The AFR’s Chris Joye has continued his crusade against the Big Four banks flimsy capital buffers, revealing over the weekend that Australia’s four major banks had all the capital assigned to their $1.25 trillion home loan books completely wiped out in APRA’s recent stress-tests.

According to Joye’s weekend report, the majors only passed and kept core equity above APRA’s minimums by drawing on capital from other areas of their business and funds that were internally-generated through profits in some years of the test. Just as controversially, the smaller banks did, in fact, appear to have enough capital allocated to their residential mortgages to cover the stress-test losses even though they had higher loss rates.

While APRA never revealed these facts in chairman Wayne Byres’ speech on the stress-tests last week for fear of interfering with David Murray’s financial system inquiry, enquiries by AFR Weekend were able to confirm the findings. According to Joye:

In a footnote in the published version of the speech, Mr Byres said capital for non-major banks was “just sufficient to cover the losses incurred during the stress period”. The footnote added that this “was not the case” for the major banks. The text was unclear as to whether the major banks had sufficient or insufficient capital held against their mortgage books to withstand the losses. But an APRA source confirmed to AFR Weekend that it was the latter, and that all residential mortgage capital was wiped out in the stress test…

AFR Weekend understands that in an earlier iteration of Mr Byres’ speech, the impact of the stress tests on the capital banks’ hold against home loans was discussed in a dedicated section with accompanying charts. This was, however, condensed down to the footnote due to concerns it might interfere with the financial system inquiry.

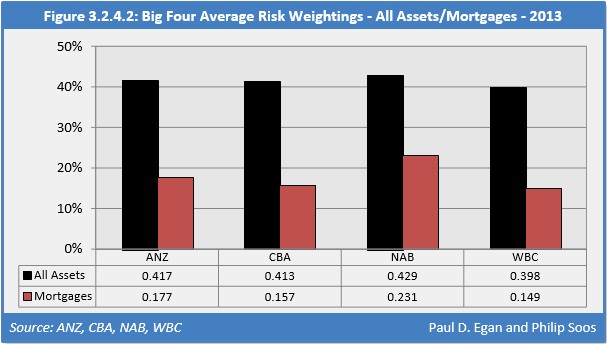

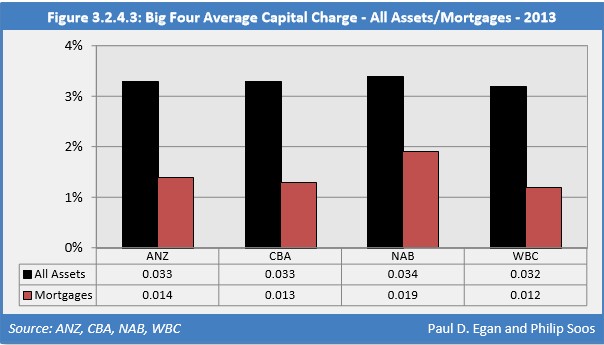

The relative capital strength of the smaller ADIs is due to their use of the “standardised approach to credit risk”, which requires these institutions to assign a 35% risk-weighting to most residential mortgages (i.e. those with an loan-to-value-ratio of 80% or less, or above 80% LVR with lenders’ mortgage insurance). Accordingly, the smaller ADIs are required to hold around 2.8% capital against their mortgage book, or $2.80 per $100 of mortgages.

By contrast, the major banks and Macquarie use their own internal models to determine their risk-weighting, which has resulted in the average risk-weight applied to the Big Four’s mortgages ranging from just 15% to 23%, with the average capital charge against mortgages a meager 1.2% to 1.9% (see below charts).

Hopefully, APRA’s stress testing results will once and for all bury the myth that Australia’s major banks are well-capitalised and embolden the Murray financial system inquiry to recommend increases in their equity buffers when it reports in the next few weeks.

unconventionaleconomist@hotmail.com