The business-as-usual crowd in the press has had an interesting reaction to today’s soft CPI. Phil Baker at the AFR reckons:

The real concern is do we need that rate cut and are we going down the deflationary path like the rest of the world?

…Wednesday’s latest inflation report won’t kill off talk of the possibility that the Reserve Bank can cut the official cash rate one more time if it wants to. But with a property market thriving, the RBA has so far been reluctant to add to it.

If borrowing rates are at record lows what good would another rate cut do?

It would still mean lower borrowing rates, which is why you also need macroprudential policy to ensure that the cheaper money is offset by curtailed distribution. So long as you’ve prepared with that, lowering rates will do one more thing – trash the currency – which is what we desperately need.

Not according to CBA chief economist Michael Blythe who’s had a bizarre reaction the CPI, arguing Australia “is different”, from the SMH blog:

- Interest rates here are a long way from zero, growth rates are a long way from recession, and deflation does not appear to be a serious risk.

- Much of the post‑CPI analysis today will no doubt focus on the impact of removing the carbon tax. Our high‑end expectation reflected data showing that the average size of a utility bill rose in QIII rather than fell. In the event, more of the tax cut impact and less of the gas price rise effect showed up in QIII. Business anecdotes suggested a reluctance to pass on the claimed price benefits of the carbon tax removal.

- So today’s outcome does suggest some upside risk to the RBA’s inflation projections published in August. Those projections assumed that the carbon tax removal will ultimately knock ¾% off the inflation rate.

- The recent fall in the Aussie dollar is the other source of upside risk to RBA forecasts. Today’s data shows tradables (or “imported” inflation) rose by 0.3% in QIII (2.0%pa). This relatively benign result predates the recent drop in the AUD that should have imported inflation starting to lift again.

- Today’s data puts domestic inflation, roughly excluding the carbon tax effect, at 2.7%pa. While the QIII outcome is at the low end of the range of the past decade, it is a moderately disappointing result when benchmarked against the significant slowdown in wages growth over the past eighteen months or more.

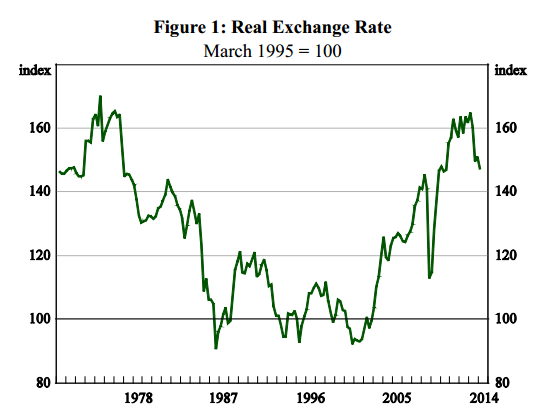

So long as the REER remains so high, we are unable to fire up the tradable sectors of the economy (roughly 40%), and given much of the rest of the economy is moribund owing to household over-indebtedness, that ensures stagnation. The most painless and swift way to engineer improved competitiveness is a fall in the real exchange rate wherein the currency drops but inflation is held down via weak wages.

Both Baker and Blythe are pushing a narrow barrow around housing while ignoring the huge structural overhang from the boom which is preventing a sustainable recovery.