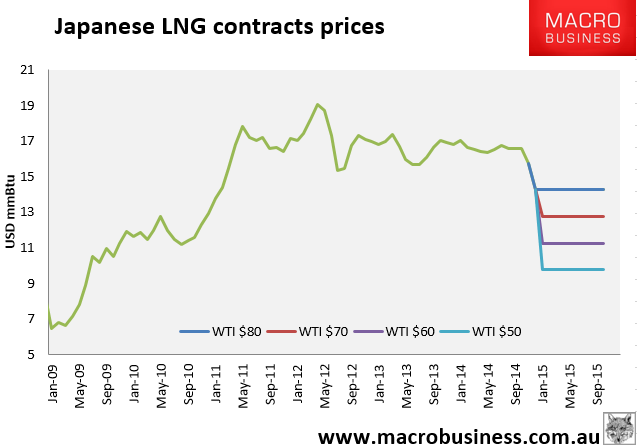

Citi today offers some useful analysis of the trillion-dollar question. At what price can Saudi and/or OPEX dislodge US shale oil production? And, by extension, what price are we going to see for LNG contracts for the next few years?

In a stand-off between OPEC and US shale, how low can shale go? In a bear scenario, $75 WTI may only be a soft floor

Brent and WTI have plummeted, and supply cuts are needed to support prices; with the Saudis and OPEC bracing for lower prices, shale is set for a showdown with the cartel.

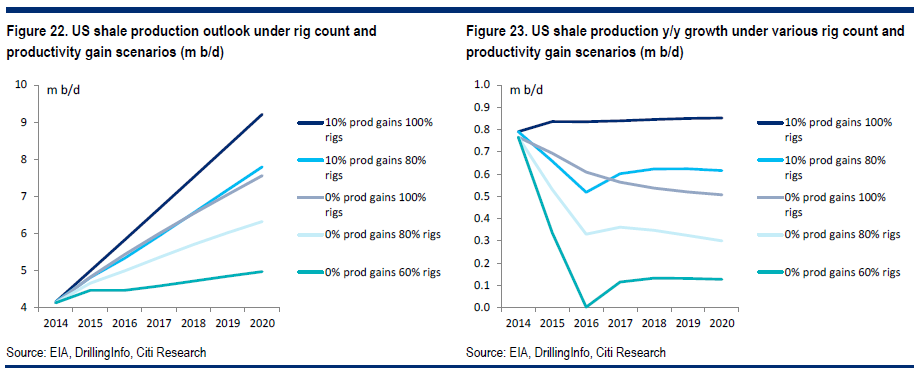

At what price might US shale production growth be meaningfully reined in? Full-cycle capex for shale production includes land, infrastructure, and well costs (of which some 40-50% is from pumps, ~10-15% for drilling rigs) and operating costs. In mature plays where the land grab is over and infrastructure is available, the remaining capex required (“half-cycle costs”) to bring on an additional well is far lower than areas requiring “full-cycle” costs. Full-cycle costs might be as high as $70-80/bbl WTI, but half-cycle costs could be as low as the high $30s-range. Thus, those fringe and emerging areas requiring full-cycle capex could now face a reassessment, while established areas should continue drilling and growing output.

Shale production breakeven prices are particularly driven by well productivity (initial production/IP) and well costs; there can be a wide range of IPs within a single play. In the Eagle Ford, an $8m well with IP of 400 b/d breaks even at ~$70 WTI, but an $8m well with a 500 b/d IP breaks even at $55; fringe acreage should be the first to be cut. A $7m well with a 400 b/d IP is economic at $60 WTI; well cost reductions matter too, and could fall by ~20% as services sector slack intensifies.

To triangulate how much US shale production growth might be curbed at $70 WTI, two approaches are considered: sensitivity to rig count reductions, and a look at distribution of well IPs. WTI prices below $70 could rein in as much as 25% of rigs; such a sustained rig reduction could lead to a ~25% fall in US shale output growth in 2015 and a ~50% fall in production growth in 2016. A 40% reduction in rigs or more might be needed to completely flatten production growth – but this is based on modeled reductions of average wells, not the least productive wells. Productivity gains can also offset this further. In any case, at $70 WTI, this is a slowdown, not a halt, in production growth.

An assessment of wells that might be left undrilled at $70 WTI can be made by looking at wells below certain IP rates (though well costs are not necessarily independent from IPs). A look at recent wells drilled suggests that even if ~70% of wells could become uneconomic at $70 WTI, they might only account for 30% of business-as-usual production. To take out enough new production to flatten production growth might require prices in the $50 range in the short-term.

Additional factors create inertia that can slow producer pullbacks, such as sunk costs, well backlogs, and producer hedging.

In short, many current assessments of US shale costs could be wildly underestimating the robustness of US oil production growth.

Yep, that’s fair bet, given what we are living through on just about every other industrial commodity forecast currently. On the upside, it is very unlikely that Saudi would be prepared to push prices to $50 given that that would destroy its own budget. A period of sub-$70 seems more plausible.

Still, here’s what it looks like for LNG contract prices:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.