The FT has some nice coverage of the oil market, Australia’s very important emerging commodity via LNG (on which the comatose Australian press is, as usual, snoring). It begins with some conventional wisdom on Saudi Arabia:

By encouraging oil prices to fall, Saudi Arabia is taking a calculated gamble in its already strained relationship with the US, hoping that the potential damage to America’s shale industry will be offset by the geopolitical and economic prizes on offer to Washington.

At a time when the US and Saudi Arabia are fighting a new war together in Iraq and Syria, the Saudis have taken the bold step of asserting their pivotal role in the oil market and subtly squeezing the finances of some of America’s fledgling shale companies.

Yet, at the same time, the falling oil price will deliver a de facto tax cut for American consumers and – if sustained – will hit both Russia and Iran at a time when Washington is trying to pressure both countries.

Deborah Gordon, director of the energy and climate programme at the Carnegie Endowment, sees the Saudi pressure on oil prices as a carefully calibrated move that will not alienate allies but will cause problems for rivals and foes such as Russia and Iran.

“The Saudis seem to have concluded that this could be a game-changer for them,” she says. “They get several benefits without hurting the people they do not want to hurt.”

I can’t help feeling that this is a dated exposition. Saudi represents only has 12.6% of global oil output. It has controlled the market through OPEC (37%) not in and of itself. The FT’s Nick Butler agrees:

…The challenge now is whether the Saudis are in any position to reverse the price fall. The danger of the trend which we have seen since June is that with each step downwards, other producers are tempted to increase production in the short term in order to maximise much needed revenue.

…The only action which would break this trend is a sharp and sustained cut in output by Saudi Arabia. Saudi has acted in this way in the past but never alone. Its cuts in output have always been part of an agreed strategy in which it has been joined, if only in a modest way, by its OPEC partners. But the world has changed and it is hard to think of any OPEC state, except perhaps Kuwait, which is in a position to accept any sustained cut in production and revenue.

The Saudis then are on their own. Can they do it ? The judgment is very marginal. Restoring order will require a serious cut in output of perhaps 2 million barrels a day for a sustained period to rebalance a market which is in surplus even in the absence of significant supplies from Libya and Iran. In the short term such action would require a rewritten budget, reduced domestic welfare and defence spending, and a cut in some of the subsidies being made to allies in the region who are trying to maintain order after the Arab Spring.

Advertisement

A 20% output is massive. And why do it if you make someone else? Finally from the FT on US shale:

Harold Hamm, chief executive of Continental Resources, told the Financial Times all shale companies were reviewing their plans, and some were already cutting back on drilling.

However, he said, the industry would not fall into a crisis in the way it might have done had the oil price fallen this far in 2012.

…Like many shale producers, Continental is still spending more than its operating cash flow on drilling rigs and other capital expenditures. Mr Hamm suggested that many companies would want to bring their spending into line with their income.

“When the market’s going up, you can overspend what your cash flow is, with confidence. But when the market’s going down, it’s not best to do that, because the debt market goes away,” he said.

…Scott Sheffield, chief executive of Pioneer Natural Resources, another leading shale oil producer, told a conference in Washington DC on Tuesday that there would be a “significant cutback” in oil drilling if US benchmark West Texas Intermediate crude fell below $70, and “some cutback” even at $80. The price on Thursday was $80.24

“If it drops into the $70s and the $60s, you will see significant curtailment,” he said.

Presumably that is where we are going then. As well, Reuters adds that shale will not disappear overnight:

…even as drillers consider cutting budgets for 2015, output may continue to grow through next year and possibly into 2016, according to experts and industry insiders.

…Existing wells that are drilled but not yet fracked will keep output surging for months, they said. Many drillers have long-term rig contracts and are loathe to pay costly penalties for dropping equipment they could need soon after. Most have hedged next year’s production at much higher prices, and are racing to lock in 2016, protecting their revenues even if the free-fall in oil marketscontinues.

…”It is not as though oil goes to $75 and everyone just panics,” said Mark Hanson, an energy analyst at Morningstar. Prices would have to remain below $75 a barrel for a prolonged period before drilling slows. Some plays are profitable as low as $50 a barrel, he said, let alone $80.

Many companies have also already locked in their 2015 hedges at higher prices that will make next year’s output profitable, according to company presentations.

…Genscape analysts expect the oil rig count to fall by 300 by the end of 2015, but even that would only slow oil production growth to some 600,000 bpd, according to their models. That’s nearly enough to meet the increase in global demand this year.

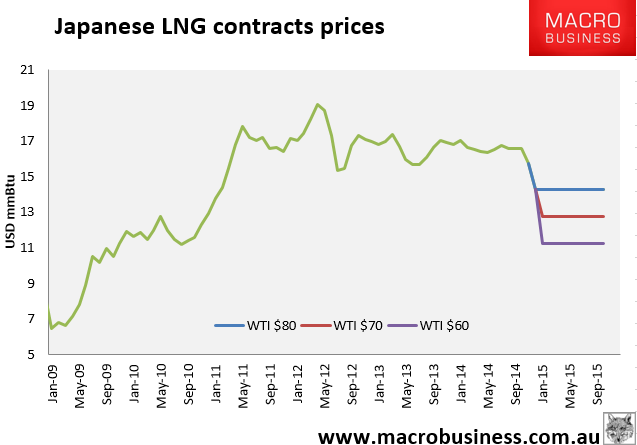

Here, then, is the LNG oil-linked price chart:

By 2017, Australian and US LNG will be flooding into the Pacific Rim market, keeping pressure on LNG spot prices and oil-linked contracts to bend or break. It appears the great LNG price correction has come four years early.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.