nothing to help affordability of homes”.

Moreover, on balance, Fairfax property coverage is in toto notorious for its favourable coverage.

Back to Sloan:

Being able to deduct costs associated with investing in an income-producing asset has always been part of the tax code. It does not simply apply to housing.

To eliminate negative gearing would be to introduce double taxation. The flip side of an investor taking a loan to buy an asset is a lender providing the loan. And that lender pays taxation on the associated profit.

Let’s get something straight. What most opponents of negative gearing are seeking is the quarantining of negative gearing losses on all assets – so that interest and other costs related to an asset can only be offset against the same asset’s income. It is also what happened when the Hawke Government temporarily ‘abolished’ negative gearing between 1985 and 1987. Such tax treatment is standard practice across most developed nations, which do not allow costs related to an investment to be deducted against non-related income (e.g. wages and salary). Australia and New Zealand are outliers in this regard.

Sloan’s argument that “the flip side of an investor taking a loan to buy an asset is a lender providing the loan” and that to disallow the cost of borrowing by investors would amount to “double taxation” is ridiculous.

Using this logic, the private health insurance rebate is not really a cost to the budget, since it is income in the hands of health funds that in turn pay tax to the government. Using the same logic, childcare should be made tax deductible, since childcare centres would earn higher profits, part of which would also be remitted back to the government via company tax (not to mention the extra income taxes paid by childcare workers). To do otherwise would amount to double-taxation, according to Sloan’s twisted logic.

On this point, Sloan also fails to acknowledge that the extra house price inflation caused by negative gearing also means home buyers have to take-out bigger loans and pay more loan interest which, while beneficial to the banks, limits their expenditure elsewhere in the economy, in turn crimping the profits (and tax paid) by other sectors.

Back to Sloan:

To eliminate or restrict negative gearing on residential property would lead to a massive dislocation in the property market. It would hurt renters and affect the incentive for developers to invest in new residential property.

Another classic straw man argument from Sloan. Again, most opponents argue that negative gearing should be quarantined for all assets/investments, not just housing, as was the case when the Hawke Government temporarily ‘abolished’ negative gearing between 1985 and 1987.

As for the claim that eliminating negative gearing would damage the rental market and dampen development, where is Sloan’s evidence?

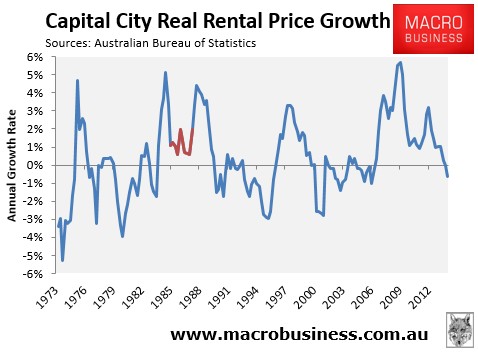

What the data does show is that the last time negative gearing was abolished – between June 1985 and September 1987 – there was absolutely zero impact on rents (shown in red), with much higher rental growth experienced both before and after the policy change (charts at the individual state level are available here):

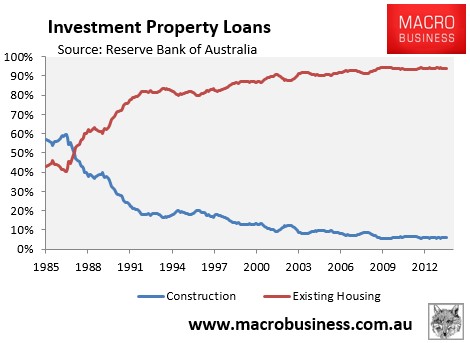

Reserve Bank of Australia data also clearly shows that the proportion of investors constructing new dwellings has fallen spectacularly since negative gearing was re-introduced in September 1987:

Again, only ill-informed and illogical commentary in this debate from Ms Sloan.

unconventionaleconomist@hotmail.com