By Gerard Minack, founder of Minack Advisors

Australia’s once in a century commodity boom is (unsurprisingly) reversing. There is a serious risk – say, a 40% chance – that Australia has a recession in 2015. Recession would become my base case if leading indicators of employment deteriorate. Under almost any scenario the outlook is for a lower A$, lower interest rates and under-performing equities. If there is a recession expect sharp outright losses in equities, notably banks, and significant falls in house prices.

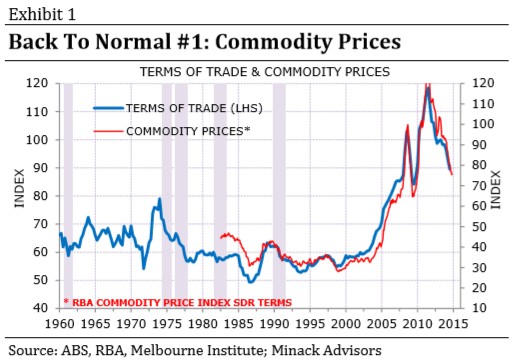

The past decade saw a once-in-a-century boom in Australia’s commodity prices and mining investment. It was completely predicable that the twin booms would not last, even if it was not easy to say exactly when they would peak, or how fast they would reverse. The terms of trade (ratio of export prices to import prices) are now falling fast. They remain well above long-run averages, so further declines are likely (Exhibit 1).

The full text of this article is available to MacroBusiness subscribers