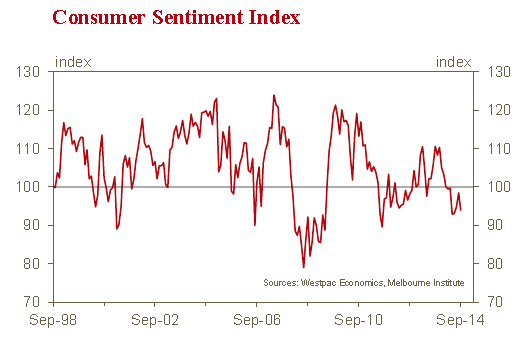

Westpac’s Consumer Sentiment Index sank by 4.6% in September from 98.5 in August.From Bill Evans:

This is a surprising and disappointing result. Following the 6.8% plunge in the Index in the aftermath of the Commonwealth Budget in May the Index had stabilised and was gaining ground. From June to August the Index had lifted by 5.9% to find it only 1.3% below the pre-Budget level. The Index is now 5.8% below the pre- Budget level and only 1.1% above the post-Budget print. In effect most of the steady recovery we had seen in the Index over the last three months has been eroded.

Every quarter we survey respondents’ recall of major news items.

In June, following the release of the Commonwealth Budget, 73.8% of respondents recalled news items about ‘Budget and taxation’. That was a significantly higher percentage than for any other categories of news items, the next highest being ‘economic conditions’ (42.7%); ‘employment’ (22.2%); and ‘interest rates’ (16%).

For September ‘Budget and taxation’ continues to dominate. The significant topics recalled in September are: ‘Budget and taxation’ (62.7%); ‘economic conditions’ (53%); ‘employment’ (29.5%); and ‘interest rates’ (18.1%).

We also survey whether respondents assess the news heard as being favourable or unfavourable. All four topics were assessed as unfavourable although there were some marginal improvements in ‘Budget and taxation’ and ‘employment’. There was a marginal deterioration in ‘economic conditions’ and assessments of news on ‘interest rates’ were steady.

The proportion of respondents recalling ‘Budget and taxation’ issues is the second highest since the survey was introduced in mid-70s. The highest was the June reading and this compares with other high readings of 56.3% in June 2000 (associated with the introduction of the GST) and 55.2% in June 2010 (associated with the announcement of the mining tax). On both those occasions ‘news recall’ had fallen away significantly by the following quarter, to 26.7% and 30.5% respectively.

A reasonable summary from the ‘news heard’ / ‘news recall’ series is that households are a little more comfortable with the Budget but it continues to dominate their thinking and they remain on edge. Furthermore, they are still quite concerned about the domestic economy and the labour market with these concerns having deteriorated further since June.

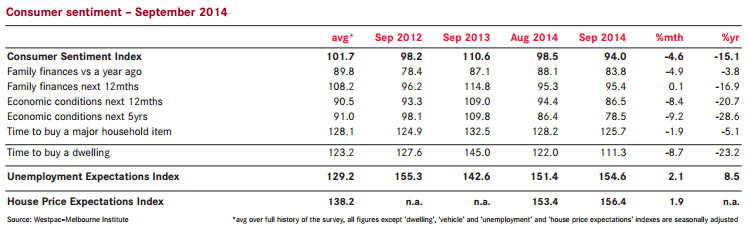

Four of the five components of the Index fell in September.

One component, the sub-index tracking expectations for ‘family finances over the next 12 months’ was steady. The sub-index tracking assessments of ‘family finances compared to a year ago’ fell by 4.9%. There was a sharp deterioration in respondents’ 10 September 2014 assessments of the economic outlook. The sub-indexes tracking views on “economic conditions over the next 12 months” and “economic conditions over the next 5 years” fell by 8.4% and 9.2% respectively. The sub-index tracking assessments of ‘whether now is a good time to buy a major household item’ fell by 1.9%.

Of most concern here is the five year economic outlook. This component is typically much more stable than the 1 year outlook but the print in September is the lowest for 16 years. It is down 28.6% on its level from a year ago. Concerns around the medium term outlook are likely to make households more cautious.

Logically, such concerns indicate that households expect any current economic weakness to be sustained for a considerable period.

The ‘news heard’ indexes indicated that respondents remain nervous around the labour market. These concerns were emphasised by the 2.1% increase in the Westpac–Melbourne Institute Unemployment Expectations Index (recall that a rise in the Index shows heightened concerns around the employment outlook). Fortunately, the Index is still 2.0% below its average for the first half of 2014 but there appears to be no sign of any sustained improvement in respondents’ outlook for the labour market.

Households continue to expect house prices to keep rising. The Westpac–Melbourne Institute House Price Expectations Index rose by 1.9% to be 25.5% above the level in July 2012 and 7.4% higher than July 2013.

However, there was an 8.2% fall in the index tracking assessments of ‘time to buy a dwelling’. This index is now 23.2% below its peak level in September last year. Clearly, households are unnerved by rising prices, surmising that affordability issues are constraining the attractiveness of buying a house. As we saw in the recent housing finance statistics, the momentum in the housing markets is clearly moving towards investors who are motivated by prospective price gains and rental yields and less affected by affordability considerations.

The September survey included additional questions on the ‘wisest place for savings’. Responses show just over a third of consumers (34%) now favour ‘bank deposits’, up significantly on June’s 27%. While that suggests a more conservative approach to finances, the consumers continue to show less emphasis on debt reduction with just 14% nominating ‘pay down debt’ as the best option – that compares with 17% in June and average readings of 20–25% between 2008 and 2012. ‘Real estate’ was still viewed relatively favourably with 26% nominating this as the ‘wisest place for savings’ in line with the reading in June. Fewer consumers favoured ‘shares’ (8.5% down from 10%) and ‘super’ (4% down from 5.5%). The mix suggests a further slight increase in consumer caution but still a marked improvement on the risk averse attitudes prevailing two years ago.

The Reserve Bank board next meets on October 7. The disappointing results in this survey are consistent with a need for lower interest rates rather than higher interest rates. However, the Governor has made it clear that lowering interest rates is not on the policy agenda. In his recent statement following the September Board meeting he reiterated his guidance that “the most prudent course is likely to be a period of stability in interest rates”. This survey indicates that households are still concerned about the jobs market. However in a recent speech the Governor noted that “while we may desire to see a faster reduction in the rate of unemployment, further inflating an already elevated level of housing prices seems an unwise route to try to achieve that”.

Consequently we cannot expect anything apart from a no change decision at the upcoming meeting. We continue to expect that rates will remain on hold for another year until they are raised next August. Of course, issues around the recent Budget, which are still unnerving households, will have been resolved and we expect that households will be encouraged by their much improved balance sheets to lift spending.

My own take is a little more straight forward. Consumers are aware that:

housing is a raging bubble

iron ore is crashing

the country is run by idiots

Advertisement

There’ll be no recovery in “balance sheet” spending given the above and there’s no income to spend either. Rate cuts coming.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.