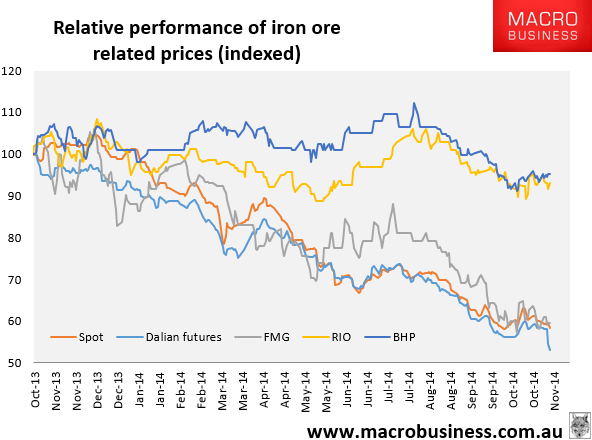

Since last October, the iron ore price is down 42%, Dalian futures are down 47%, FMG is down 41% but the majors – BHP and RIO – are both down only 5% and 7% apiece. Quite impressive, what gives?

The first and most obvious explanation for the outperformance is that they are the lowest cost producers of iron ore in the world and are offsetting price falls with volume expansions. As the price has fallen and margins have been squeezed both have been cutting costs in capex and opex to keep pace. However, there is no way that they’ve added or cut enough!

FMG has also had periods of outperformance (including now in my view) suggesting that markets themselves haven’t grasped the significance of what is happening. This mispricing has been led by sell side analysts that have resisted iron ore price falls all the way down and are still doing so, allowing markets to look through the price weakness to the illusory high plains of forecast better times. This has been boosted by the narrative that the big miners are in a battle for market share that they planned and control, as opposed to truth, which is that they overestimated Chinese demand in their big expansions and now it controls the market.