The brainiacks at the Housing Industry Association (HIA) have produced another piece of self-interested “analysis” warning against changes to negative gearing and lobbying to remove stamp duties. From The SMH:

Cutting back tax deductions for property investors would erode housing affordability, reduce housing supply and bump up rents, a new report says…

…reducing negative gearing would diminish the incentive to invest in housing and exacerbate current undersupply, pushing rents almost one per cent higher…

“Under current housing policy settings, discounting residential negative gearing would lower Australian living standards by making the tax system less efficient,” the report says…

“Adding to the tax burden on rental properties reduces the incentive to invest in housing, and therefore reduces housing supply…

Abolishing stamp duty on property transfers, however, would improve housing affordability and living standards, by removing barriers to investing, the report said.

While it is true that winding back negative gearing would “diminish the incentive to invest in housing”, why would this be such a bad thing?

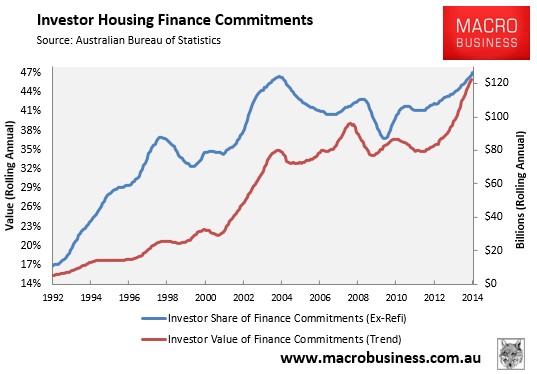

Removing some speculative demand from the housing market – which is absolutely rampant at present (see next chart) – would take the pressure off house prices, improve housing affordability, and increase the rate of home ownership by allowing more first home buyers to enter the market.

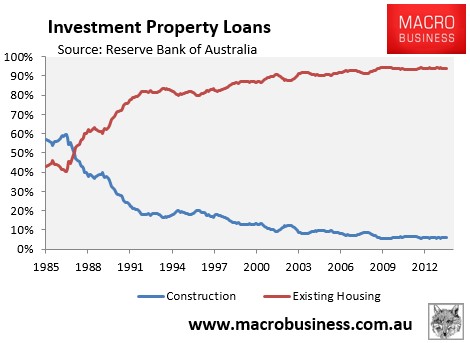

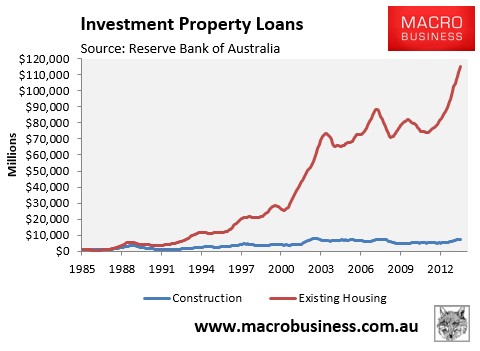

As for the HIA’s claim about rental supply, Reserve Bank of Australia data clearly shows that the overwhelming majority of investors – over 90% – buy existing dwellings rather than invest in new construction. It also shows that the proportion of investors constructing new dwellings has fallen spectacularly since negative gearing was re-introduced in September 1987 (see below charts).

Since investors primarily purchase existing dwellings, negative gearing in its current form simply substitutes homes for sale into homes for let. As such, the policy has done little to boost the overall supply of housing or improve rental supply or rental affordability.

For this reason, the HIA’s warning that rents would rise if negative gearing was wound-back also does not hold water.

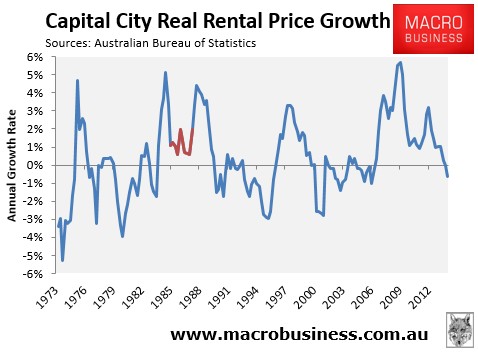

The next chart plots the Australian Bureau of Statistics (ABS) rental series from 1972 in real (inflation-adjusted) terms, with the period where negative gearing losses were last quarantined (i.e between June 1985 and September 1987) shown in red. As you can see, there was no discernible impact from the ‘abolition’ of negative gearing on rents, with periods of higher rental growth recorded both prior to and subsequently. Charts at the individual state level are available here.

Finally, the HIA’s recommendation that the Government should instead abolish stamp duty is meaningless unless it can identify an alternative source of taxation revenue for the states. My pick would be replacing stamp duties with a broad-based land tax, but would the HIA support such a move?

As noted many times before – so many times that it is getting boring – negative gearing is costing the government billions in lost tax revenue but is doing absolutely nothing to boost supply. It also creates additional demand from tax subsidised investors, placing upward pressure on home prices and locking-out would-be first time buyers.

There is little policy rationale in favour of keeping negative gearing in its current form, whose foregone funds could instead be used to fund schools, hospitals, housing-related infrastructure, or any number of other worthwhile initiatives.

The Government would do well to ignore the screams from vested interests, like the HIA, which seems more concerned about protecting the value of its member’s land banks rather than actually boosting supply and improving affordability.

unconventionaleconomist@hotmail.com