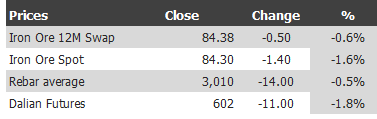

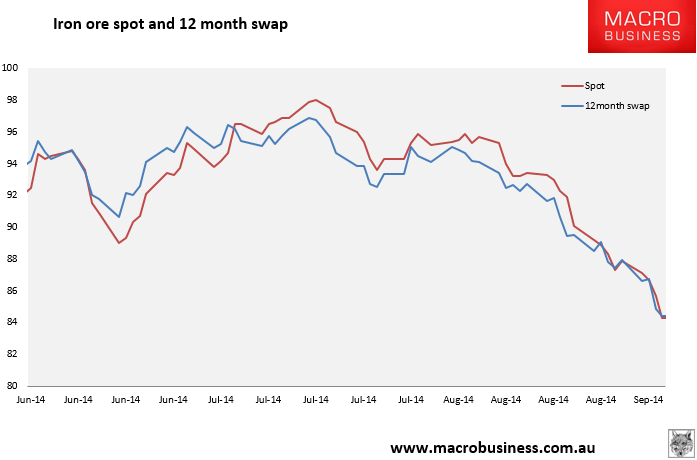

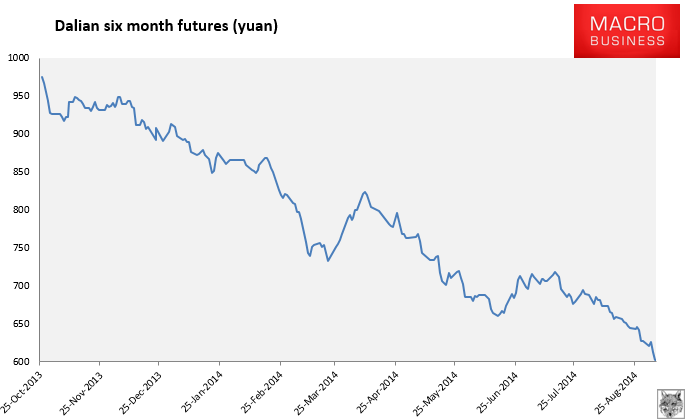

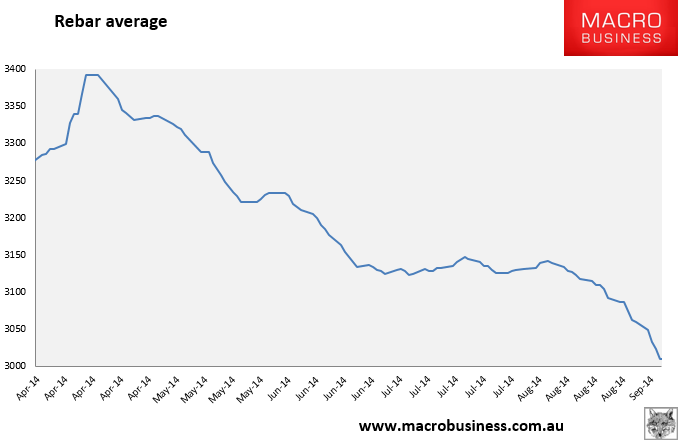

Here are the iron ore price charts for September 4, 2014:

All markets still in free fall. And still no convincing contango signaling a turn. Rebar futures are leading everything down, falling sharply again yesterday to end at 2838.

Miners continued to trade as if this is nothing more than a cyclical blip yesterday. And of course, Goldman was out suggesting there’s not much prospect of a deep destocking by steel mills. If you’re on board with this line of thinking then Kimber Capital suggests you go long the living dead.

Advertisement